Is The Truth Engine Being Distorted?

Updated On 9 July 2026

Published On 10 July 2026

%20(6)-1-960x540.webp?prefix=media)

Key takeaways:

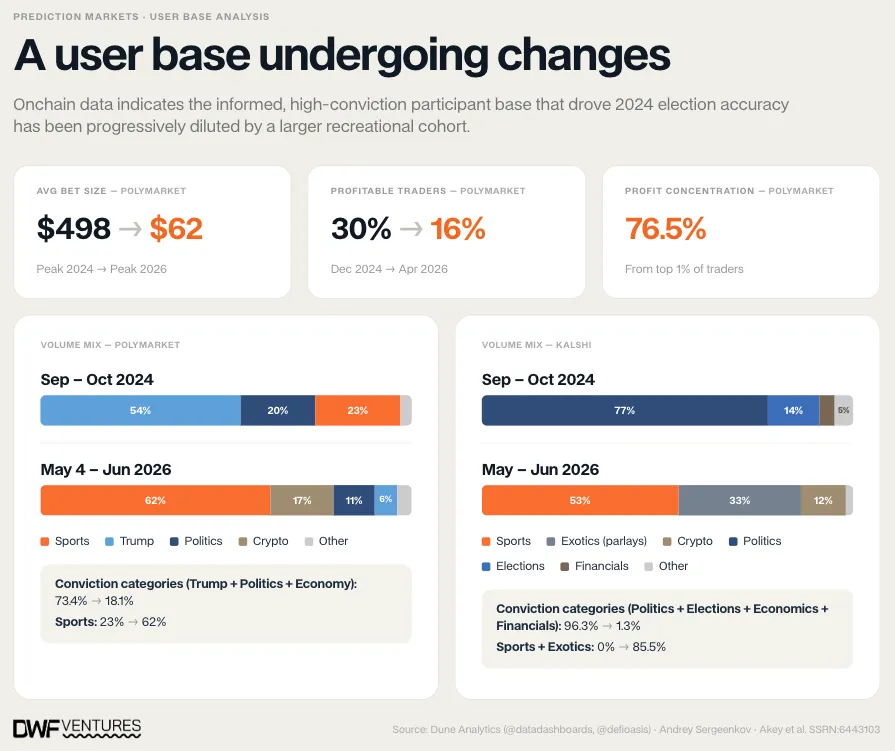

- Onchain data shows prediction market user bases have shifted fundamentally since 2024. Informed, conviction-driven trading has been diluted by a much larger recreational cohort motivated by entertainment and outsized payouts rather than accurate forecasting.

- Kalshi and Polymarket's informed trading categories (politics, elections, and economics) collapsed from 73–96% of volume during the 2024 election to under 20% today, replaced by sports and parlay-dominated activity

- The RFQ parlay model on both platforms creates a structural information asymmetry. Institutional market makers price combinations through infrastructure retail users cannot see or verify.

- The current trajectory of prediction markets suggest a growing deviation from their initial mission of being an accurate, transparent forecasting tool, and instead towards gambling products they have long sought to distinguish themselves from.

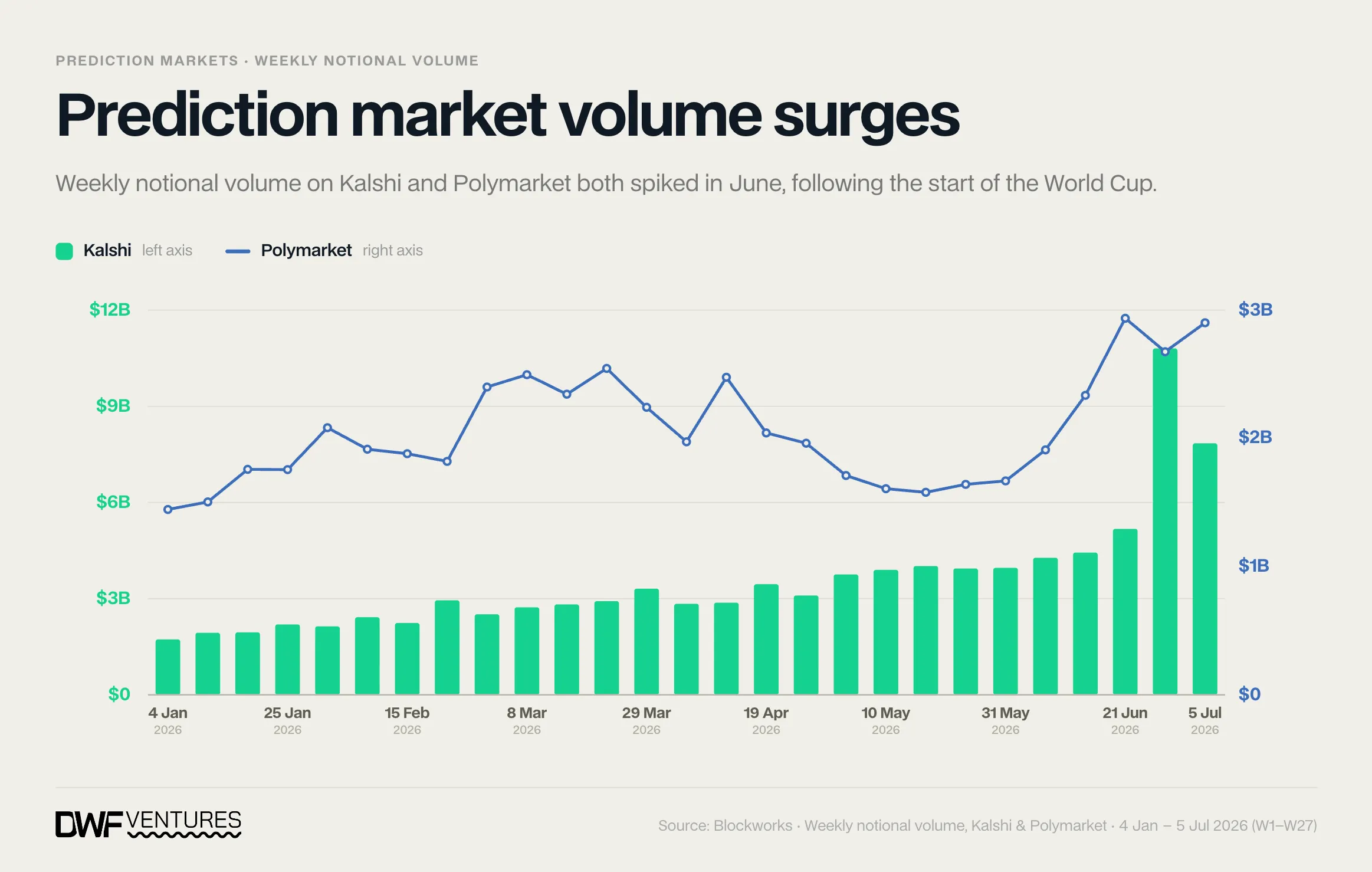

Polymarket’s parlay product launched on June 15th, in the midst of the World Cup group stage. This was in line with the biggest weeks posted by prediction markets, with Kalshi and Polymarket doing close to $9 billion and $3 billion in weekly notional volume respectively. While the rising share of volume derived from sports markets makes this a practical product extension, this raises the question of the type of users the platforms are catering to and trying to onboard, and if they differ from the early group of users that contributed to the feasibility and accuracy of the truth engines prediction markets set out to be.

The initial vision of prediction markets was built on the claim that financial stakes produce more accurate forecasts than traditional alternatives, since users bet on what they think will happen rather than what they want to happen. The 2024 US election reflected this, as Polymarket had Trump’s victory priced at 60% or above for extended periods of time while polls hovered between 45-50%. Polymarket would even reach up to 95% nearing the end of the election day, an accuracy level attributed to its then user base.

A Shifting User Base

In its early years, Polymarket attracted a few distinct groups of users: crypto-native traders, political insiders and analysts, and information arbitrageurs. These groups were similar in the way they traded based on information, not entertainment. However, onchain evidence suggests that this relatively sophisticated user base has since changed drastically.

- Average bet size is down >85% from peak 2024: While not definitive, a dropoff of this magnitude cannot be attributed solely with an adjustment in user strategies but instead to the arrival of an entirely new type of user. Furthermore, a Bitget Wallet study found that 60% of Polymarket's active traders had no prior onchain experience before joining the platform. These users likely lack prior framework for sizing positions in a financial market, causing the overall decline in bet size.

- A large portion of traders are unprofitable: This is consistent with a user base that has lost the informational advantage that made prediction markets accurate. The 2024 election user base traded in categories where research, political networks, and data analysis produced genuine edges: Trump, politics, and elections-related markets together accounted for 73% of Polymarket volume and 96% of Kalshi's during that period. The current user base is concentrated in sports, where the information edge available to a retail participant is far lower and sometimes non-existent. Knowing more than the market about a World Cup scoreline is fundamentally different, and far harder than knowing more than the market about a Fed rate decision.

- Sports and exotics markets are dominating volume: Exotics (parlays) alone have grown to contribute 33% of total volume on Kalshi, representing vast interest from their user base. Parlay products present the opportunity of a large multiplier on a small initial stake, appealing specifically to the risk-loving, and payout-motivated user who treats prediction markets as a form of entertainment versus a platform to express calibrated conviction. This is similar to sports markets, where the information edge is low and users are tempted with the upside of underdog comebacks and major upsets. The smaller the bet size, the more the parlays and sports markets payout narrative dominates user decisions, and in the case of parlays, the less any individual leg reflects a genuine probability assessment. As such, the falling average bet size and the rising share of parlay volume are unlikely independent trends.

Contradiction & Noise

While these trends have done little to hurt prediction markets from a commercial standpoint, they introduce substantial contradiction to what prediction markets initially set out to achieve. The forecasting mechanism that made them accurate and useful depends largely on a specific type of user, one with an information edge, who is financially incentivised to correct mispricings and push event prices toward their true probability. When that user base is diluted by a much larger base of entertainment-motivated users placing small, high-frequency sports bets and parlays, the self-correcting mechanism weakens. Trades motivated by payout preference rather than calibrated belief still move prices, but for reasons largely unrelated to the actual probability of the outcome.

The end result is a noisier signal generated by a user base that looks increasingly like a sportsbook's recreational betting population, being consumed by institutional partners like ARK Invest, ICE, and CNN, who built their initial relationships with these platforms on the vision of truth engines. While noise is initially limited to data from markets like sports, this could potentially see spill over effects in the future.

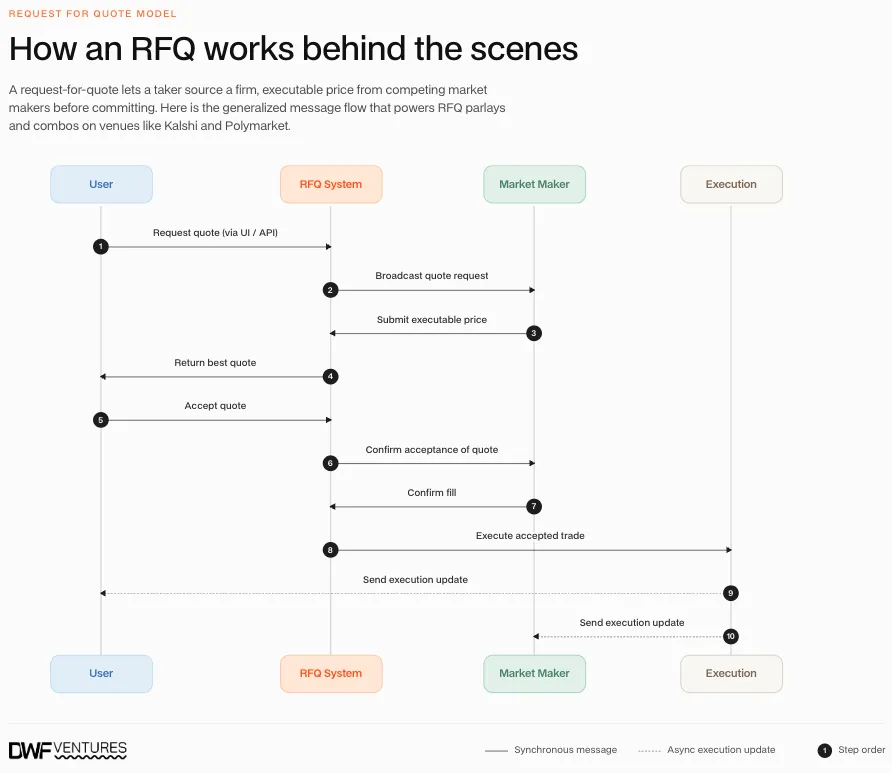

The concern compounds when parlays are factored in specifically. Current parlays on Polymarket and Kalshi run off an RFQ model, where users submit their desired combinations and receive price quotes from institutional market makers. This structure, although opaque, is a practical necessity, given the proprietary modelling infrastructure required to price multi-leg predictions. Retail users are left to take on a trade in the face of this structural information asymmetry, without a means to verify fairness of quoted odds, or independently access models used to price the combination of correlated legs.

The Underlying Opportunity

The above bear case, however, assumes that entertainment-driven volume and forecasting ability are inherently in conflict. A counterintuitive argument in favor of prediction markets is that more volume makes individual markets more liquid and harder to manipulate over time, regardless of the type of volume. Casual and entertainment-driven participation contributes to a deeper orderbook, raising the cost of manipulation and tightening spreads. On top of this, a growing user base and volume is still a strong indicator of platform success and PMF, and will provide them the revenue required to continue to iterate and improve. While dominance of entertainment and payout-driven users have grown substantially, it is also important to note that the absolute number of information and conviction-based traders could have still increased, and the depth of political and economic markets in the 2028 US elections could substantially exceed that of 2024’s.

The more compelling opportunity, however, lies with fixing the structural flaw that parlay products currently face. The information asymmetry in the existing RFQ model is not completely inevitable, but the result of a design choice optimised for convenience. Alongside quotes from institutional market makers, platforms could implement a publicly visible model, where correlation assumptions are disclosed and auditable by any user. Any systematic mispricing in those correlation assumptions would be immediately exploitable by sophisticated arbitrageurs, creating a self-correcting dynamic that mirrors the mechanism that made single-contract prediction markets accurate. A parlay product built this way would not only be more transparent, but also defensible to regulators.

Conclusion

The truth engines that previously built their credibility on the 2024 US elections have shifted in composition, and is now dominated by a more recreational and entertainment-driven user base, noise, sports and parlay volume, and an RFQ model that disadvantages the least sophisticated users. If left unaddressed, this shift points towards a product that thrives commercially while drifting from the forecasting mission that prediction markets were created to achieve. Conversely, this could serve as a key gateway for prediction markets into a more general and wider target audience that poses many clear advantages for the future such as deeper liquidity and lower risk of market manipulation. The focus should instead be on their next steps: how will the platforms convert these users into accurate signals?

NFA + DYOR