Stablecoin Velocity Hits Record 49.7x as Real Economic Usage Surges

Published On 2 June 2026

Stablecoin Velocity Hits Record 49.7x as Real Economic Usage Surges

- Remittances, B2B and B2C payments is now the fastest-growing segment, while exchange-related volume has shrunk to a minor share of total activity

- Since 2025, transaction volume has outpaced supply growth, pushing velocity (actual dollar usage) first to 39.3x and now to the current 49.7x annualized run rate.

- Spanning three full quarters, Bitcoin ETFs are now weathering their longest sustained outflow period on record, while the diminishing of Grayscale’s Ethereum ETF overhang has revealed a lack of institutional interest toward ETH.

In recent weeks, we have seen two key developments playing out: stablecoin usage is aggressively accelerating alongside real world adoption, while Bitcoin and Ethereum ETFs are experiencing sustained net outflows. This week, we dive deeper into both trends, uncovering what the data is telling us.

Money at the Speed of the Internet

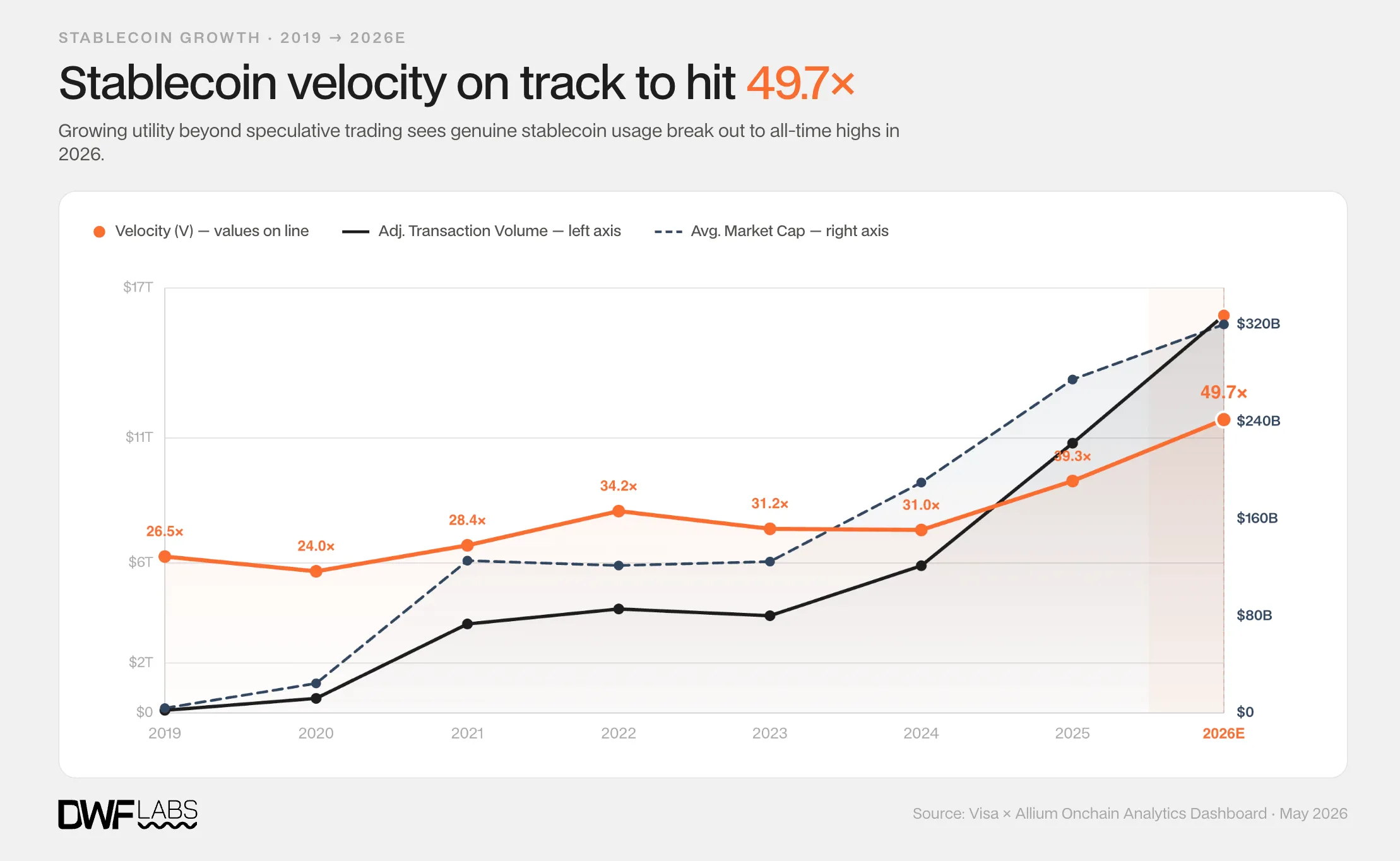

$320 billion tokenized American dollars. That is the number you have seen dominating headlines everywhere. Yet market cap is only half of the equation for a digital currency. The more important number right now is velocity, which measures how often those dollars are actually being used. When we say stablecoin velocity is at 20x, it means that for every single tokenized dollar currently in circulation, that specific dollar is changing hands an average of 20 times per year. A soaring velocity proves capital is circulating rapidly to facilitate real trade and transaction volume rather than sitting stagnant or idle as dead weight in accounts.

According to filtered data from Visa and Allium, which removes bots, high-frequency trading loops, and internal transactions, stablecoin velocity has reached an annualized rate of 49.7x, shattering every previous record. In less than five months this year, stablecoins have facilitated $6.64 trillion in filtered transaction volume. More importantly, the composition of that volume has shifted. Non-exchange activity, remittances, B2B and B2C payments is now the fastest-growing segment, while exchange-related volume has shrunk to a minor share of total activity. This marks a clear structural break from previous cycles, dividing stablecoin adoption into three distinct phases.

Note: 2026 velocity was calculated by annualizing year-to-date filtered transaction volume and dividing by the current stablecoin market cap of $320B.

3 phases of stablecoin adoption

Phase 1 (2019–2021): The Speculative Bootstrap. Stablecoin growth was largely tied to speculative activity. Velocity stayed range-bound between 24× and 28× even as market cap exploded, meaning usage grew in exact lockstep with incoming capital.

Phase 2 (2022–2024): The Stress-Test. The market entered a defensive regime. Velocity actually peaked at 34.2× during the Terra and FTX collapses as users aggressively moved money off exchanges and de-risked. When the market recovered in 2024, velocity remained flat at 31.0× despite rising supply, suggesting much of the new capital was still sitting rather than working.

Phase 3 (2025–Present): Real World Adoption. Since 2025, transaction volume has completely outpaced supply growth, pushing velocity first to 39.3× and now to the current 49.7× annualized run rate. It reflects a genuine expansion of real-world utility over speculation.

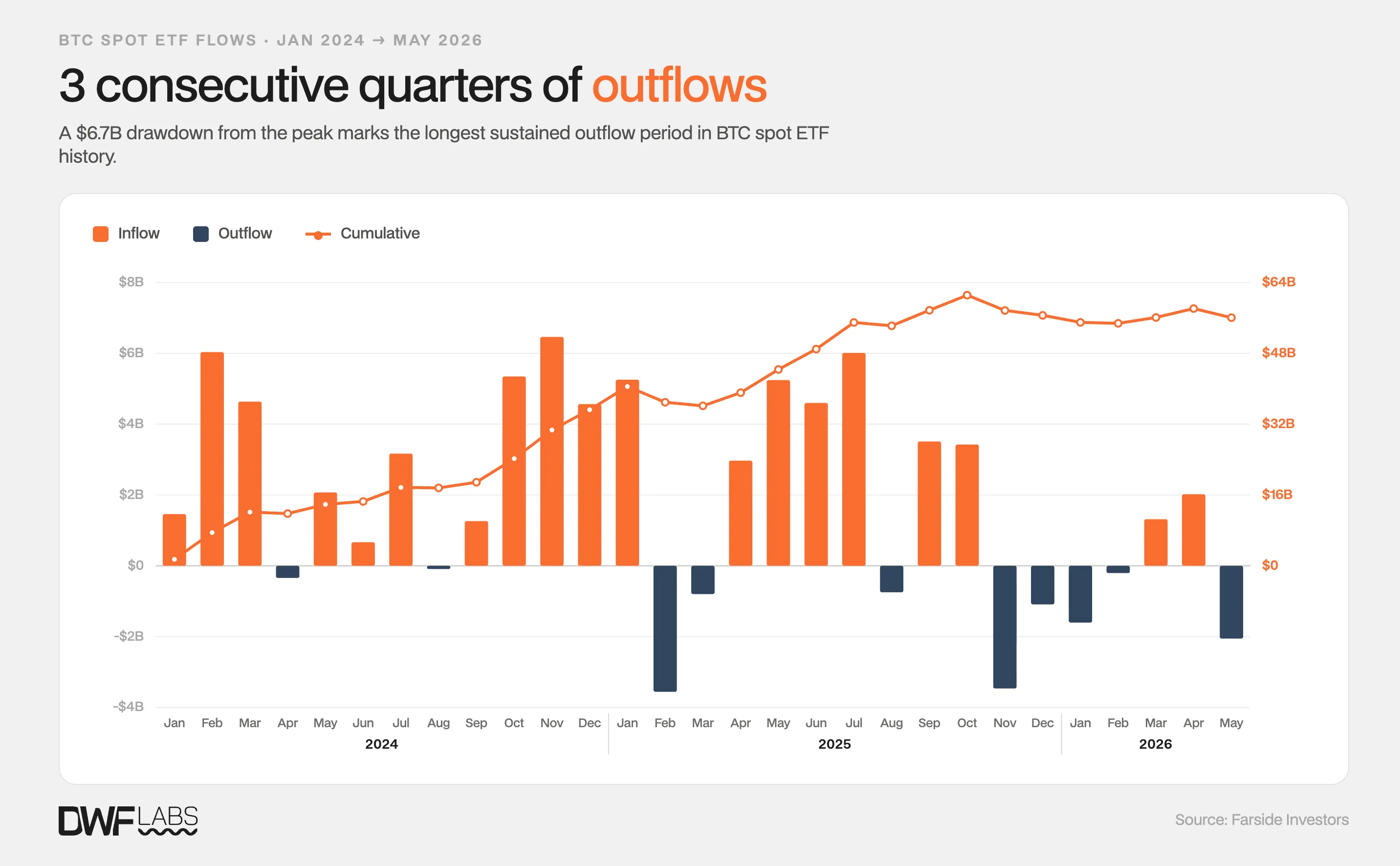

The Longest Dry Spell Since Launch

After six consecutive quarters of net inflows, Bitcoin spot ETFs started seeing outflows in October 2025 and have not meaningfully recovered since. A $6.6B drawdown from the peak across the last three quarters marks the longest sustained outflow period in the short history of these products.

For most of the ETF's history, large outflow days carried a specific signature: capital leaving the expensive GBTC and rotating into cheaper alternatives like IBIT or FBTC. It looked like selling but it was really just housekeeping; institutional money was shuffling between more capital efficient products.

What’s happening the past month is categorically different. On May 27, IBIT itself posted a single-day outflow of $527.8M. This was not a rotation, and it was not a rebalancing. The entire wall of institutional money pulled back simultaneously, producing a total daily net outflow of $733.4M across all issuers, marking one of the largest single-day contractions.The peak capital that accumulated through October 2025 was never uniformly earned either; a single macro catalyst, the United States election result in November 2024, led to $6.5B of net inflows that month. The highest ever.

Momentum trades inevitably unwind. Three quarters of evidence is forcing a question the industry has been reluctant to sit with: are institutional allocators treating Bitcoin ETFs as a genuine, long-duration portfolio allocation, or as a macro momentum vehicle they rotate in and out of like any other volatile risk asset? The data right now is leaning heavily toward the latter.

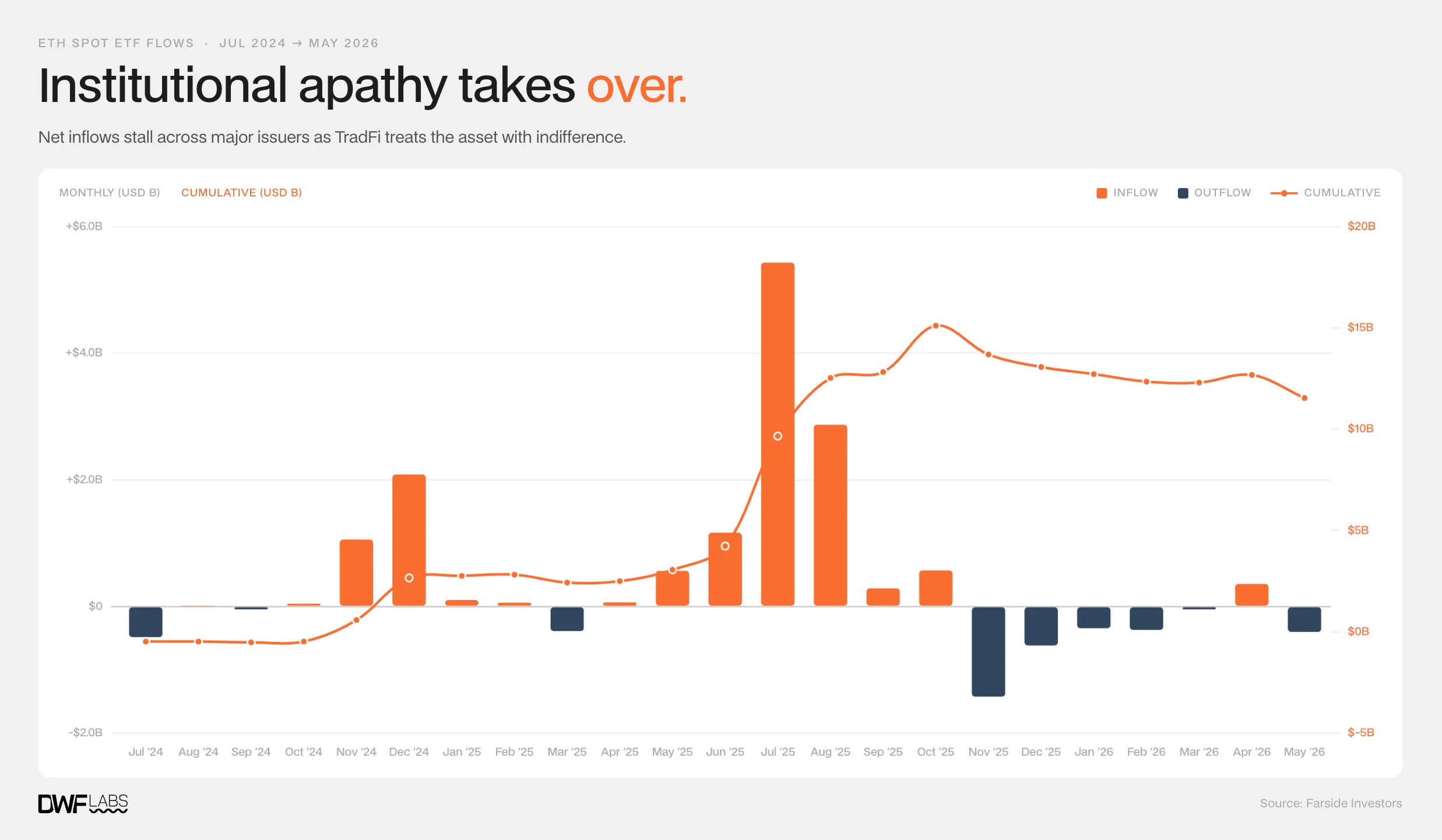

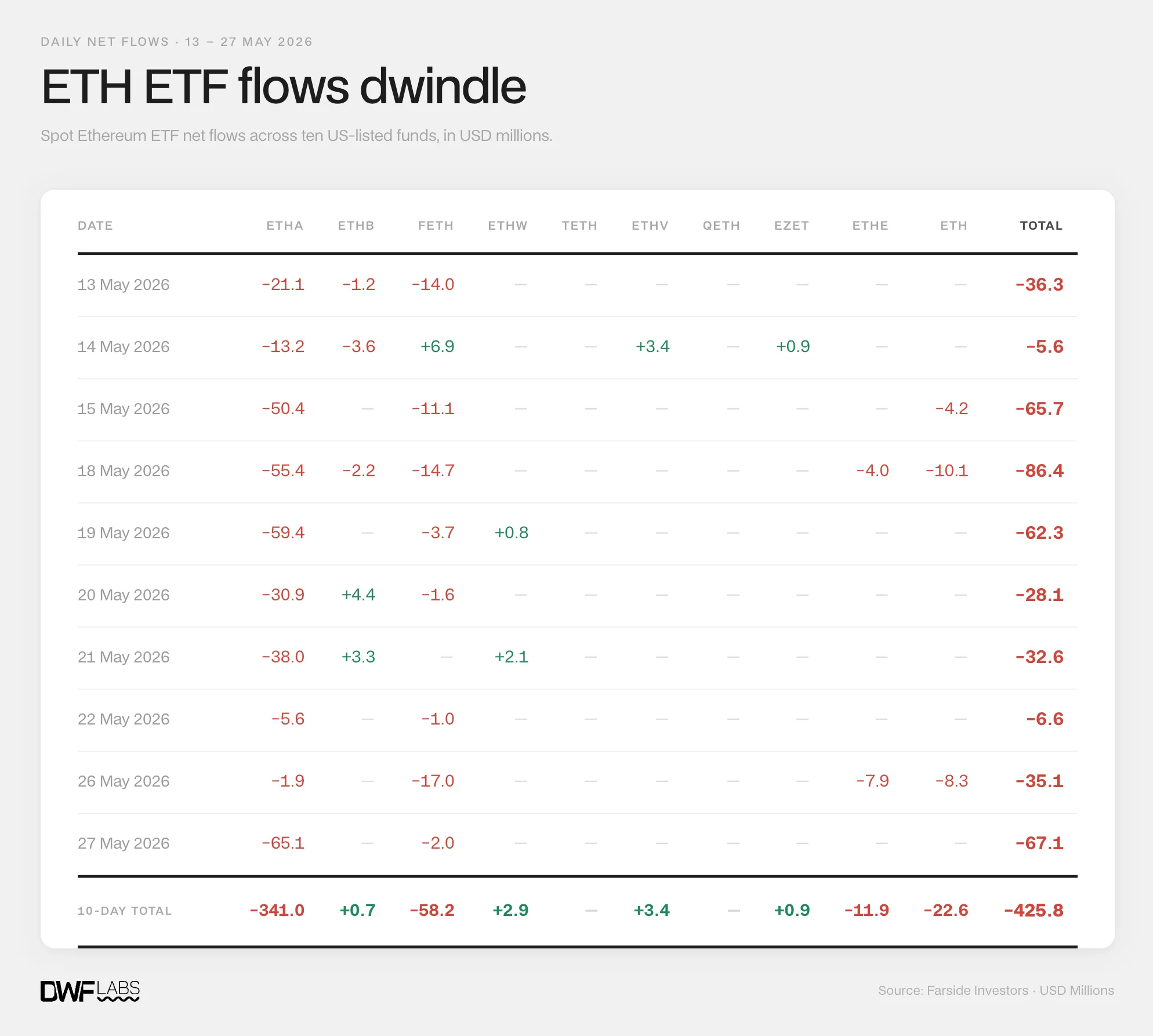

The Quiet Flatline

Ethereum's ETF journey has had more turbulence packed into its shorter life than Bitcoin's. The products launched in July 2024 and immediately followed a familiar script. Grayscale's converted ETHE trust bled $484M on day one alone, overwhelming everything the new entrants were pulling in, and forcing the market into four months of net outflows before demand finally caught up.

It looked like an exact repeat of what Bitcoin had experienced with GBTC, leading to the industry assumption that once the Grayscale overhang exhausted itself, a massive, unencumbered institutional bid would emerge.

Then came July and August 2025, an explosive two-month window where BlackRock's ETHA alone pulled in $4.2B and $3.38B in back-to-back months. Even when compared to Bitcoin's early trajectory, this surge suggested that the institutional demand thesis was entirely correct. For a moment, it looked like ETH was becoming ultrasound money. It wasn’t.

Those two months proved to be a cyclical ceiling, and what late May 2026 reveals is something far more uncomfortable than a simple price drawdown. Grayscale's bleeding has effectively ground to a halt; ETHE is posting minimal outflows on most days. Yet the rotation that was supposed to naturally follow, with capital migrating from the expensive Grayscale product into cheaper alternatives like ETHA or FETH, has failed to materialize.

Competitors like Bitwise, VanEck, Invesco, and Franklin are registering consecutive strings of absolute zeros, while even BlackRock's dominant ETHA spent most of May posting outflows. The lack of an institutional bid coupled with low burn rates at the protocol level has seen the price of ETH struggling to stay above $2,000.