Eyes on the Market, Volume 2: Game of Flows

Updated On 31 December 2025

Published On 3 December 2025

TL;DR

- Bitcoin just had a “Sunday slam” — a ~5% drop to ~$86,900 in three hours, wiping out $539M in long liquidations and locking in Bitcoin’s worst November since 2018.

- BTC dominance is rising above ~58–60% as capital retreats from alts and ETF / treasury / stablecoin demand flips into outflows, but NYDIG argues the long‑term institutional/sovereign thesis is intact – this is a liquidity loop reset, not a fundamental break.

- The Fed’s December rate cut is back on the table, with markets pricing ~75–85% odds for a 25 bps cut, helping risk assets but also pushing stablecoin issuers like Tether further into an “interest‑rate trade” on BTC and gold.

- Stablecoin structure is under the microscope: Tether’s larger BTC/gold allocation boosts upside but also makes its equity sensitive to a 20–30% drawdown, while exchange stablecoin reserves are at record levels and stablecoin-vs-coin ratios at historical extremes — a lot of liquidity is sitting on the sidelines.

- SEC’s revised 2025 plan points toward clearer, more structured digital‑asset rules, a medium‑term positive for compliant, institutional‑grade platforms.

- Solana’s run cools at the margin: after 22 straight days of inflows, Solana ETFs posted an $8.2 million net outflow, led by 21Shares — a pause, not a collapse, but the first sign that “always up” ETF flow is over.

- DeFi risk and DeFi buildout in one week: Yearn’s legacy yETH product was hit by an “infinite mint” exploit that drained roughly $2.8-9 million, while DWF Labs announced a $75 million DeFi fund aimed exactly at fixing on‑chain liquidity, money markets and yield infrastructure for the institutional phase of DeFi.

Sunday Slam: Leverage Gets Cleaned Out (Again)

Over the weekend, Bitcoin traded quietly around $91,500 — until it didn’t. In roughly three hours on Sunday, BTC slid nearly 5% down to around $86,950, with no clear news catalyst.

The move triggered about $539 million in liquidations across crypto, hitting more than 180,000 traders, with almost 90% of the wiped positions being leveraged longs, largely in BTC and ETH.

Despite the drama, this looks less like “new information” and more like market infrastructure doing what it always does when leverage builds up in thin weekend liquidity:

- A rush of selling hits a shallow book

- Liquidation engines kick in

- Forced selling amplifies the move

- Then things calm down

The constructive take — and one we agree with — is that this is a structural flush. A chunk of leverage is gone, downside liquidity has been tested, and the market starts December with a cleaner base. That doesn’t mean we’re “bottomed,” but it does mean the next leg lower, if any, likely needs a fresh catalyst, not just fragile longs.

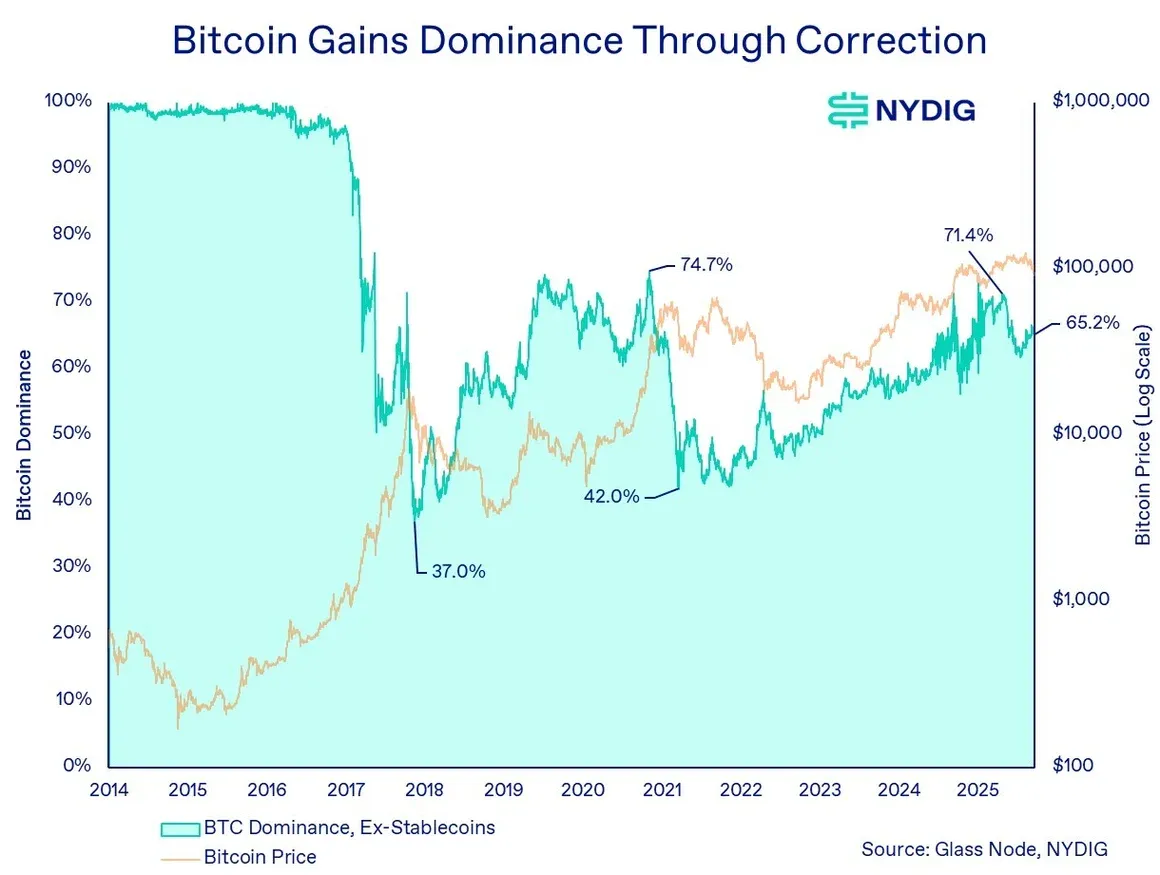

BTC Dominance and NYDIG: Demand Engines in Reverse, Story Intact

NYDIG’s latest note frames what just happened in BTC as a classic reflexive unwind:

- The same engines that pushed BTC to its October peak — spot ETF inflows, digital‑asset treasury (DAT) buying, and expanding stablecoin supply — have now flipped into outflows and contraction.

- ETF flows turned from steady buyers into a meaningful headwind, DAT premiums compressed, and stablecoin supply ticked down. NYDIG calls this “actual capital flight,” not just bad vibes.

At the same time, Bitcoin dominance climbed back above 60%: crypto capital hides in the most liquid, most established asset while high‑risk altcoins take the real beating.

NYDIG’s key point, which we share, is this is a cycle dynamic, not a thesis break.The main appeal of Bitcoin (institutional adoption, sovereign interest, BTC as neutral monetary asset) is untouched.What is broken for now is the liquidity loop that was pulling fresh capital in.

It is wise to interpret the current environment as “late‑cycle fragility” rather than “Bitcoin is dead again.” Bitcoin dominance is typically what you see when market participants de‑risk but are not leaving cryptocurrencies as an asset class entirely.

And to zoom out even further: a new Glassnode/Fanara report shows Bitcoin attracted $732 billion in new capital this cycle.

Macro Backdrop

Macroeconomy is quietly turning supportive again. Futures markets are now pricing roughly 75-85% odds of a 25 bps Fed cut in December 2025, up sharply from around 40% a week earlier, as labor data softens and inflation cools.

That shift helped U.S. tech stocks to their biggest daily gain in six months, with the Nasdaq up ~2.7% on November 24, 2025, as rate‑sensitive growth names ripped higher.

For crypto, a credible December 2025 cut does three things:

- Reduces the appeal of Treasuries (less yield to park in cash).

- Improves the discounted cash flow (DCF) on long‑duration assets like BTC and high‑growth tech stocks.

- Feeds the “liquidity is coming back” narrative that historically helps flows into ETFs and on‑chain capital.

But, as we see with Tether below, a lower‑rate world also forces stablecoin issuers and treasuries to reach further out on the risk curve to maintain returns.

Stablecoins: Tether’s Rate Trade and Record Stablecoin Exchange Balances

Tether’s BTC and Gold Bet

Arthur Hayes’ latest note zeroes in on Tether’s reserve mix. Based on the most recent attestation, Tether now holds roughly:

- $181 billion in total assets, mostly in cash and liquid securities.

- ~$10 billion in Bitcoin.

- ~$13 billion in precious metals (primarily gold).

- over $14 billion in secured loans and other investments.

Hayes’ read: Tether is front‑running a Fed easing cycle, accepting that T‑bill income will fall if rates are cut, and compensating by loading up on BTC and gold, which they expect to outperform as “the price of money” drops.

The risk is symmetric:

- If BTC and gold rip higher into rate cuts, Tether’s equity balloons.

- If BTC and gold drop by ~30%, Hayes argues Tether’s equity could be largely wiped, re‑opening the USDT solvency debate.

The S&P agency already gave USDT a “weak” stability rating, explicitly flagging growing exposure to volatile assets as a vulnerability under stress.

USDT still functions as core liquidity, but risk systems should increasingly underwrite it as cash plus embedded macro call options: you’re not just holding dollars; you’re implicitly long Tether’s balance‑sheet management.

However, a former Citi research crypto lead offers a counter-thesis to Hayes’ argument. The core pushback: Tether’s disclosed reserves are only one slice of its corporate balance sheet, and not the slice that determines whether the firm can absorb a drawdown. In particular:

- Disclosed reserves do not span all corporate assets. Tether’s attestations only show matched reserves and exclude a far larger corporate balance sheet: equity holdings, mining assets, and retained earnings that could absorb losses long before solvency is threatened.

- The equity is lucrative and can be monetized. Given Tether’s annual profit engine of about $10 billion from Treasuries and small costs, its equity is highly valuable and could be sold or tapped to recapitalize in any reserve-portfolio drawdown.

- Traditional banks operate with much smaller buffers. Compared with traditional banks that hold just 5-15% of deposits in liquid assets, Tether is substantially more collateralized.

Thus, Tether is not close to insolvency, but is instead operating a high-margin, structurally advantaged “money-minting machine”.

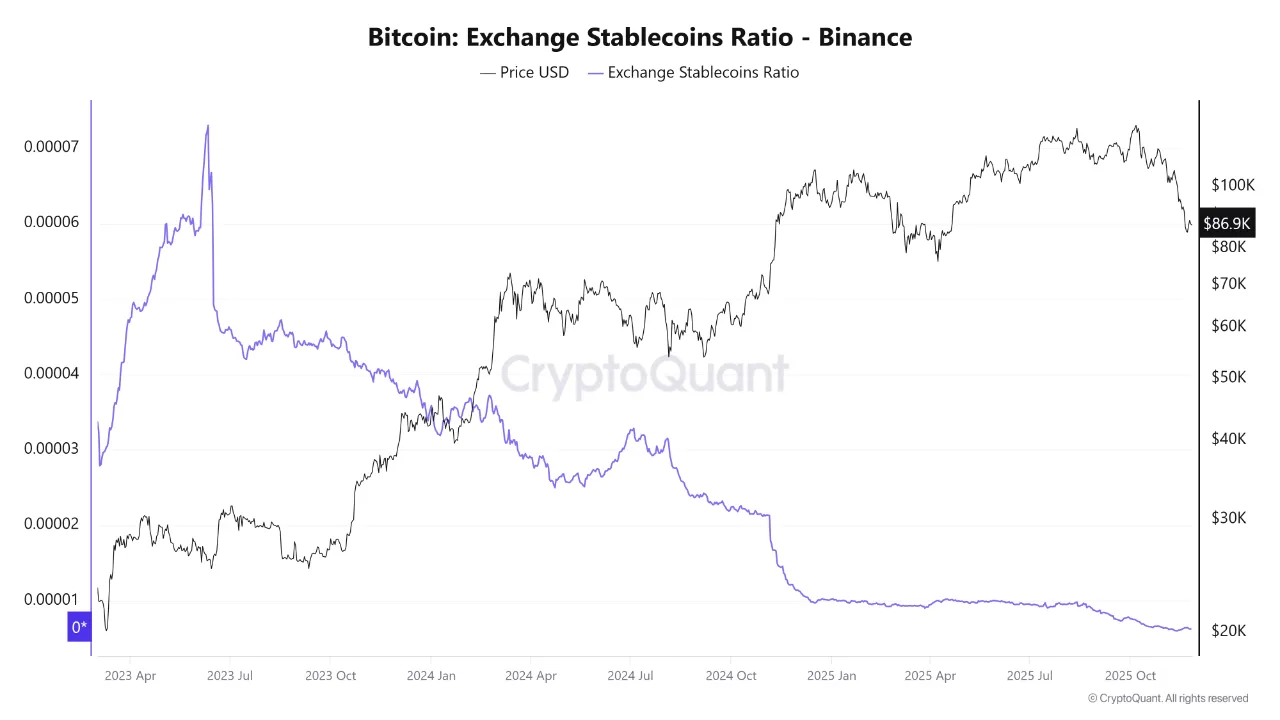

Exchange Stablecoins: Record Ammo, Thin Conviction

On exchanges, the picture is the mirror image of price. CryptoQuant’s metric called Exchange Stablecoins Ratio (exchange balances of stablecoins vs major coins) is at or near its lowest level on record, which in practice means a lot of buying power relative to available crypto.

Binance alone is estimated to hold around $50-51 billion in stablecoins, an all‑time high, even as BTC and ETH balances on the exchange are down sharply.

What it means:

- Investors have not left — they’ve rotated into stablecoins.

- There’s plenty of liquidity on the market right now, but it’s waiting for better entry points and clarity.

Historically, this combination: falling BTC on‑exchange, plus rising stablecoin balances has appeared before major upside legs, but timing is messy.

Treat this as an environment where “locked and loaded” doesn’t mean “firing now.” Size positions assuming that stablecoin ammo can either rush in on any convincing bullish catalyst, or sit sidelined for months if macro or regulation throws another curveball.

Yield-Bearing Stablecoins

Yield-bearing stablecoins have been on a decline, and lowering interest rates and volatility in the market are among the primary causes. Stablecoins that solely rely on T-bill rates will likely be affected deeply, with the high possibility of Fed rate cut at the end of 2025.

However, it won’t likely end yield-bearing assets. Instead, other projects with more flexible and diversified earning models could likely absorb idle liquidity in case they can offer more competitive yield rates, coupled with robust transparency and risk management systems.

One of such candidates is Falcon Finance: it managed to grow the supply of its USDf synthetic dollar by about $400 million since October, demonstrating the community values its offering, which remains competitive even in the bearish crypto market.

Regulation: SEC’s 2025 Plan Shifts from Fog to Framework

On the crypto policy front, the U.S. SEC’s revised 2025 plan is an under-priced story. Published in late November 2025, it explicitly calls for:

- Clearer rulemaking and examination priorities around digital assets

- More consistent treatment of tokenized products

- A focus on investor protection plus market integrity, not just enforcement

For builders and institutions, that matters.Startups get a clearer legal map, which can reduce the “should we just build offshore?” pressure. Larger allocators can justify internal green‑lights for onshore, compliant products once rules and supervisory expectations are better defined.

This doesn’t magically make the SEC “pro‑crypto”, but it does look like a step away from regulation by lawsuit and toward regulation by rulebook, which is exactly what institutional capital has been waiting for.

Flows: Solana ETF Streak Finally Breaks

One clean, high‑signal data point this week: Solana ETF flows blinked.

- After 22 straight days of net inflows, Solana ETFs recorded their first net outflow: about $8.1-8.2 million in a single day, driven entirely by the 21Shares product (TSOL), while other SOL ETFs still saw modest inflows.

- That streak had turned Solana into a standout “institutional alt” during the recent drawdown.

- A single $8 million outflow doesn’t change the core thesis, but it does tell you that even the strongest narratives are flow‑sensitive when volatility picks up.

Think of this as “pause after chase”, not rotation out of Solana. If BTC stabilizes and regulation stays constructive, SOL will likely remain a preferred high‑beta expression. But the easy “every day green” phase for the ETFs is probably behind us.

Risk Watch: Yearn’s yETH Infinite‑Mint Exploit

On the DeFi risk side, Yearn Finance’s yETH product suffered a textbook “infinite mint” attack on November 30:

- An attacker exploited a vulnerability in the legacy yETH token contract, minting an absurd ~235 trillion yETH in a single transaction.

- Using those fake tokens, they drained Balancer pools of ETH and liquid staking tokens, with estimated losses in the $2.8-9 million range depending on the source.

- Around 1,000 ETH (~$3 million) was quickly routed through Tornado Cash with additional assets remaining in the attacker’s wallets.

- Crucially, Yearn’s V2 and V3 vaults were not affected: the blast radius is limited to the older yETH implementation.

The bigger lesson: even “blue‑chip DeFi” still carries idiosyncratic smart‑contract risk, especially in legacy code paths and exotic pools. This reinforces the need to treat DeFi exposure as credit with a tech risk on top, not just “yield with composability”.

DeFi’s Institutional Phase: DWF Labs’ $75 Million Fund

Against that backdrop, DWF Labs stepped in with a structural bet on what comes next: the firm announced a $75 million DeFi fund, explicitly framed as capital for the institutional phase of DeFi.

The fund focuses on teams building:

- Dark‑pool perpetual DEXs

- Decentralized money markets

- Yield‑bearing protocols

- Across Ethereum, BNB Chain, Solana, and Base blockchains

As Andrei Grachev put it, DeFi is now “entering its institutional phase”, and the infrastructure has to actually work at size: handle big tickets, protect flow, and unwind cleanly when conditions change.

Why this matters:

- We just saw leveraged crypto perps, fragile liquidity, and synthetic risk contribute to another sharp flush.

- We also saw Tether, ETFs, and sovereign/treasury flows prove how dependent crypto has become on “institutional” structures.

- DWF Lab’s fund is essentially a bet that the next leg of growth will come from DeFi rails that look and feel closer to traditional market infrastructure: dark pools, robust money markets, and proper fixed‑income primitives.

This is the direction of travel if crypto wants to graduate from speculative cycles into durable, institutional capital markets on‑chain.

So What Now?

This is “Game of Flows,” not Game of Narratives. Downside tails are still alive (Tether, more ETF outflows, policy surprises), but so is the upside if even a fraction of the current stablecoin and ETF liquidity rotates back into beta under a friendlier Fed and clearer rules.