Eyes on the Market: From Concept to Rails

Published On 2 April 2026

The past two weeks offered one of the clearest examples yet of a pattern that has been defining this cycle: crypto infrastructure is maturing faster than the market is pricing it.

Tokenized stocks crossed $1 billion in on-chain value for the first time. Solana's stablecoin supply reached a record $17 billion, with Stripe, Visa, PayPal, and BlackRock routing real payment volume through it. DeFi protocols moved further toward distributing actual revenue to token holders. A new primitive connecting AI agents to on-chain identity and stablecoin payments launched. And the SEC and CFTC jointly classified 16 crypto assets as digital commodities, providing the clearest jurisdictional map the industry has received.

Bitcoin traded between $65,015 and $75,991 and sits around $67,749 as of March 30. The market is in a consolidation phase. But the rails underneath it are not slowing down.

Tokenized Assets: The Numbers Behind the Narrative

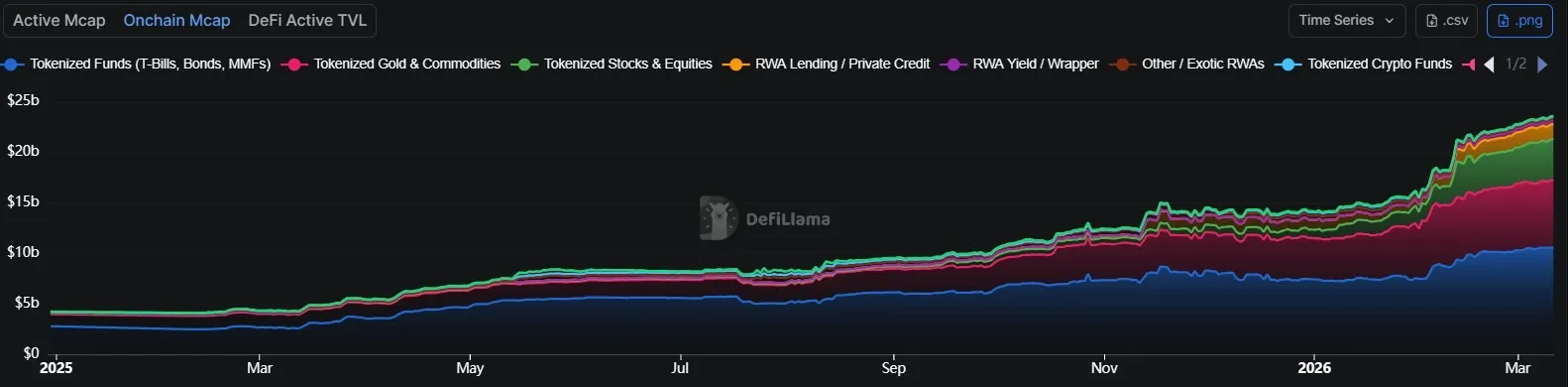

The on-chain RWA market reached $26.48 billion as of March 23, up 5.25% in 30 days and 66% year-to-date, from $14.1 billion in January . Total asset holders reached approximately 694,000, growing 6% month-on-month. The growth is broad-based, spanning treasuries, private credit, equities, and commodities.

Within that, a few milestones stand out.

- Tokenized stocks surpassed $1 billion, with Ondo and xStocks accounting for the largest share. This is meaningful because tokenized equities require a different infrastructure layer than tokenized bonds or stablecoins: real-time pricing feeds, corporate action handling, and cross-jurisdictional compliance. The fact that this category has reached $1 billion suggests the infrastructure is now functional enough to support it at scale.

- The tokenized U.S. Treasury market reached $11.13 billion in March, up from $10 billion in February. BlackRock's BUIDL fund remains the largest product at $1.9 billion.

- An RWA.xyz spokesperson told Cointelegraph that the current phase is driven less by tokenization as a concept and more by distribution, market access, and assets that trade and settle around the clock. In other words, the product-market fit conversation has shifted from "can this work?" to "how do we distribute it?"

- On March 25, the House Financial Services Committee held a hearing titled "Tokenization and the Future of Securities", the most significant congressional examination of tokenized assets to date. During the same week, senators reached a deal "in principle" on the CLARITY Act's stablecoin yield language.

Stablecoins as Infrastructure

Solana's on-chain stablecoin supply crossed $17 billion in March, a record. What is notable about this figure is the composition of participants driving it. Stripe, Visa, PayPal, and BlackRock have all integrated with Solana for cross-border payments and asset tokenization. This is commercial adoption from companies that collectively process trillions in annual payment volume.

Ethereum continues to host over 60% of all tokenized RWAs by value, maintaining its position as the primary settlement layer for institutional tokenized products. The dynamic between the two networks reflects a broader trend: Ethereum as the institutional settlement layer, Solana as the high-throughput transaction layer. Both are growing stablecoin supply, but through different use cases and user profiles.

The broader stablecoin market is now well above $300 billion in total supply. What started as a trading utility has evolved into payment infrastructure. Cross-border settlement, payroll, and merchant payments are now live use cases running on stablecoin rails.

DeFi: From Governance to Yield Infrastructure

The broader shift in DeFi, however, goes beyond fee distribution. As DWF Labs Managing Partner Andrei Grachev wrote in CoinDesk this month, the real institutional unlock is not digitizing assets but financializing yield. Tokenized Treasuries or equities are only marginally useful if they behave like static certificates. What institutions require is the ability to deploy tokenized assets as functioning collateral, isolate and trade yield independently of principal, and integrate positions into broader strategies without breaking compliance constraints.

That is the transition from first-order tokenization to second-order yield markets. Early design patterns are already emerging: hybrid structures where permissioned, regulated assets serve as collateral while borrowing happens through permissionless stablecoins and open liquidity pools. Yield trading architectures are separating principal exposure from yield streams, making hedging, duration management, and structured products feasible on-chain.

As Grachev noted, tokenization was phase one because it proved assets could live on-chain. Phase two is about making those assets behave like real financial instruments. When that transition matures, the conversation shifts from crypto adoption to capital markets migration.

AI Meets On-Chain Identity

Sam Altman's World project launched AgentKit during the period, a toolkit that allows AI agents to carry cryptographic proof of human identity through World ID. It integrates with Coinbase and Cloudflare's x402 protocol, creating a layer where AI agents can make stablecoin micropayments while proving they act on behalf of a verified human.

The timing matters. As AI agents begin executing transactions autonomously, whether shopping, booking, or settling, the question of identity and verification at the protocol level becomes a prerequisite for scale. Coinbase founder Brian Armstrong said he expects there will "very soon" be more AI agents than humans making transactions. If that trajectory holds, the intersection of on-chain identity and stablecoin payments becomes foundational infrastructure, not an edge case.

Regulatory Context

On March 17, the SEC and CFTC issued a joint 68-page interpretive release classifying 16 crypto assets as digital commodities, including Bitcoin, Ethereum, Solana, and XRP. Staking, mining, and airdrops were classified outside securities law. The release also established a five-category token taxonomy.

The interpretation awaits the CLARITY Act for statutory force. The Act passed the House in July 2025 and the Senate Banking Committee markup is the next step.

For the infrastructure thesis, the regulatory development is relevant because it reduces the jurisdictional ambiguity that has historically slowed institutional adoption of on-chain products. Clearer classification enables faster product development, broader distribution, and deeper integration with traditional financial systems.

Overall

The past two weeks reinforced a theme that has been building throughout early 2026. Tokenized assets, stablecoin infrastructure, DeFi revenue distribution, and AI-to-crypto connectivity are all progressing on their own timelines, independent of price action. The on-chain economy is developing the characteristics of functional financial infrastructure: real assets, real settlement, real payment volume, and increasingly, real regulatory frameworks to support them.

This commentary is for informational purposes only and does not constitute investment advice.

%20(5)-960x540.webp?prefix=media)