Tokenized Stocks Explained for Beginners: A Guide to the Next Market Revolution

Updated On 31 October 2025

Published On 30 October 2025

Tokenization is an infrastructure upgrade, which keeps familiar investor protections while moving key operations to programmable, always-on systems. That is one, yet not the single, reason for tokenization of the stock market gaining momentum in 2025. Read this article to learn why tokenized shares are gaining traction across retail brokerages, policy circles, and institutional finance at the same time.

What Tokenized Stocks Are and How They Work

Tokenized stocks are digital instruments issued on a blockchain that provide economic exposure to a stock or exchange-traded fund (ETF). Today’s market uses two main structures:

- In a fully backed model, a regulated entity holds the underlying shares, typically via a custodian or special-purpose vehicle (SPV), and issues tokens that mirror those shares one-for-one.

- In a reference or derivative model,the token mirrors a company’s price but doesn’t grant direct ownership. Instead, its value is tied to market prices or to contractual rights held by a special-purpose vehicle (SPV).

A concrete example illustrates the mechanics. In June 2025, Robinhood launched tokenized access in the EU to more than 200 U.S. stocks and ETFs, enabling 24/5 trading with zero commissions, and reported a stock-price jump around the announcement. The platform emphasized on-chain settlement, auditability, and a blend of traditional-finance (TradFi) protections with blockchain speed. Regulators quickly engaged: the Bank of Lithuania requested additional details around private-company tokens, while the firm reiterated its view that those instruments fit within MiCA and MiFID as derivatives rather than direct equity.

Why the Conversation About Tokenized Stocks Is Accelerating

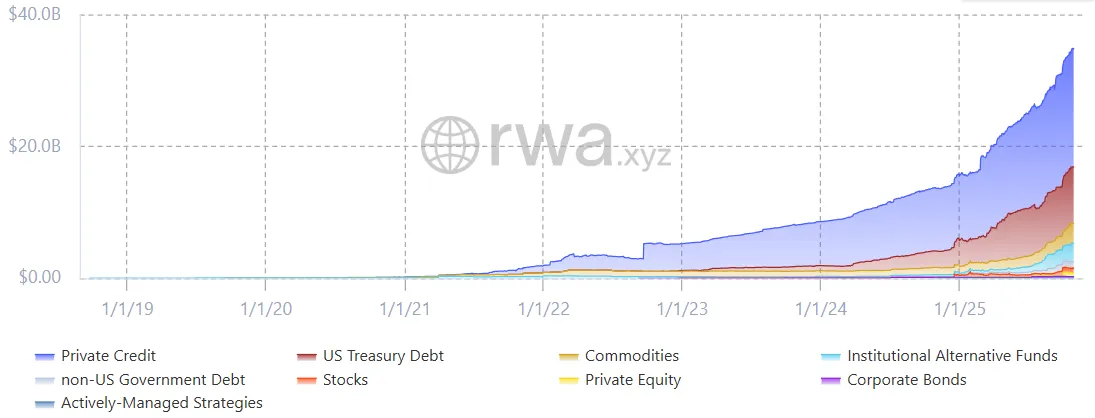

In the new narrative, two forces are converging. First, the on-chain real-world assets (RWA) market has become material: in 2025 alone, total RWA value gained over 120%, surpassing the $34 billion mark in October and bringing tokenized treasuries, money markets, and equity exposures into mainstream view.

Second, industry voices argue for supervised experimentation, i.e. regulated sandboxes where custody, disclosure, and auditability can be tested end-to-end before locking rules into place. This approach aims to prevent “regulation by denial” at the very moment adoption is compounding.

Benefits of Tokenized Stocks Beyond the Buzzwords

Some headline advantages of tokenized stocks are familiar: fractional access, longer market hours, and faster settlement. However, what matters is how those features interact:

- fractionalization lowers the ticket size to blue-chip exposure;

- extending trading beyond market hours makes that access usable across time zones;

- putting settlement and audit trails on-chain increases operational transparency.

Once these tokens exist on a blockchain, they can connect to lending platforms and other investment tools, so investors can use tokenized equities as collateral and build portfolios that were previously available only to large accounts. This allows investors, retail and institutional, to post tokenized stocks as collateral and to compose portfolios with tools that were previously gated to large accounts.

While mainstream brokers like Robinhood move to launch stock-based token inventories, decentralized finance (DeFi) is building infrastructure that makes composability real. For example, Aave Labs’ Horizon now lets institutions borrow stablecoins against tokenized RWAs like U.S. Treasuries, pointing to a pathway for collateralized portfolios that could include equity exposures as regulatory clarity expands.

And traditional market operators are taking notice: just recently, Nasdaq has requested to allow tokenized securities on its main market, signaling that on-chain settlement and auditability are being integrated into familiar venues rather than left to the periphery.

Convergence Between TradFi and Crypto

The tokenized stocks market is expanding rapidly, bridging traditional finance (TradFi) with the crypto ecosystem. Below are several recent examples of how tokenized equities are being added to crypto-native applications and protocols:

- At the end of October 2025, Falcon Finance announced the integration of xStocks from Backed, enabling users to use tokenized shares and ETFs of leading companies as collateral. The list of accepted Backed tokens includes Tesla ($TSLAx), NVIDIA ($NVDAx), Strategy ($MSTRx), Circle ($CRCLx), and SPDR S&P 500 ($SPYx), alongside a range of other digital assets such as Tether Gold ($XAUt), Superstate’s tokenized U.S. Treasuries ($USTB), popular stablecoins ($USDC, $USDT), and major cryptocurrencies ($BTC, $ETH, $SOL). Falcon Finance users can now deposit xStocks into the app to mint $USDf synthetic dollars, which can then be staked to earn on-chain yield, turning tokenized equities into productive, yield-bearing assets.

- Earlier in the same month, Backpack partnered with Superstate to integrate Opening Bell, bringing SEC-registered U.S. equities natively on-chain for eligible non-U.S. users within Backpack’s wallet and exchange. The partnership makes Backpack the first centralized exchange to support SEC-registered equities that live directly on-chain (initially on Solana) rather than as synthetic wrappers. These tokens carry the same CUSIP identifiers and preserve shareholder rights such as dividends and voting. Superstate provides the transfer-agent and issuance infrastructure, while Backpack handles distribution and trading alongside crypto and stablecoins in a unified interface.

- In September 2025, Blockchain.com integrated Ondo Global Markets, allowing users outside the U.S. to access tokenized U.S. stocks and ETFs, including major tickers such as Tesla (TSLA) and NVIDIA (NVDA), directly through Blockchain.com’s crypto wallet. The tokens behave like other crypto assets, remaining accessible in self-custodial wallets and usable across DeFi platforms, with Chainlink oracles supplying real-time pricing and settlement data.

Together, these integrations mark a turning point in how traditional equities interact with the crypto world, signaling a future where stocks trade, earn yield, and move seamlessly across blockchains.

The Hard Problems

Tokenization changes legal definitions, market infrastructure, and investor protections that were built for paper-era securities. The result is a set of challenges that are less about cryptography and more about governance, in particular:

- Classification and venue rules. Jurisdictions differ on whether a token is the security itself, a depositary-style receipt, or a derivative. The answer dictates licensing and conduct requirements. The EU’s early cases around private-company tokens have leaned derivative, while in the U.S., if a tokenized equity fully mirrors ownership rights (dividends, voting), then the token could be treated as the security.

- Policy uncertainty in key markets. Where rules reshape mid-century statutes to modern rails, institutions hesitate. By contrast, Europe’s MiCA reduces uncertainty for crypto-assets outside existing securities law, while tokens that meet MiFID’s financial-instrument tests remain in the traditional regime.

- Corporate-actions processing. Dividends, splits, proxy voting, and updates to the shareholder register must flow cleanly from issuer registries to token holders. This is straightforward in fully backed models and more complex for reference tokens, which mirror price exposure but not necessarily shareholder rights. The engineering task spans both smart contracts and off-chain legal agreements.

- Market integrity and inclusion. Wealth-based accreditation regimes can cordon off early-stage exposure for retail investors, risking a future in which tokenization widens access technically but not legally. That tension is a recurring theme in industry commentary and policy debates.

Regional Outlook: Where Tokenized Stocks Are Poised to Scale First?

Within the global RWA market, two regions are at the forefront of integrating tokenized securities, including stocks, into the broader economy.

In Asia, financial authorities are pioneering structured, regulator-led environments that test tokenization under real conditions, establishing frameworks that blend innovation with oversight. The Hong Kong Monetary Authority (HKMA) develops the Project Ensemble Sandbox that connects banks’ tokenized-deposit platforms and is explicitly designed to test PvP/DvP settlement for tokenized assets with wholesale-CBDC in the loop. In parallel, the Securities and Futures Commission (SFC) has operational guidance for tokenized securities, giving intermediaries a supervised path to market. Meanwhile, the local digital bond market has seen new offerings.

In Singapore, MAS’s Project Guardian is the archetype of a supervised, multi-party pilot program: by June 2024 it had 24 global financial institutions testing tokenisation across fixed income, forex, and fund tokenisation, and it rolled out the Global Layer One (GL1), a public-private effort to define a shared-ledger standard with BNY, Citi, J.P. Morgan, MUFG and SG-Forge involved.

Meanwhile, in the U.S., policymakers and infrastructure providers are building the legal and operational foundations for large-scale adoption, from the new federal stablecoin framework to on-chain settlement pilots and regulated venues preparing for tokenized stocks and other assets.

In particular, DTCC’s “Smart NAV” pilot, conducted in 2024 with Chainlink alongside major financial institutions such as J.P. Morgan, Franklin Templeton, and BNY Mellon, showed how to broadcast fund data on-chain, marking an essential step for tokenized funds, and DTCC subsequently announced a tokenized collateral platform for real-time use cases.

But on equities, uncertainties in the applicable rules still bite: Commissioner Hester Peirce has flagged custody and classification frictions (e.g., how crypto-asset security intersects with broker-dealer obligations), and leading law firms stress that despite a regulatory thaw, developers must still navigate unsettled tokenized-security questions. At the same time, Nasdaq’s filing with the SEC to permit tokenized securities trading on its markets showed some signs of acceleration.

Future Scenarios for Tokenized Stocks

Current pilots and sandboxes for tokenized stocks in Europe, Asia and the United States will lead to playbooks: standardized disclosures, attestation routines, and event-handling templates, that supervisors can lift into permanent rulemaking.

Hybrid brokerages then will start bundling features: tax-lot tracking, corporate-action alerts, dividend reinvestment options and one-click use of holdings as collateral. In the background, issuer agents and registrars expose APIs that sync smart contracts with off-chain shareholder registers, reducing reconciliation work and cutting settlement exceptions.

On the collateral side, risk teams calibrate haircuts (risk-based discounts to collateral value) and maximum exposure limits to a single asset for tokenized positions, first in bilateral arrangements and then in broader programs, while institutional DeFi venues adopt pre-approved connections and on-chain attestations of asset backing to satisfy compliance. The net effect is a slow convergence, with tokenization gradually becoming a baseline for the stock market.

Closing Thoughts

For investors and institutions, tokenized equities deliver broader access (fractional, extended-hours markets), faster and more transparent settlement, and programmable systems that cut costs while unlocking new collateral and portfolio uses.

The continuous merger between TradFi and crypto throughout 2025, underlined by a growing wave of integrations, such as Falcon Finance enabling xStocks from Backed as collateral or Backpack offering SEC-registered shares through Superstate, illustrates how tokenized stocks are becoming active components of the onchain financial infrastructure.

A regulated-sandbox approach, long advocated by industry leaders, offers the most credible route to scale. If platforms pair clear legal structures with supervised pilots, the next phase will be defined less by headlines and more by standardized processes that let tokenized stocks fit into familiar apps and balance sheets.

The most likely outcome is gradual convergence: the word “tokenized” fades, while the benefits—broader access, faster settlement, and flexibility thanks to the digital nature—remain.

-960x540.webp?prefix=media)