Evolution of RWAs: Perpification and 24/7 Markets

Published On 31 March 2026

Key Takeaways

- Perpification and tokenization serve fundamentally different audiences: The latter upgrades capital markets for institutions, while the former democratizes access for retail traders through synthetic, permissionless, and self-custodial exposure to real-world assets.

- A retail speculation supercycle is underway: Gen Z traders, priced out of traditional wealth-building practices, contribute to record derivatives volumes globally. Onchain perp DEXs are the product best positioned to meet this demand.

- RWA perps are already gaining serious traction: HIP-3 markets have driven over $130 billion in cumulative volume since launch, with over 2.2 million unique traders and $1.7 billion in open interest, over 90% of which comes from RWA-related markets.

- The oracle problem is the main technical challenge: Pricing traditional assets 24/7 without a continuous regulated reference price forces platforms to choose between capital safety and market availability, shaping their entire product architecture.

- 24/7 regulated markets are a double-edged sword: Moves by NYSE and ICE toward continuous trading will improve oracle quality and attract market makers to onchain venues, but also narrow the window for crypto-native platforms to differentiate before regulated alternatives arrive.

- RWA perpification may become crypto’s second great export: Just as perpetual futures became the dominant non-spot primitive in crypto, RWA perps are on track to become foundational infrastructure for global retail derivatives access.

Tokenization vs. Perpification

While the concepts of RWA tokenization and perpification have been discussed and debated greatly, it simply comes down to who each process is for and what it’s actually good at.

Tokenization is a process that involves the upgrading of capital markets, and building a better version of traditional finance. This comes with benefits like real-time settlement, fractional ownership, programmable smart contracts, while still allowing holders to maintain full ownership of underlying assets. However, being largely championed and built for institutions, retail users become a secondary concern. As it stands, most tokenized real-world assets still live in permissioned platforms rather than open DeFi, inheriting similar access barriers such as KYC requirements, brokerage relationships, jurisdictional and geographical blockers, which resulted in the exclusion of retail investors in the first place. Tokenization promises a fairer financial system, but largely delivers it to asset managers, hedge funds, and other institutional investors.

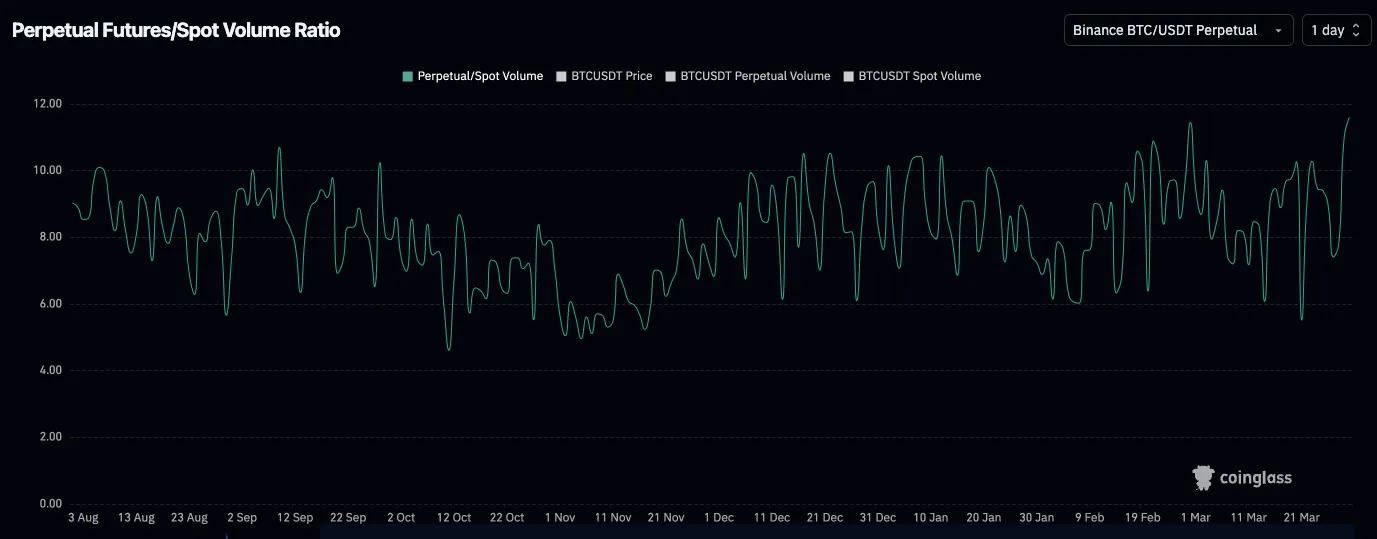

Perpification starts from the opposite end. Popularized by Kaledora (cofounder of Ostium), the process involves the utilization of a perpetual swap or futures-first approach to onboard traditional and non-crypto-native assets onto the blockchain. Synthetic by design, there is no ownership or custody of the underlying which avoids the need to navigate legal scaffolding. Combined with its ability to be created on top of any asset with a reliable price feed, perpetuals have become the fastest and most frictionless way to bring new assets on-chain. As evidenced by the recent influx of new perps products, such as equities, commodities, and even pre-IPO companies. The result is a product optimized for retail investors, who are now able to take directional price views on various assets with leverage and no expiry, all in a capital efficient, self-custodial, and permissionless manner. This is also why perps in general have become the dominant non-spot primitive in crypto by a wide margin. BTC perpetual volumes in crypto already exceed spot volumes by anywhere from six to eleven times, a direct indicator to where user demand actually sits.

The Structural Shift

This demand is not an anomaly, it is a leading indicator of a much larger structural shift. We are in the midst of a retail speculation supercycle, where retail accounted for more than half of U.S. options volume in 2025, and CFD volumes hit record highs with three brokers each reporting monthly volumes exceeding $1 trillion. Gen Zs have entered financial markets not with the buy-and-hold mindset of their parents, but with a fundamentally different relationship to risk. This is shaped by a world where traditional wealth-building paths like property ownership feel structurally out of reach, where the logic of modest and consistent compounding over 40 years is simply not good enough anymore. The rational response for a generation priced out of conventional asset accumulation is to engage in high-conviction, high-leverage bets. This isn’t irrational behaviour, but a coherent response to circumstances and a breaking system.

Syncracy frames this directly: rising costs of living, lack of social mobility, and the sheer accessibility of speculation via mobile phones have together produced a generation of traders for whom leverage isn't a warning label but a baseline assumption. Onchain perp DEXs are the product that meets them where they are, removing the cognitive overhead of options (expiry dates, time decay, implied volatility) and delivering intuitive directional exposure that is purpose-built for the way this generation actually wants to trade. Tokenization offers a fractional share of a BlackRock money market fund yielding 5% per annum, while perpification offers traders a potential ticket to early retirement. The PMF gap between these two products, for this audience, could not be wider.

Onchain Adoption and Relevance of RWA Perps

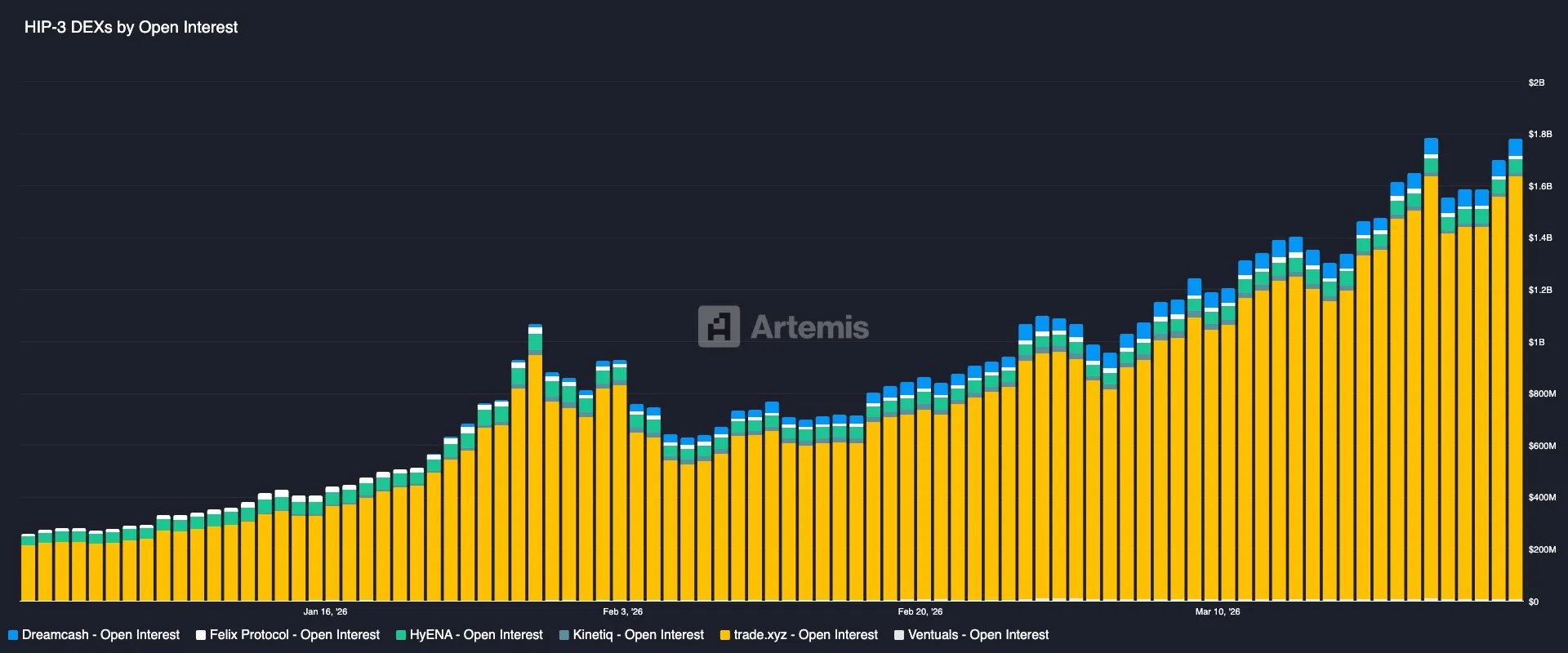

Onchain traction of RWA perps has already been on a rise. The launch of Hyperliquid’s HIP-3 in October 2025 served as a key inflection point, unlocking the permissionless deployment of perpetual futures markets on the platform and resulting in over 100 different RWA markets being launched across equities, commodities, indices, FX, and even pre-IPO companies. These new markets have already driven over $130 billion in cumulative volume since inception. As of late March 2026, total open interest across all HIP-3 DEXs and markets has grown to $1.7 billion, with RWA-related markets contributing over 90% of that total, with BRENTOIL and CL markets contributing to $295 million and $208 million respectively.

The number of unique traders on HIP-3 have also followed in similar fashion, now over 2.2 million cumulatively.

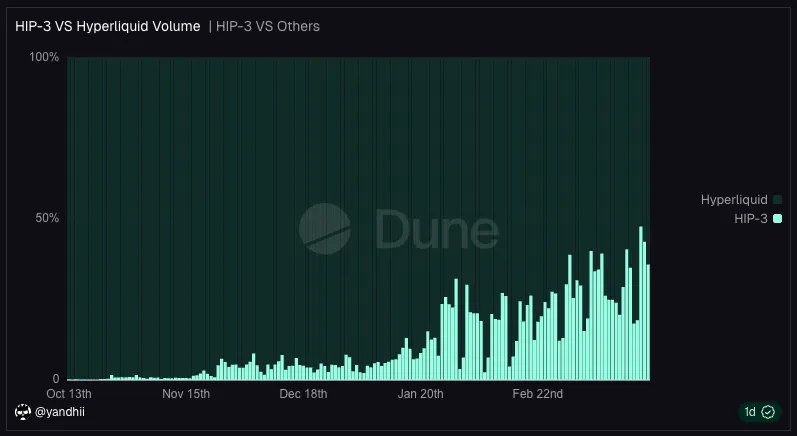

The share of overall Hyperliquid volume attributable to HIP-3 markets has also been climbing steadily, peaking at over 40% of total daily volume in early March 2026. Commodities form the largest share, as geopolitical tensions between the U.S. and Iran escalated on the weekend of February 28, 2026, Hyperliquid’s crude oil market experienced an influx of traders looking to gain exposure to market volatility. Furthermore, analysts at JPMorgan indicate that this influx was driven almost entirely by non-crypto traders who were left without options due to the closure of traditional markets, demonstrating the growing reach and appeal of the onchain perp DEX and its 24/7 offerings. This even led to the market’s peak daily trading volume of $1.7 billion.

As the second largest RWA perps platform by volume, Ostium has also carved out its share of the market. The platform has processed approximately $46 billion in cumulative volume across over 25,500 traders, with anywhere between 85-95% of open interest concentrated in markets for traditional assets like equities, commodities, indices, and FX. Total open interest has ranged between $160 million and $320 million over the past two months, with commodities forming the largest share of activity similar to Hyperliquid. According to the team, the platform even accounted for more than 50% of total tokenized gold perpetuals open interest during the recent gold rally.

Pricing the Unpriceable: 24/7 Markets

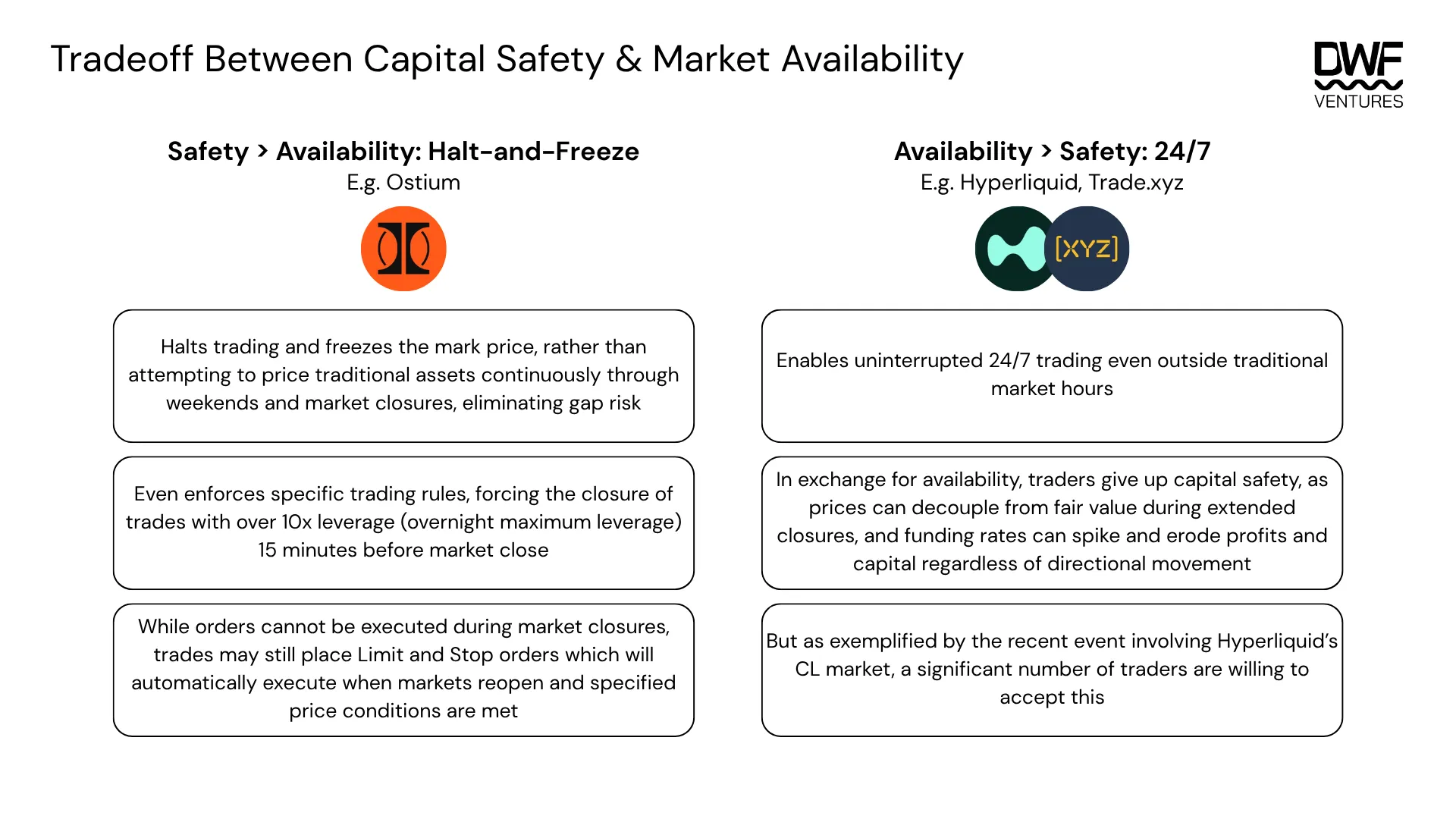

Although both platforms have emerged as leading venues for RWA perps trading, they adopt different approaches to 1) market access, and 2) real-world asset pricing. In the absence of a continuous, regulated reference price for traditional assets outside of market hours, platforms are forced to then make a fundamental tradeoff between capital safety and market availability.

According to the tradeoff that each platform chooses, there are key differences that have to be factored into RWA pricing, and hence oracle design.

Ostium

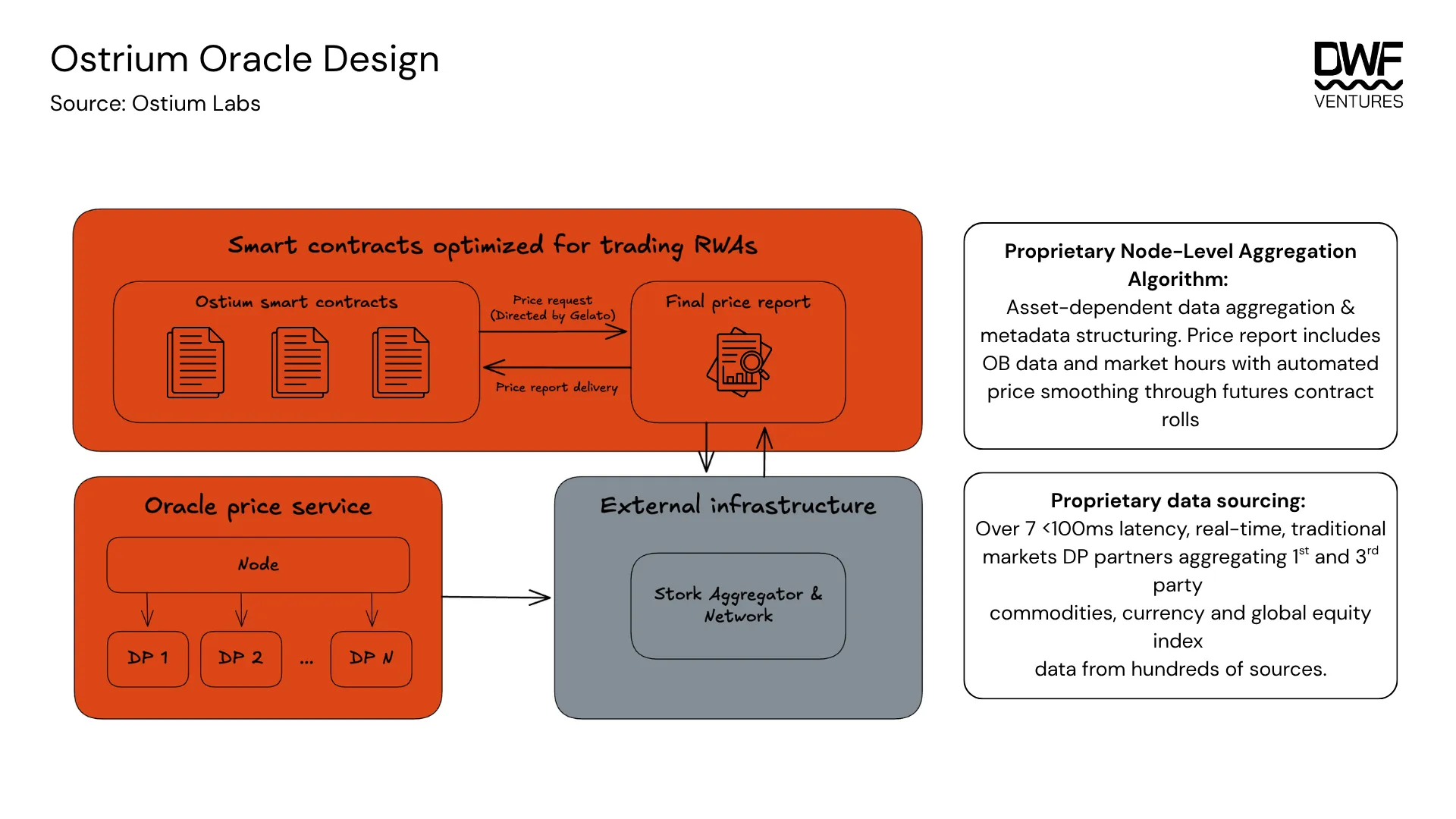

To support its halt-and-freeze model, Ostium partnered with Stork Network to build a bespoke oracle solution capable of handling the complexities that traditional asset pricing introduces, including out-of-market hours, futures contract rolls, and price gaps at open. Rather than relying on periodic snapshots or single-source references, Stork’s Composite Oracle Services allows for the creation of tailor-made feeds for each asset class, constructed using Ostium’s own pricing algorithm and a custom Stork aggregator capable of parsing both market hours and bid/ask data.

These feeds include metadata that enables portfolio-level risk management capabilities for traders. Delivery is then handled through a pull-based oracle that only pushes price updates onchain at the moment of trade execution, minimizing unnecessary onchain activity while maintaining accuracy. Liquidations and limit orders are then triggered by Gelato Functions, an automated keeper system built to handle the specific order types like stop losses, take profits, stop limit orders etc.

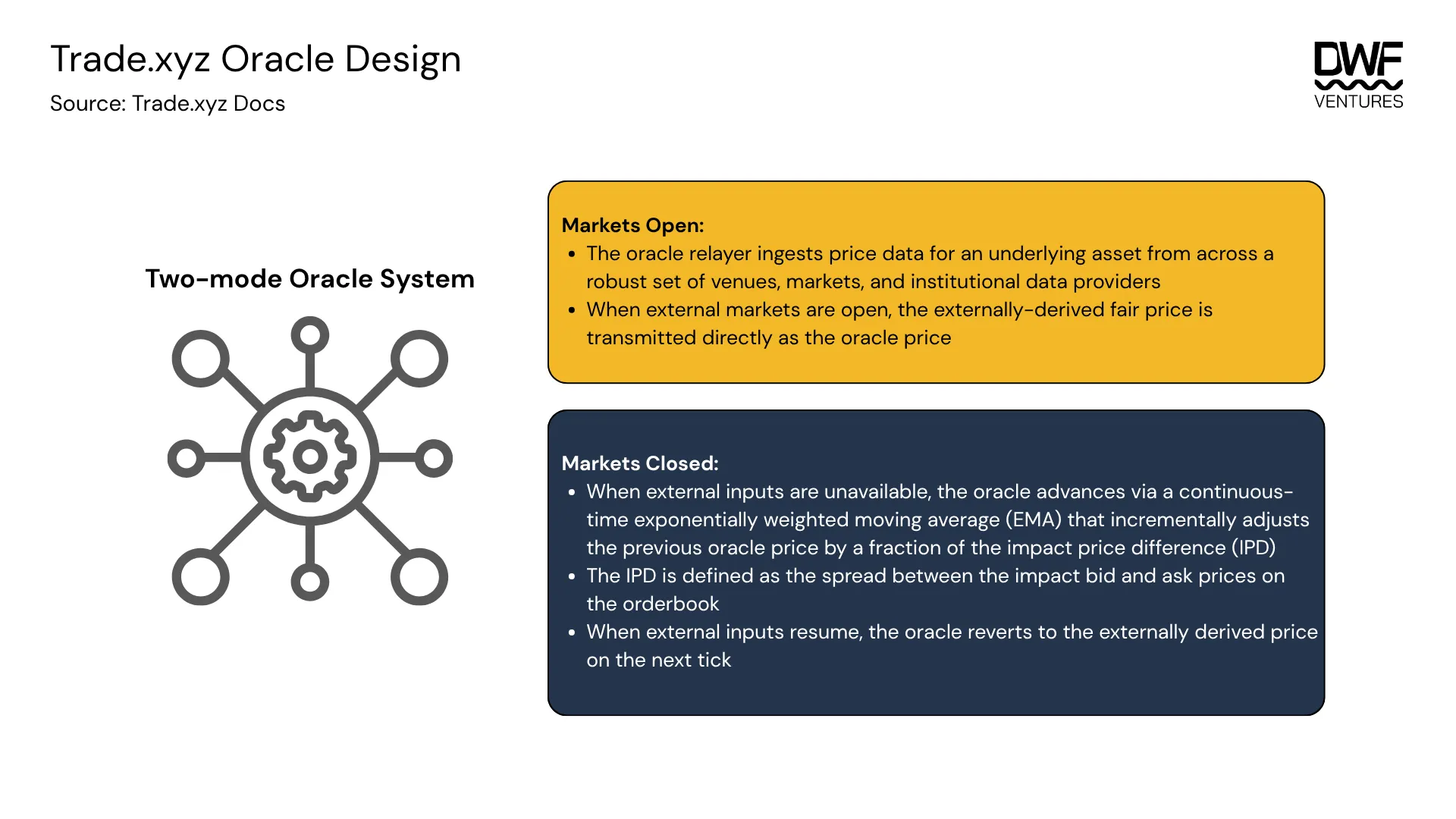

Trade.xyz

Trade.xyz adopts a two-mode oracle system - one for when markets are open, another for when they are closed. The oracle system serves two critical functions: as the reference price for funding, and as a direct input to mark price calculation.

While neither approach is inherently superior, they reflect different perspectives and bets on what traders actually need. Ostium optimizes for predictability and capital protection, while Trade.xyz and similar platforms optimize for continuous availability and price discovery. As RWA perp markets mature and liquidity deepens, the two models are likely to converge toward a middle ground.

What 24/7 Regulated Markets Mean for RWA Perps

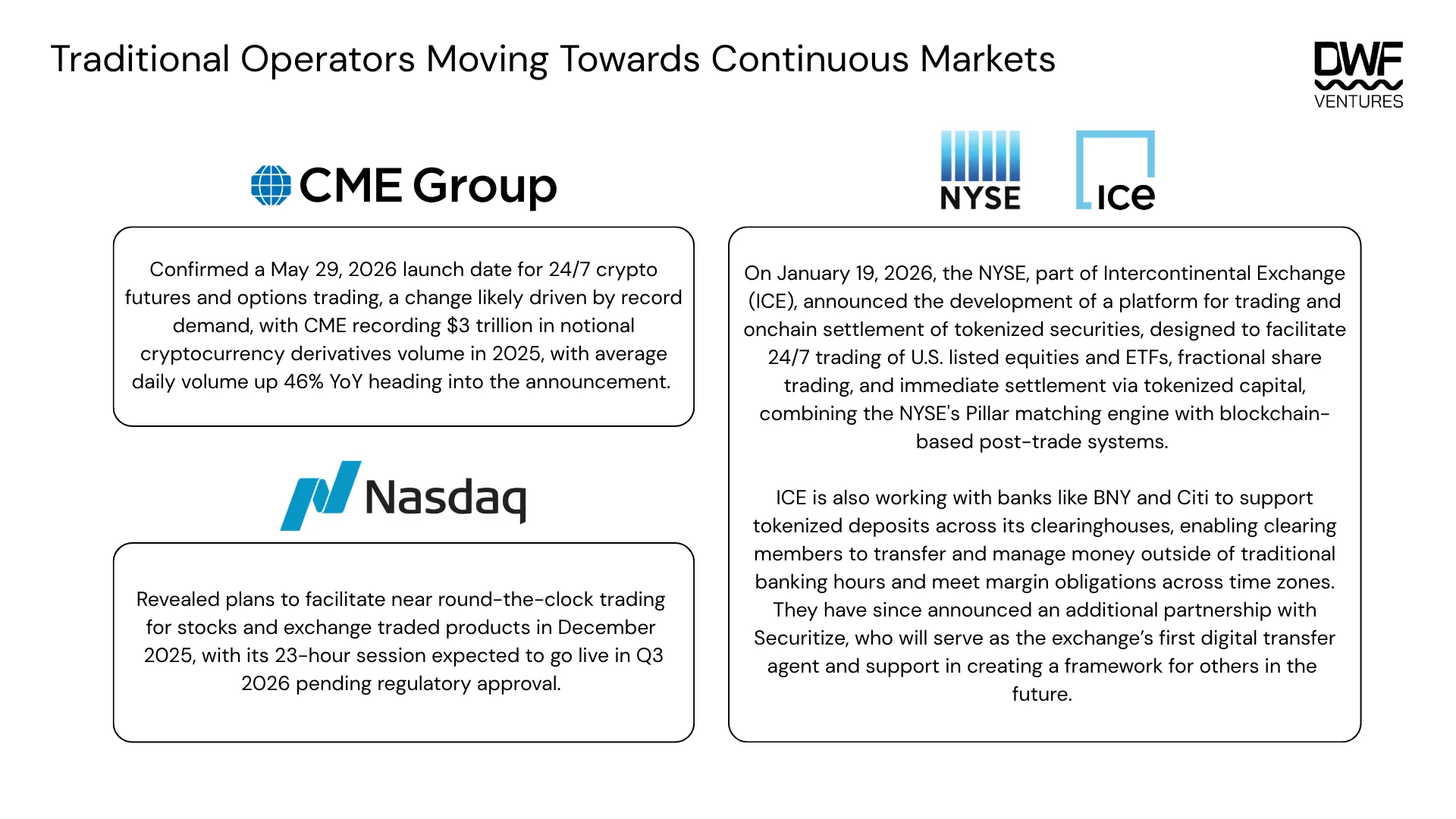

As mentioned above, the oracle problem at the core of RWA perp architecture lies with the absence of a continuous, regulated reference price for traditional assets outside of market hours. This however, may be on the verge of being solved, as traditional financial infrastructure that has long defined the boundaries of when and how assets can be traded has begun moving decisively toward continuous markets. Some examples include:

Taken together, these moves represent the most significant restructuring of market hours since 1985, and a direct response to the same demand signal that RWA perps platforms have been serving. Nonetheless, there are several impacts and considerations that would be taken into account.

- Oracle Quality: Whether relying on EMA-based estimates or other internal pricing mechanisms, existing 24/7 RWA perps platforms introduce basis risk and potentially create funding rate volatility that weekend traders absorb. A 24/7 regulated futures market for even a subset of traditional assets would provide a high-quality anchor price that oracles could reference directly, materially improving pricing accuracy and tightening the spread between onchain perp prices and fair value.

- Market Depth and Institutional Legitimacy: Continuous regulated price flow compresses arbitrage costs and narrows the basis between onchain and offchain markets, which then opens up the onboarding of market makers who were previously unwilling to provide bid-ask quotes without a reliable reference price. This makes RWA perps more viable and appealing for traders, with better execution at scale.

- Liquidity Fragmentation: 24/7 trading remains new to most market participants, and institutional infrastructure may face a lag in implementation. This could result in higher price impacts during off-hour sessions that could be more retail-dominated. However, for onchain RWA perp DEXs, this could present more of an opportunity than a threat. These platforms are already serving this market, and improved oracle quality from continuous pricing would reduce the basis risk and funding rate volatility that currently make off-hours trading costly.

The nature of the NYSE and ICE’s move make this a strategically pivotal moment for tokenized RWA perp DEXs. The platform is being built around tokenized securities that remain fungible with traditionally issued shares, preserving full ownership, dividend rights, and governance participation. This indicates an approach more similar to tokenization rather than a pure perpification one, especially in the aspect of potential regulatory approval before a full launch and wider adoption commences. While onchain RWA perp platforms operate on fundamentally different values and properties -being permissionless and synthetic, the window to differentiate and establish a strong moat on these is closing. As regulated 24/7 alternatives become fully operational, crypto native platforms will need to adapt and develop stronger features to cater to traders. These could include higher leverage, cross-collateralization, deeper liquidity, improved oracle infrastructure, and much more.

The Road Ahead: Perpification as Financial Infrastructure

The trajectory of RWA perps over the next three to five years will likely follow the same arc that perpetual futures themselves followed within crypto, from a niche product serving a specific group of users, to becoming a dominant primitive.

The building blocks are already in place. Oracle infrastructure is maturing rapidly, with custom feed providers like Stork purpose-building for the specific challenges of traditional asset pricing onchain. Execution quality on leading DEXs has reached parity with centralized alternatives for retail traders, and the demand has moved well beyond onchain speculation into genuine macro hedging and directional trading from a broader audience.

The more interesting question is not whether RWA perps will grow, but whether they will grow into a complement or a competitor to traditional derivatives markets. The answer is probably both, largely depending on the asset and the user.

For the unbrokered retail trader, RWA perpification is not a complement, but the only option. For the trader who already has access to traditional platforms, the 24/7 access that comes with onchain platforms offers genuine utility that regulated venues cannot replicate. Either way, both are likely to lead to increased interest and activity for onchain RWAs. The platforms that build the most reliable pricing infrastructure, the deepest liquidity, and the most intuitive user experiences will define what that market looks like at scale. What started as a workaround, simply a way for crypto traders to get exposure to gold and oil without leaving their wallet, is quietly becoming something more structural. Perpetual futures were crypto’s first great export to the world, RWA perpification may be its second.