How the New Generation of Money Markets Redefines the $50 Billion DeFi Lending

Updated On 31 July 2026

Published On 3 March 2026

Summary

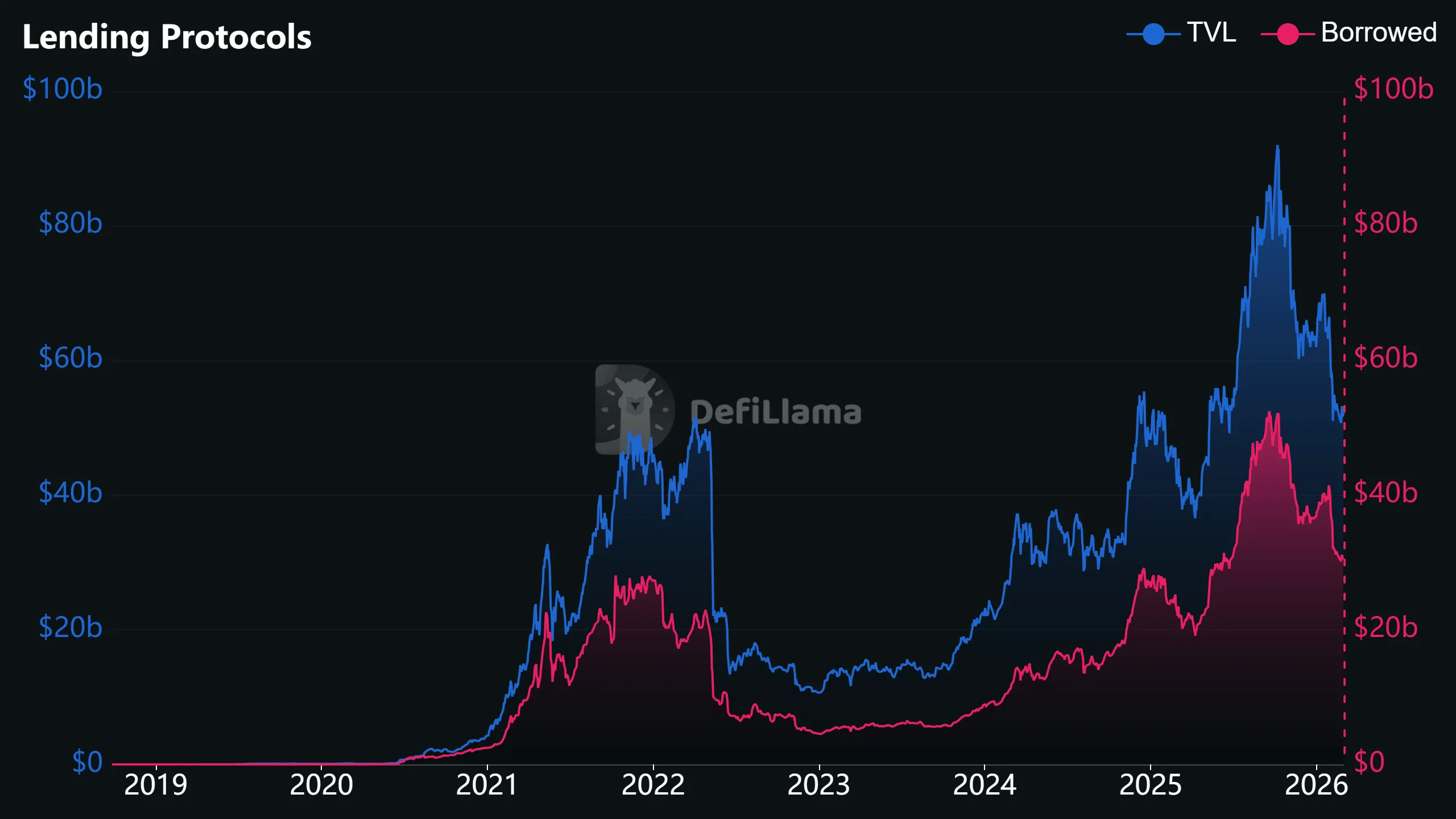

- DeFi lending protocols reached around $50 billion in TVL with $30 billion in active loans by March 2026, nearly doubling the 2021 bull-run peak despite broader crypto liquidity stress.

- DeFi money markets function as smart-contract “operating systems” for the decentralized lending market, handling rate discovery, collateral rules, and liquidations where rates rise with utilization (loans-to-deposits), boosting lender yield.

- The new generation of money market protocols is shifting from monolithic shared pools to modular, isolated markets with per-market parameters (oracles, collateral factors, and more) plus vault and allocator layers that route capital and enable automation and programmable credit strategies.

- DWF Labs’ DeFi Fund targets new money market projects in blockchain ecosystems like Ethereum, BNB Chain, Solana, and Base. The fund pairs venture capital with liquidity plus go-to-market, marketing and partner network support to help teams ship viable money-market dapps.

One of the strongest signals of 2026 in crypto is on-chain credit that keeps compounding: TVL scaled to $50 billion volume, with $30 billion in active loans, nearly doubling the peak of the 2021 bull run.

Despite the liquidity crunch across the wider crypto market, decentralized money market protocols are still attracting massive demand. If tokenized RWAs grow into a multi-trillion-dollar market by 2030, the need for on-chain credit will increase as well, enabling DeFi money markets to scale by an order of magnitude.

At the same time, the sector is undergoing a fundamental shift. To address existing issues, projects are moving away from monolithic lending pools toward modular architectures and isolated markets. In this piece, we’ll take a close look at how DeFi money markets work and break down the mechanics of a new wave of protocols to understand what capabilities they offer users, as well as explain where the builders can get financial backing and additional support for going to the market.

How DeFi Money Markets Actually Work

In DeFi, a money market is a lending protocol that facilitates the on-chain supply and borrowing of digital assets via smart contracts. In essence, these are permissionless systems that directly connect capital providers and borrowers.

Decentralized lending is the user-facing action: deposit, borrow, repay or get liquidated.

Money markets are the underlying machinery that makes those actions possible: rate discovery, collateral rules, liquidation mechanics, alongside capital routing and even risk packaging in latest iterations.

In other words, lending is the interface, and the money market is the operating system.

The core logic across most of these projects is similar. There are two sides: liquidity providers (lenders) and borrowers. Lenders deposit assets into a pool and receive a tokenized position that represents their claim on principal plus accrued interest. Borrowers post collateral and take out a loan within a limit dictated by risk parameters such as the collateralization ratio, liquidation threshold, and other settings.

Interest rates on DeFi money markets typically depend on liquidity demand: the higher the ratio of outstanding loans to deposits, the more expensive borrowing becomes, driving up the yield for lenders.

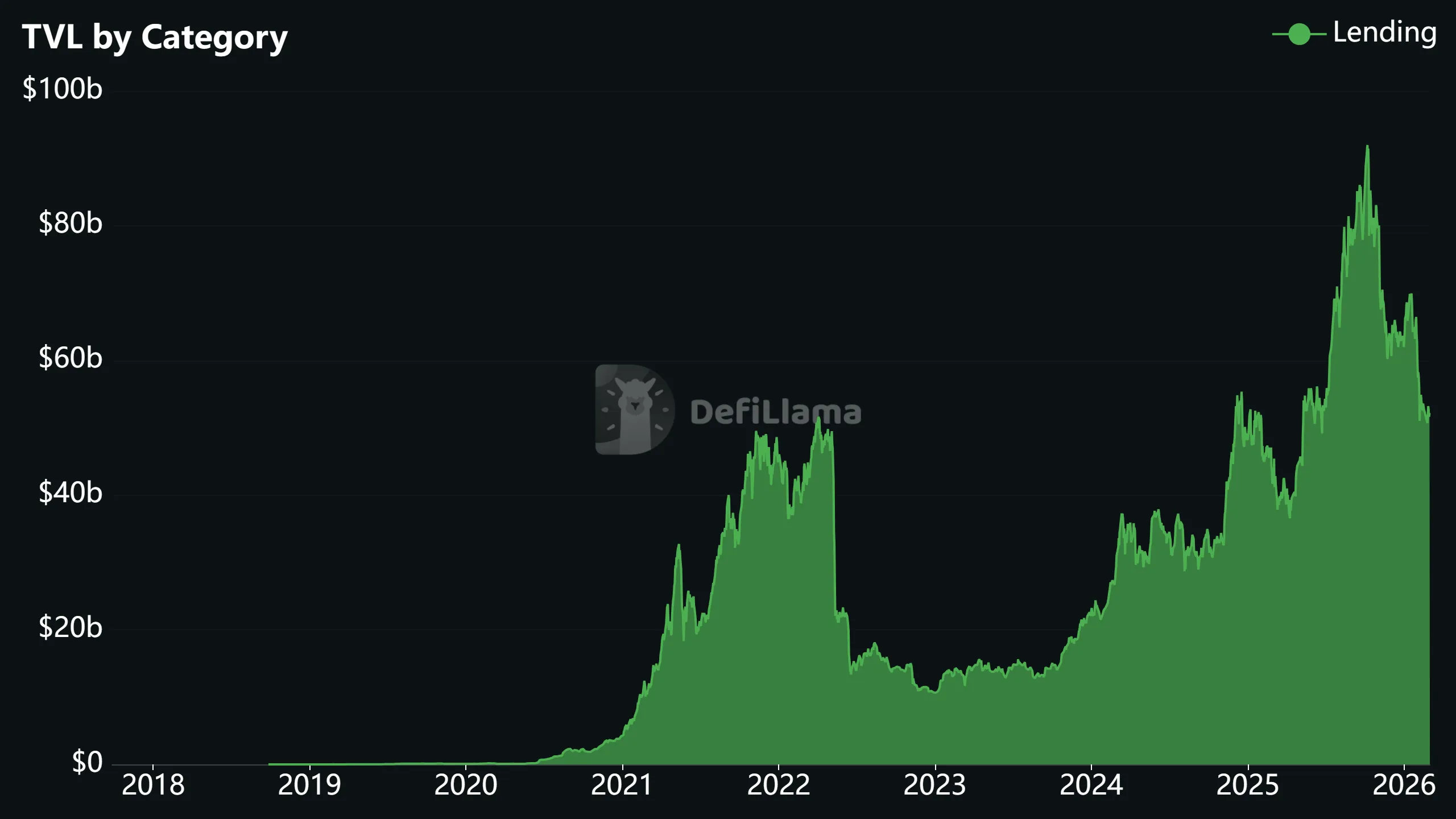

The decentralized money market model is one of the most successful financial primitives in the space. The data makes that clear: for several years running, lending protocols have led DeFi by Total Value Locked (TVL), with more than $50 billion in assets locked in smart contracts.

Why Users Lend and Borrow On-Chain

DeFi money markets aren’t valued only for attractive rates and deep liquidity. You can think of these protocols as open infrastructure — the foundation for digital financial “money legos.” Blockchain rails allow us to bypass the bottlenecks of the legacy credit system by offering some unique design qualities:

- Permissionless. Powered by smart contracts, decentralized money markets operate on a permissionless model: you don’t need approval from any central gatekeeper to supply capital or take out a loan.

- Non-custodial. Thanks to DeFi money markets, users deposit crypto and RWAs into smart contracts rather than transferring them to an intermediary, maintaining full control over their capital and actions.

- Composability. Dapps have a major advantage: assets can be tokenized. Positions in lending pools are often tokenized and remain liquid, for example, to be used in other DeFi protocols to get extra return.

- Transparency and programmability. Because every money market is defined in code, anyone can check how rates are calculated, which assets are supported, what collateral thresholds apply, and under what conditions liquidation is triggered.

This makes it possible to assess the rules of the game — and the system’s behavior in advance, including under stress. It also helps make returns more predictable.

From “Flat” Lending to Modular Credit Infrastructure

Although the definition about decentralized lending is accurate, it fails to capture the major transformation in DeFi architecture that led to the emergence of the new generation of protocols.

While the 1st generation of protocols like Aave and Compound were optimized for scale through shared liquidity pools, modern money markets such as Morpho and Silo Finance are optimized for precision.

Here are the major shifts in modern decentralized money markets:

- Market isolation. 1st-gen lending aggregates assets into broad liquidity pools with reserve-level parameters. Modern designs isolate risk at the asset pair’s (“market”) level, reducing contagion and making risk explicit rather than systemic.

- Fine-tuning for each market. Instead of global settings, newer architectures allow each pool or vault to define its own oracle, interest rate model, collateral factors, and liquidation thresholds. Risk becomes modular and customizable.

- Curated vaults. Earlier models required users to choose markets manually. Newer protocols introduce vaults and allocator layers that automatically route liquidity across markets, abstracting complexity while preserving isolation under the hood.

- Active capital routing. In 1st-gen systems, capital mostly sat in a pool earning utilization-based yield. In 2nd-gen systems, liquidity can be strategically allocated across isolated markets, effectively turning money markets into on-chain asset management rails.

- Wider automation. A major change in modern money markets is the automation layer built on top of them. As markets become modular and isolated, they also become easier to plug into bots, vault strategists, and autonomous agents that handle strategy execution, capital rotation, liquidations, and portfolio rebalancing in real time.

- Programmable credit. Modern architectures increasingly treat credit as composable infrastructure: instead of simply borrowing to withdraw funds, users can deploy leverage, interact across protocols, and construct structured strategies.

- Design-based scaling. The first generation scaled by being simple and unified. Modern money markets scale by separating risk domains, then rebuilding aggregation through routing, curation, and composability.

What does this mean for DeFi users? In short, more control and more choice. Instead of depositing into a single, generalized pool, you can select specific risk profiles, or go with a curated vault that optimizes allocation on your behalf. Borrowers gain access to more tailored collateral and leverage options.

Money markets become less of a one-size-fits-all lending app and more of a flexible financial toolkit.

After Aave: Why the Money Market Is No Longer a Monopoly

Historically, the DeFi money markets sector has been associated with monolithic liquidity pools. In this traditional model, depositors’ funds are commingled in a single pool, interest rates are calculated as a function of liquidity utilization within a given reserve, and risk parameters are set at the reserve level.

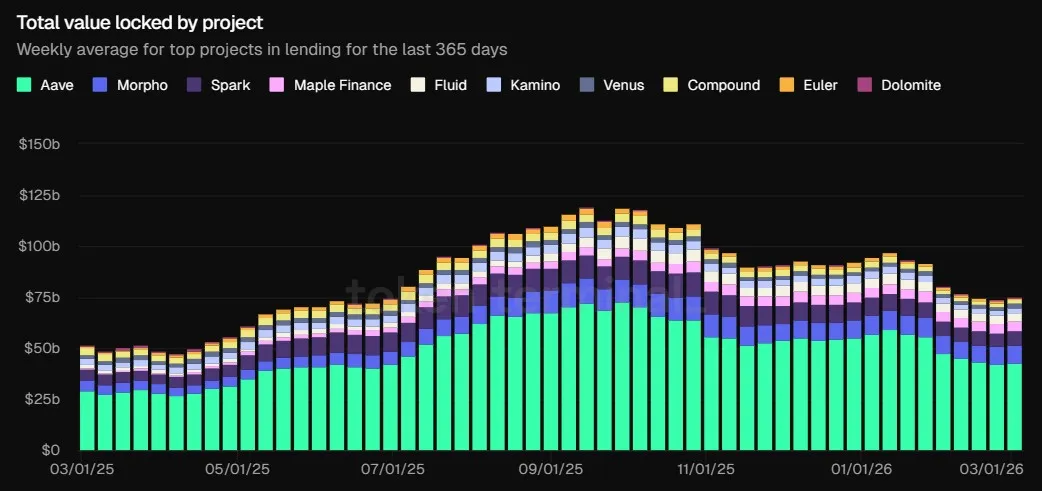

A classic example of this architecture is Aave — the largest lending protocol, with total deposits exceeding $41 billion as of this writing.

However, the sector, especially in the EVM ecosystem (Ethereum, plus other EVM chains like Base and Optimism) has become noticeably more diverse, and other protocols are capturing a bigger share. The industry constantly tries new approaches to lending protocol design, leading to the emergence of narrower solutions that tackle resilience, capital efficiency, and parameter control in different ways.

Morpho

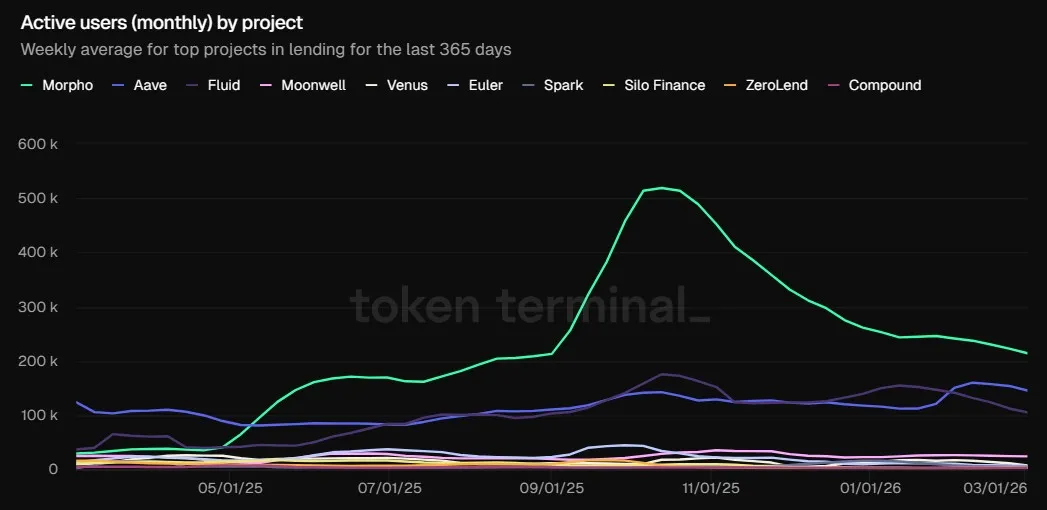

If Aave is the undisputed leader by TVL, Morpho is ahead in terms of active users. As of this writing, the project’s monthly active users (MAU) exceeds 226,000. Morpho supports multiple EVM blockchains, though most liquidity is concentrated on Ethereum and Base. Total deposits in the protocol are estimated at $8.7 billion.

Morpho moves away from the shared-pool model toward isolated markets. In the protocol’s architecture, each market is a “collateral asset / borrowed asset” pair. Configuration is set at the market level. Its oracle, interest rate model, and other parameters are chosen independently.

Importantly, markets are created by independent capital managers, and are designed to remain predictable, since they are isolated and immutable after deployment.

In addition to lending pools, Morpho also lists another product: Vaults, deposit “wrappers” that put user funds together in a single asset to allocate them across markets. In other words, you deposit into a specific vault and gain exposure to its allocation strategy without having to manually pick individual markets.

Silo Finance

Silo Finance designed its money market around a simple idea: each asset gets its own isolated “lane.” In practice, the protocol runs separate markets called silos where collateral and liquidation risks stay local. Silo Finance operates across four blockchains: Ethereum, Arbitrum, Sonic and Avalanche, and its total deposits are estimated at about $50 million at the beginning of March 2026.

All silos are technically identical, but borrowing parameters, interest rate models, and oracles are configured on a per-silo basis. This approach is especially useful for more volatile or niche tokens: an issue in one segment doesn’t have to automatically become a problem for every lender in the protocol.

As a modern DeFi money market, Silo demonstrates the importance of risk isolation and scaling via standardized “lanes”, alongside vault-style abstractions that help lenders avoid manual market selection.

Euler

You can think of Euler as a lending market “construction kit,” which lets you deploy custom lending vaults (essentially separate markets) with predefined rules — what assets are accepted as collateral, which data feeds are used, and so on.

These markets are isolated from one another, and even for the same asset there can be multiple vaults with different parameters. At the same time, users can use collateral supplied in one vault to borrow from another.

The protocol runs on a dozen blockchains, but the lion’s share of liquidity is on Ethereum. Total deposits exceed $1 billion.

Euler is a good example of how 2nd-gen money markets move beyond decentralized lending as a single product and become a platform for building many distinct credit products, each with different risks, collateral policies, and liquidation terms.

Venture Funding for Builders of New DeFi Money Markets

The growth of DeFi money markets is being fueled not only by user demand, but also by the availability of capital and hands-on support for teams building apps and infrastructure.

This is why DWF Labs launched a $75 million DeFi Fund. This program’s core investment thesis is that certain types of decentralized protocols, including money markets, will drive the new wave of growth in decentralized finance. The scope of the DeFi Fund are the projects in blockchain ecosystems like Ethereum, BNB Chain, Solana, and Base.

The DeFi Fund works on a hybrid support model. In addition to crypto venture capital, founders receive liquidity, go-to-market and marketing support, as well as access to a network of exchanges, infrastructure providers, and institutional partners, and more — because shipping a lending market is no longer the whole job, other critical areas are a business model, risk management, and liquidity routing.

Closing Thoughts

Even the most successful products eventually run into obvious inefficiencies — and those inefficiencies become the growth point for the next wave of solutions. In the first-generation money markets, the inefficiency was monolithic pools optimized for simplicity and scale, and the 2nd-gen markets optimized for explicit risk, modular design, and programmable credit.

More and more money market projects are entering the space, often making their unique mechanics to compete. Overall, this race will define how the credit and risk operating system will be like that the entire DeFi will build on, potentially integrating tokenized assets along the way.

This dynamic creates opportunities for everyone involved. Retail users get more tools for deploying capital and managing collateral, investors and builders get a chance to carve out their niche in a highly promising market.