Lending Markets: DeFi’s Fastest Horse?

Updated On 17 March 2026

Published On 3 July 2025

Since the launch of Sky, formerly known as MakerDAO, in 2017, lending markets have become a cornerstone of DeFi, allowing users to freely lend and borrow assets. What started as simple over-collateralized loans has evolved with innovations like algorithmic lending, peer-to-pool models, variable interest rates, and permissionless access to credit—pioneered by protocols such as Compound and Aave on Ethereum.

The DeFi Summers of 2021 and 2022 marked a major turning point. Interest in yield opportunities and liquidity mining incentives surged, driving billions of dollars into lending protocols. These platforms became widely known and helped push DeFi’s total value locked (TVL) to all-time highs. At a time of low traditional interest rates, they offered attractive returns and unlocked new financial strategies like yield farming and leveraged trading, reshaping the onchain finance landscape. What began on Ethereum has since expanded across nearly every blockchain ecosystem. In many cases, lending accounts for the largest share of TVL on a given chain.

With lending markets already in the midst of a resurgence in TVL and active loans, will its growth continue to sustain? Can it emerge as DeFi’s fastest horse? The DWF Ventures team explores the questions in this article.

A Climb to All-Time Highs

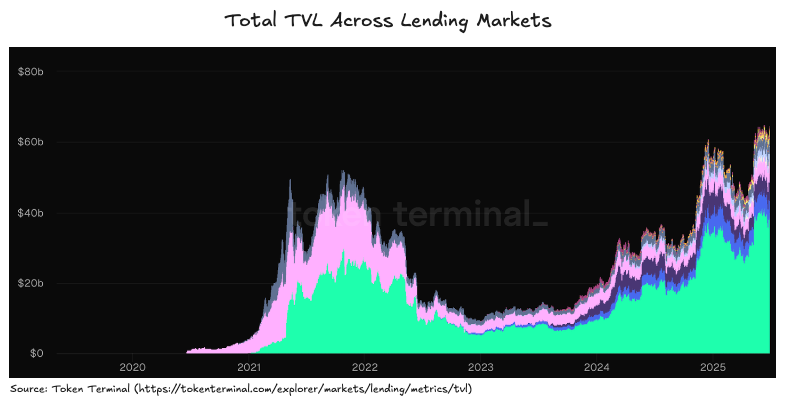

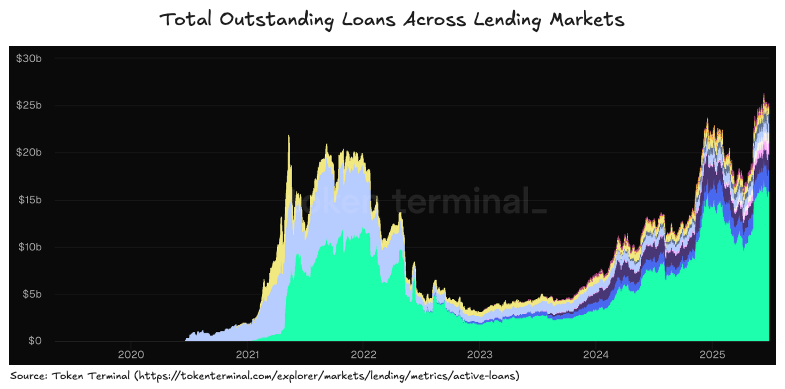

Towards the end of 2024, Total Value Locked (TVL) and outstanding loans across lending markets quietly surpassed previous highs set over the DeFi Summers in 2021 and 2022. Since then, they have continued on to establish levels at close to $65 billion in total TVL and over $25 billion in total outstanding loans, marking current values as the highest that the industry has seen to date.

By late 2024, TVL and outstanding loans in lending markets quietly surpassed the previous highs set during the DeFi Summers of 2021 and 2022. Since then, both metrics have continued to climb—reaching nearly $65 billion in total TVL and over $25 billion in active loans, marking the highest levels recorded in the industry as of July 2025.

The similarity in utilization ratios between recent levels and the All-Time Highs (ATHs) of the DeFi Summer points to a consistent demand for capital. This may indicate the renewed interest in onchain yield opportunities and increased use of borrowed assets.

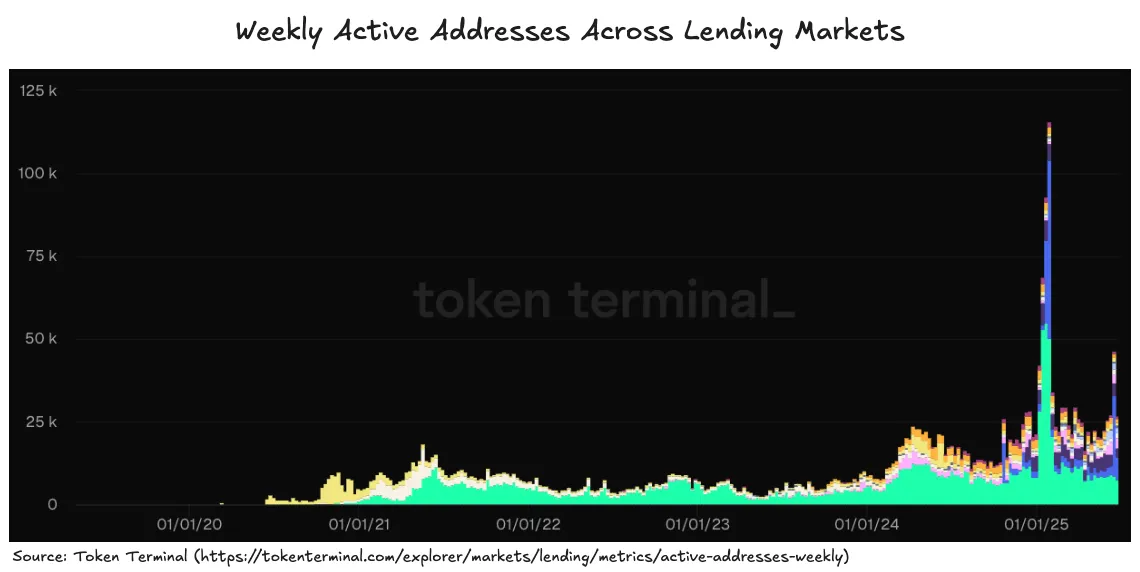

Additionally, the steady rise in weekly active addresses—despite recent market volatility driven by the U.S. presidential elections, trade tensions, and geopolitical uncertainty—offers a positive signal for the durability and continued momentum of lending market growth.

Tailwinds

Having surpassed previous ATHs, lending markets now stand at a pivotal inflection point. Supportive policy shifts from regulators like the U.S. Securities and Exchange Commission (SEC), growing tokenization and capital inflows from real-world assets (RWAs), and the rapid expansion of stablecoins are all accelerating this momentum. These tailwinds not only reinforce lending’s role as the backbone of DeFi, but also position it as one of the fastest-growing sectors in the ecosystem.

SEC Regulatory Shift

The U.S. Securities and Exchange Commission’s (SEC) evolving stance toward crypto points to a more favorable regulatory environment for the DeFi sector. At the SEC’s Crypto Task Force Roundtable in May 2025, newly appointed Chairman Paul Atkins announced plans for an “innovation exemption.” This would ease regulatory barriers for DeFi platforms.

The proposed exemption would allow both registered and unregistered entities to launch onchain products and services more quickly. It aims to support blockchain innovation while the SEC works on permanent, tailored rules for DeFi.

These shifts could reduce uncertainty, clarify compliance requirements, and give DeFi protocols more legitimacy. They may also encourage risk-averse institutions to begin exploring the space. Lending markets, seen as a lower-risk and essential layer of DeFi, are already gaining institutional interest.

Flow of Institutional Capital and RWAs Onchain

As of July 2025, more than a dozen major banks and financial institutions, including BlackRock and JPMorgan, have publicly announced plans to bring real-world assets (RWAs) on-chain. Several are already exploring decentralized finance (DeFi) protocols for lending and borrowing.

One example is a partnership between several institutions, the tokenization platform Centrifuge, and the lending protocol Morpho. Since 2022, this collaboration has enabled lending and borrowing against more than $10 million in tokenized private credit and real estate. Other protocols have also seen institutional activity. Compound, for example, has been used by Fidelity for stablecoin lending.

This recent influx of institutional capital and tokenized real-world assets, supported by the Federal Deposit Insurance Corporation’s (FDIC) 2025 guidance easing crypto engagement, reflects growing trust in DeFi. In particular, it highlights the strength and future potential of proven lending markets.

Growth of Stablecoins

As of July 2025, the market capitalization of yield-bearing stablecoins stands at over $8 billion. Over the past year, this sector has experienced major growth. It has been driven by rising demand for a productive digital dollar and sustainable yield opportunities.

New teams continue to enter the space, using strategies that generate yield from sources such as Treasury Bills, funding rate arbitrage, and others. The U.S. Senate’s passing of the GENIUS Act has added momentum. This legislation introduces a federal framework for stablecoin regulation, setting the stage for broader adoption by both retail and institutional investors.

Lending markets have been among the biggest beneficiaries of the growth of yield-bearing stablecoins. These lending markets play a key role in providing liquidity, enabling leveraged looping strategies, and improving capital efficiency for stablecoin holders. Some users have even deposited yield-bearing stablecoins into Pendle to mint Principal Tokens (PTs), which are now widely accepted as collateral in major lending protocols.

According to RedStone, PT markets have already contributed over $2 billion in TVL across platforms like Aave, Morpho, Euler, and Silo. As yield-bearing stablecoins continue to expand in both market size and usage, the importance of lending markets is expected to increase as well.

At the same time, the overall stablecoin market has grown significantly. During the DeFi Summers of 2021 and 2022, TVL in DeFi was much higher than the market capitalization of stablecoins. As of July 2025, the opposite is true. If market conditions improve in the near future, this shift could open up new opportunities for capital to flow back into DeFi.

Protocols to Monitor

Several individual protocols have announced major upgrades. These range from new methods to improve deposit utilization and yield, to efforts that unify fragmented lending markets and expand support for tokenized assets as collateral.

Euler

Among lending markets, Euler has been one of the fastest growing both in terms of TVL and active loans, boasting almost 940% and 1180% in growth respectively since the beginning of the year. More impressively, they boast one of the highest utilization ratios at the moment, at close to 53%, far above the sector’s overall ratio.

Euler has been one of the fastest-growing lending protocols in 2025, both in total value locked (TVL) and active loans. Since the beginning of the year, its TVL has increased by nearly 940%, rising from $198 million to $2.13 billion. Active loans have grown by 1,180%, from $88 million to $1.13 billion. Euler also stands out with one of the highest utilization ratios in the sector, currently at nearly 53%. This is significantly above the industry average.

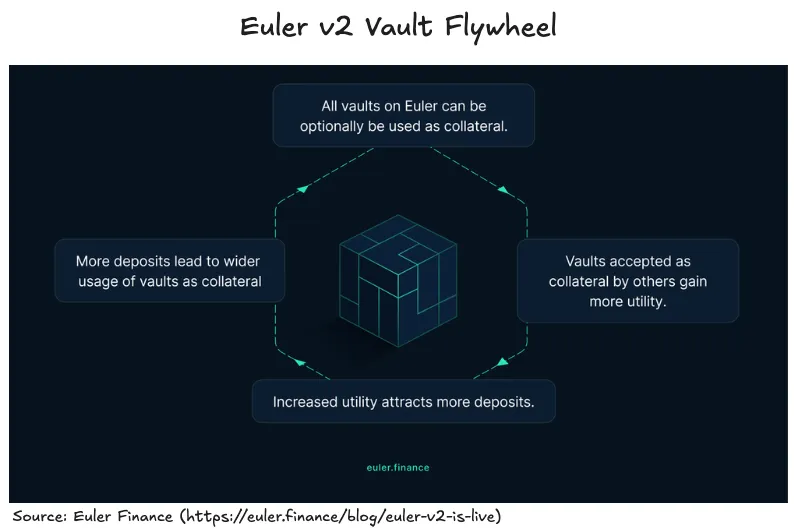

The growth can be attributed to Euler’s Version 2 (v2) upgrade, which introduced a modular architecture through the Euler Vault Kit (EVK) and the Ethereum Vault Connector (EVC). It also included support for collateral rehypothecation, a process where existing collateral is reused to back additional positions.

These upgrades enabled the permissionless creation of custom vaults designed for better capital efficiency and higher yields. At the same time, Euler created a positive feedback loop. By allowing users to use existing vaults as collateral for new ones, the protocol attracted more deposits and increased TVL.

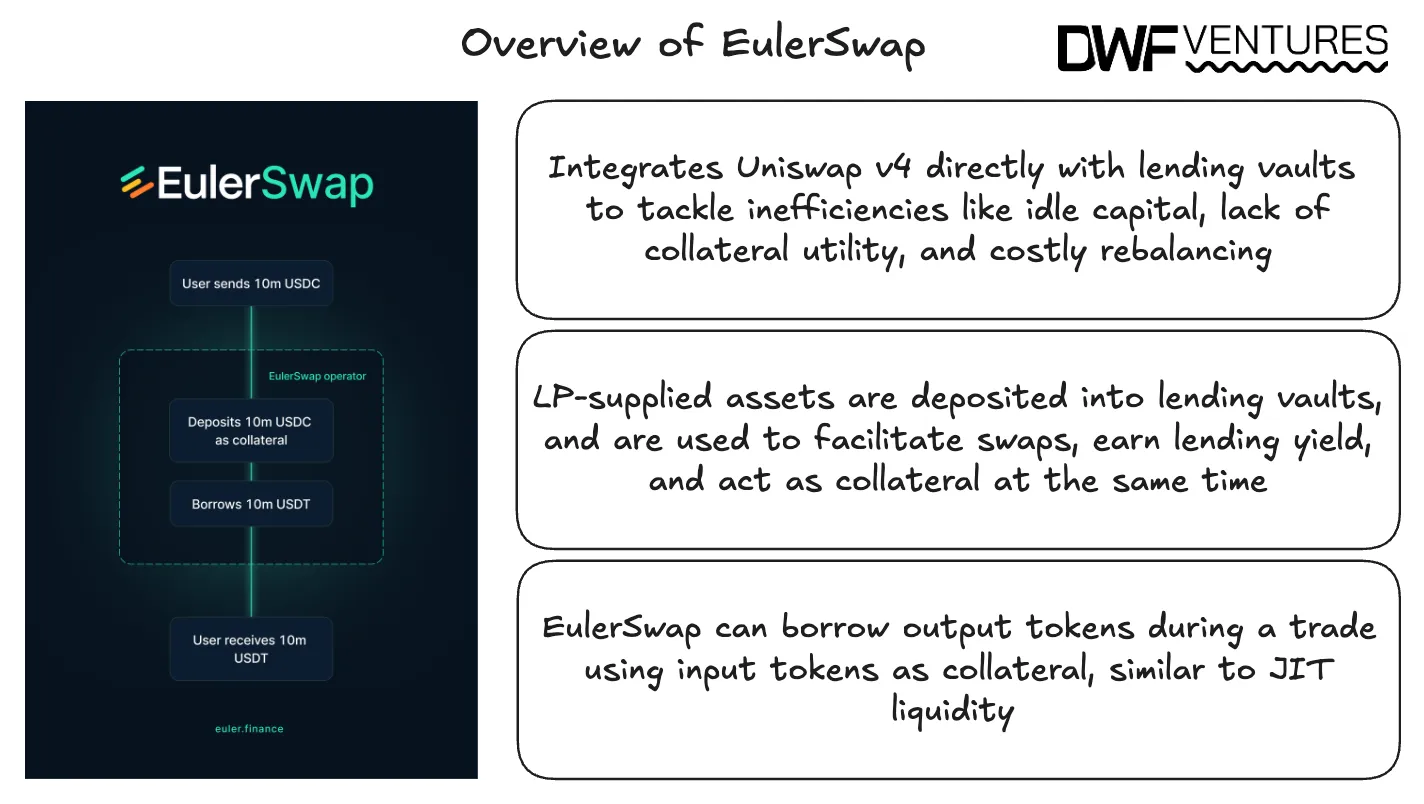

The team recently shared details about the upcoming EulerSwap, a feature expected to accelerate growth by integrating swapping functionality directly with lending. This will turn Euler’s vaults into a unified liquidity layer. The combination of lending and trading offers several benefits. These include hedgeable liquidity provider (LP) positions, leveraged LP positions, and higher yields. Together, these improvements are likely to increase the utilization of deposits.

Morpho

Currently standing at second in terms of TVL and active loans, at almost $4.2 billion and $2.34 billion respectively, Morpho has managed to surpass early entrants like Compound and Venus. This growth was largely driven by their architecture, which introduced an immutable, permissionless base layer and externalized risk curation through a new concept called curators.

With this, it has also managed to become the first protocol directly integrated by a major exchange like Coinbase, having issued over $300M in bitcoin-backed loans to date. Multiple other leading distributors, including Trust Wallet, Binance Wallet, Safe, and Ledger, also utilize Morpho to power their yield products.

In the third quarter of 2025, Morpho ranks second in TVL and active loans, with nearly $4.2 billion and $2.34 billion respectively. It has surpassed early lending protocols such as Compound and Venus. This growth has been driven largely by Morpho’s architecture, which introduced an immutable, permissionless base layer and a new approach to risk management through external curators. Curators are third-party entities that assess and manage lending risks. Morpho has also become the first lending protocol to be directly integrated by a major exchange like Coinbase, having issued over $300 million in bitcoin-backed loans as of July 2025. Other leading platforms, including Trust Wallet, Binance Wallet, Safe, and Ledger, also use Morpho to power their yield products.

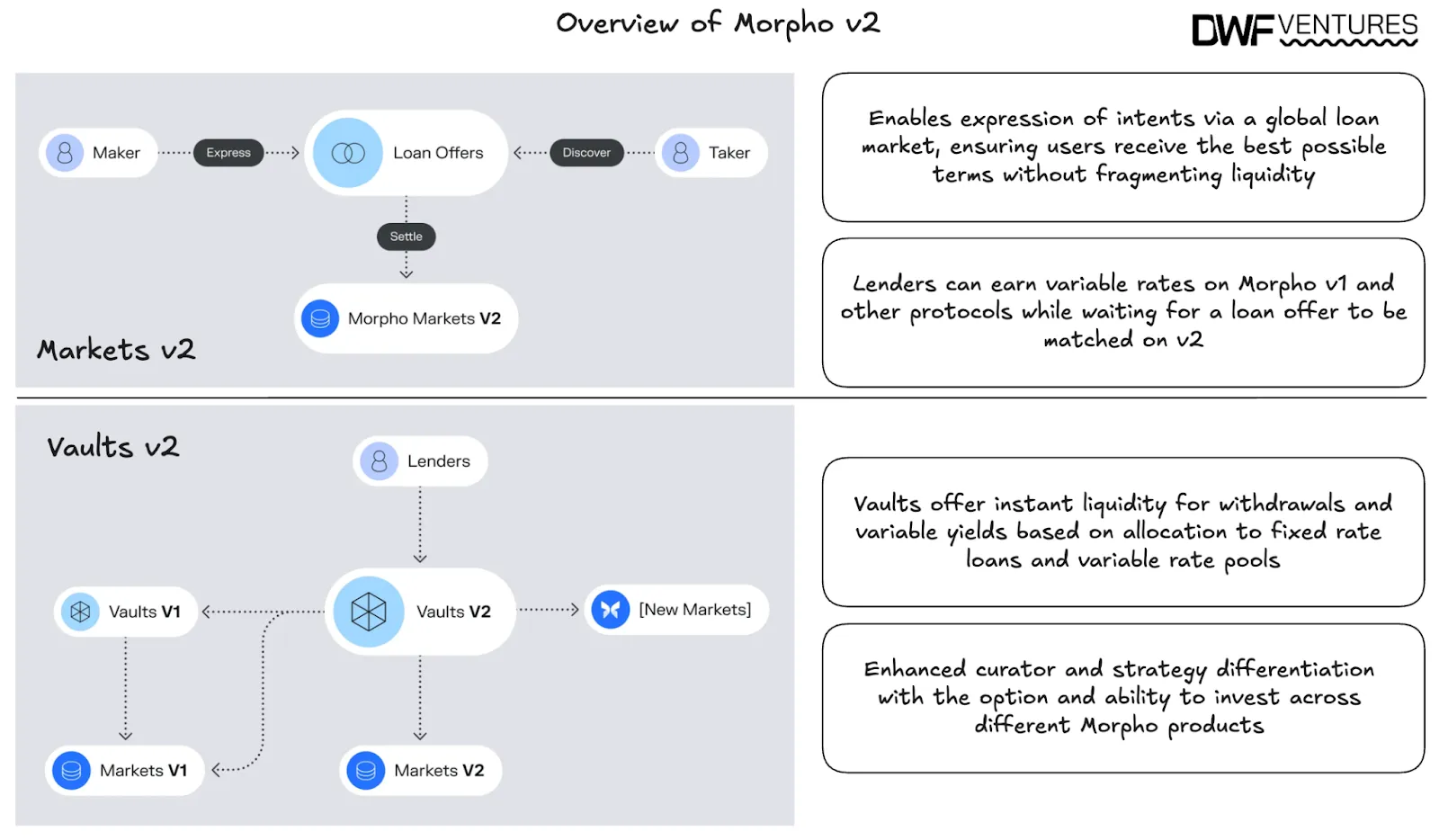

To advance its vision of building a complete onchain system for loan pricing, the Morpho team recently introduced Morpho v2. This upgrade includes Markets v2 and Vaults v2 and transforms Morpho into an intent-based lending marketplace. The new version supports fixed-rate, fixed-term loans with customizable parameters. Morpho v2 complements Version 1 (v1) and positions the protocol to better serve institutional participants seeking stable and predictable rates and yields. It also helps unify fragmented loan markets and supports broader innovation within DeFi.

Aave

As one of the more established names in the lending space, Aave has solidified its position as the market leader. Compared to the DeFi Summers of 2021 and 2022, Aave has actually increased its market share and dominance, despite a significant rise in competition. Its share of total deposits and borrows has grown from about 40% to around 60% in 2025. However, Aave’s current Version 3 (v3) architecture still has limitations. One of the main issues is liquidity fragmentation across different markets.

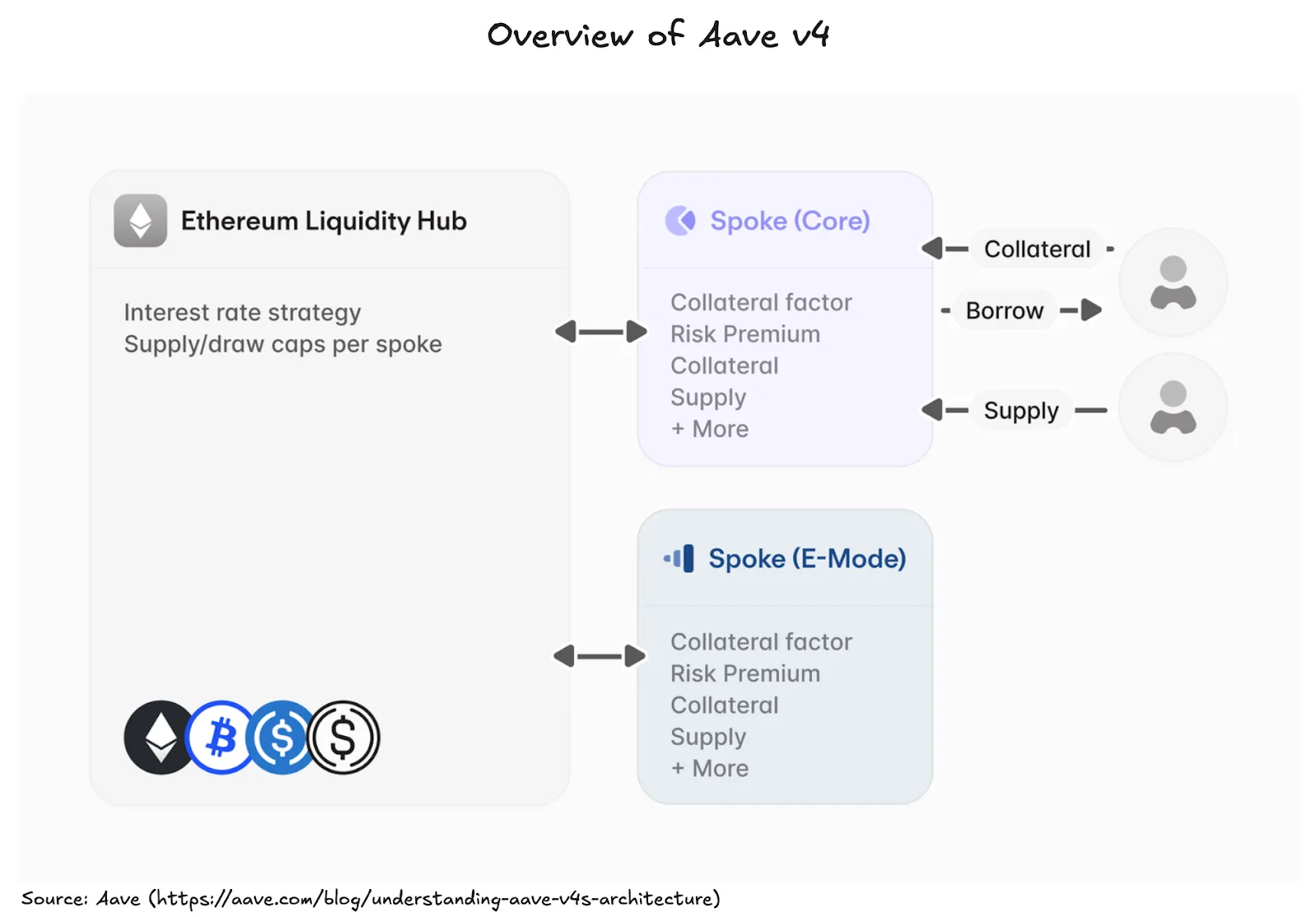

To improve its architecture, Aave’s upcoming Version 4 (v4) introduces a Hub and Spoke model that increases modularity, enhances liquidity, and offers greater flexibility for developers. Spokes are specialized lending pools that developers can create without permission. E-Mode Spokes are optimized for high-efficiency lending of correlated assets, such as stablecoins. Core Spokes are designed for general assets, including liquid staking tokens (LSTs) and real-world assets (RWAs), and offer customizable risk parameters. All Spokes connect to a chain-specific Liquidity Hub, which serves as the central source of deposited liquidity and enforces core accounting rules. This structure allows Aave to support a wider range of risk profiles and encourage innovation without fragmenting liquidity. It also provides a way to seed liquidity for new and unique Spokes.

Aave’s initiative, Horizon, launched in March 2025, complements v4. Horizon focuses on integrating RWAs into DeFi lending markets. It enables institutional-grade products, such as tokenized private credit, treasuries, and real estate, to be used as collateral in lending pools. When combined with v4, Horizon supports the creation of custom Spokes that offer risk-managed yields on RWAs, along with the potential for leveraged strategies. Horizon’s regulatory-friendly approach may also help Aave attract more institutional users by taking advantage of v4’s technical scalability.

Conclusion

Overall, current data and market tailwinds suggest a future where lending markets continue to see strong, sustained growth. Upcoming protocol upgrades indicate that this sector could become the biggest beneficiary within DeFi, standing to gain the most from greater regulatory clarity, institutional interest in tokenized assets, and the expansion of stablecoins.

At the same time, the development of innovative, yield-optimized and leveraged strategies for both retail and institutional users strengthens lending’s role as the leading force in DeFi. The sector is well-positioned to drive a new lending market-led DeFi Summer.

DWF Ventures continues to explore opportunities across DeFi. Builders seeking strategic investment or ecosystem support connect with our venture capital team.

Important Disclaimer: This research is intended for general informational purposes only and does not constitute financial advice. Readers are strongly advised to conduct independent due diligence and consult with a qualified financial professional before making any investment decisions.