Liquidity Meltdown: Failures, Contagion, and New Rules of Yield Generation

Published On 5 December 2025

-960x576.webp?prefix=media)

The events of October-November 2025 marked one of the most turbulent periods the crypto ecosystem has seen in years. A cascading series of failures originated in an emerging yield-generation sector, triggered by a major exploit at Balancer and amplified by structural weaknesses. What began as a single attack rapidly grew into a broad liquidity crunch, exposing hidden leverage, opaque risk models, and deeply intertwined obligations that many users never realized existed.

DWF Labs examines how the Balancer hack triggered a chain reaction leading to a collapse of several protocols and contagion of the lending infrastructure, and the reasons for why some synthetic-stablecoin issuers failed while others endured.

What Began the Trouble: The Balancer Hack and the Panic Ripple

The sequence of events began on November 3, 2025, when Balancer, a major multichain DeFi protocol, suffered a critical exploit in its V2 pools that resulted in about $128 million in losses.

One of the largest DeFi trading protocols saw its TVL draining from about $775 million to less than $300 million in just a week after the hack.

Some analysts described this as the “butterfly-effect catalyst”: the event was not isolated to Balancer but instead triggered a sudden, ecosystem-wide loss of confidence, becoming a market-wide stress event, and prompting the reassessment of the hidden risks embedded in many DeFi protocols.

Why Stream Finance’s xUSD Became Under-Reserved and Lost Its Peg

Stream Finance’s core vulnerability stemmed from the design of xUSD, a yield-bearing token. In its yield-generation model, the protocol reportedly engaged in recursive looping, i.e. user deposits were recursively deployed into leveraged strategies, amplifying both yields and systemic risk.

This structure meant that the backing of $xUSD was sensitive to losses in the underlying strategies.

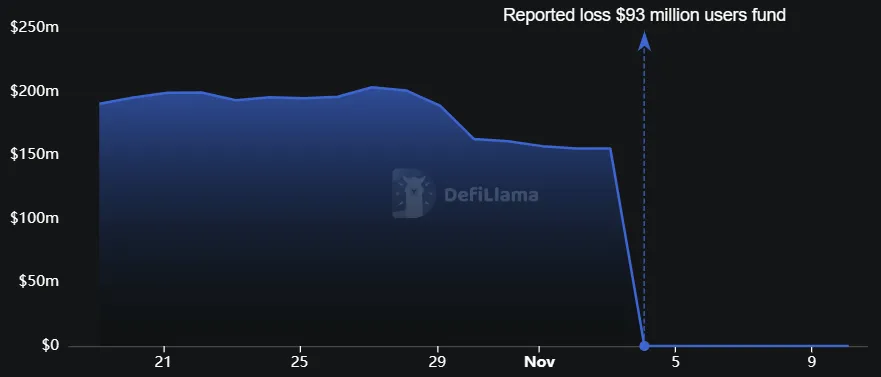

The situation deteriorated rapidly when Stream Finance disclosed an approximately $93 million loss linked to an external fund manager following Balancer’s hack. In response, the protocol paused deposits and withdrawals while investigating the issue.

That suspension proved decisive: with redemptions halted, xUSD lost the primary mechanism that kept it anchored to the dollar. Markets quickly priced in the uncertainty, and the stablecoin slipped far below its intended $1 peg.

Stream Finance’s Failure Triggered a Chain Reaction in DeFi Lending

Because xUSD circulated widely through DeFi lending markets, its declining price exposed multiple protocols to potential under-collateralization. Some lending markets were using “base value” oracle pricing (i.e. the “stable” price hard-coded in smart contracts) rather than real market prices, which temporarily delayed liquidations but masked the extent of the growing imbalance. As redemptions remained frozen and confidence evaporated, traders began off-loading xUSD on secondary markets, pushing the price down.

According to researchers, around $285 million of direct debt exposure across various DeFi lending protocols were identified as being tied to Stream Finance’s xUSD, xBTC and xETH ecosystem.

Users in vaults and lending pools that contained xUSD, such as those on Euler, Morpho, and Silo, found themselves unable to withdraw primarily because liquidity for the other side of the pair (USDC, USDT, etc.) vanished instantly during the panic.

When xUSD began to depeg, everyone tried to withdraw the paired liquid asset, primarily stablecoins like USDC or USDT, at once. But pools and lending markets are built on automated ratios: if too many users redeem one side, the pool becomes imbalanced. Within minutes, these pools flipped into a state where almost all remaining liquidity was xUSD, without a single second token left. Users who wanted to exit with xUSD could not meaningfully do so because the market price had collapsed.

DeFi Liquidity Incentives Only Made Things Worse

During the crisis sparked by Stream Finance, the interest-rate models of lending protocols responded exactly as designed, but in a way that amplified the breakdown. As borrowers fled or defaulted and utilization soared toward 100%, the protocols’ dynamic rate curves kicked in:

- Supply (lending) APY skyrocketed to triple- or quadruple-digit levels.

- Borrow APY exploded even faster, often into thousands of percent.

These explosive rate spikes were meant to encourage repayment and restore balance. Instead, they triggered two harmful outcomes.

Firstly, attracting new depositors that were chasing massive APYs, but unknowingly deposited into a system already dominated by toxic collateral (xUSD). This added fresh capital to a doomed pool.

Secondly, borrowers who held xUSD collateral had no reason (or ability) to repay loans, since their collateral had collapsed in value. Many simply walked away, leaving the system with unrecoverable bad debt.

This combination trapped liquidity: new suppliers added more USDC/USDT to pools expecting high yields, but those assets were immediately borrowed out and could not be returned. With no borrower repayments and no incentive structure capable of forcing them, the funds were effectively frozen.

Stream Finance’s Collapse Created a Contagion Effect in the Yield-Generation Sector

The collapse of Stream Finance spread beyond lending into the yield-generation and synthetic stablecoin sectors, highlighting how protocols that appear distinct can nonetheless share deep, underlying exposures:

- Stream Finance used assets from other platforms (such as Elixir’s deUSD) to back xUSD, creating mutual exposure between protocols.

- When a large borrower (Stream) defaults or becomes illiquid, the creditor (Elixir) and any downstream markets can become stressed almost simultaneously.

- Liquidity stress in one protocol therefore propagates through lending markets, AMM pools, vaults, and synthetic asset issuers, creating a contagion effect.

- Where risk management was weak: lack of transparency, high leverage, inter-protocol borrowing loops, this chain reaction was faster and more severe.

Let’s break down the underlying connection between the crash of Stream Finance and its impact on two other yield-generation projects, Stables Labs and Elixir.

Elixir (deUSD)

Elixir launched deUSD in mid-2024 as a decentralized, overcollateralized synthetic dollar stablecoin, aiming to compete with established offerings. At its height, deUSD had a total supply in the order of about $150 million and had gained traction across various DeFi platforms and AMM pools.

The protocol built much of its backing by attracting deposits and using it for collateral to issue deUSD, with a significant portion of that collateral flowing to, and being managed by, Stream Finance. According to on-chain watchers, around 65% of deUSD’s collateral or backing was exposed via Stream.

When Stream disclosed a major loss after Balancer’s hack, and halted withdrawals on November 4, 2025, the collateral underpinning deUSD collapsed in value.

Elixir stated that Stream still holds about 90% of the remaining deUSD supply, amounting to approximately $75 million of tokens.

The project says it has processed redemptions for ~80% of deUSD holders (excluding Stream’s holdings), and has taken a snapshot of the remaining holders for a claims or redemption portal, promising 1:1 USDC compensation when resources are recovered.

In the meantime, deUSD’s market price collapsed by over 99%, dropping from the peg of $1 to less than a cent (~$0.002) by November 11, 2025:

Stables Labs (USDX)

USDX, issued by Stables Labs, positioned itself as a multi-chain synthetic stablecoin aiming to maintain a 1:1 peg to the US dollar backed by collateral, hedging strategies and delta-neutral positions. At its recent peak, USDX had a circulating supply of about $685 million.

However, the stable asset experienced a swift depeg shortly after Stream Finance’s crash.

Lending pools on protocols like Lista DAO and Euler Finance which accepted USDX or its staked variant sUSDX as collateral had been drained of USDC and USDT liquidity, while interest rates soared (in some vaults surpassing 800% APY) and major borrowers apparently did not repay.

The result was a rapid loss of liquidity in USDX-backed markets, and a growing sense that the protocol had either mismanaged its collateral hedging, or that critical dependencies had broken. A research report from a DeFi management company Re7 Labs indicated that over $13 million of funds were affected in markets tied to Stables Labs in connection with the xUSD and Stream Finance fallout.

By November 14, 2025, USDX was trading at around $0.04, losing over 95% of its value:

In response to the crisis, Stables Labs announced a “USDX Restoration Arrangement,” a phased recovery process for USDX holders which involves an on-chain snapshot of affected balances and a claim process, but did not guarantee full repayment or immediate redemption.

Governance Failure Adds to the Liquidity Crunch: The Maple vs. Core Dispute

While Stream Finance and Stables Labs suffered from technical contagion and collateral devaluation, a different type of failure struck the market simultaneously, further deepening the liquidity crisis of October-November 2025. This time, the trigger was not a protocol exploit, but a breakdown in governance and partnership agreements between Maple Finance and The Core Foundation.

The conflict centered on a strategic alliance formed in early 2025 to develop a liquid staking product on the Core blockchain. By late October, however, the partnership had collapsed into a high-stakes legal battle. The Core alleged that Maple Finance had breached exclusivity and non-compete clauses by secretly utilizing joint resources to develop a direct competitor product, syrupBTC.

On October 30, 2025, right as the crypto market was grappling with the Balancer aftermath, the Grand Court of the Cayman Islands granted an injunction against Maple Finance. This ruling legally barred the launch of syrupBTC and froze specific assets tied to the dispute.

The operational impact was immediate and severe for lenders. Maple Finance was forced to abandon the product launch and initiate a wind-down of the associated pools. However, just as with the yield-bearing stablecoins, liquidity was not fully accessible: as Maple announced, while approximately 85% of user capital could be returned, the remaining funds were effectively trapped, pending the resolution of the legal proceedings.

The legal conflict added a new dimension to the month’s liquidity meltdown: both Maple Finance and Core lost about 20% and 30% of their TVL volumes, respectively, following the first announcement about legal proceedings by the Core Foundation.

Lack of Transparency, Not Yield-Generation Model, Is the Real Problem

It seems that, for now, the domino effect caused by Balancer’s hack has ended. Whether Stream Finance’s, Stables Labs’, Elixir’s, and now Maple Finance’s users will be able to get their capital back is still uncertain.

Some now question if yield-generation is inherently flawed. However, the sequence of the described collapse events cannot be summed up by this notion. Rather, it can be explained by the mistakes in how these protocols were managed: greed for high yields, coupled with lack of accountability and insufficient transparency:

- Transparency gap. Yield-generation protocols promised high yields but did not provide sufficiently detailed or real-time disclosures of how their strategies worked, what collateral was used, or what legal risks existed behind the scenes, or how much counterparty and third-party risk existed.

- Misaligned incentives and “yield race”. The drive to attract deposits by offering unusually high APRs encouraged protocols to take on more risk (leverage, rehypothecation, exotic strategies). In many cases, the yield was marketed aggressively while the risks, whether financial or operational, were less prominently disclosed.

- Opacity of off-chain risks. Many strategies involved off-chain fund managers or multiple layers of lending and recursive loops, or undisclosed development conflicts, making it hard for users to understand the real exposure.

- Inter-protocol exposure and contagion. Because many protocols used the same kinds of strategies, collateral, or even cross-protocol integration, when one faltered (Stream), the failure propagated to others (Elixir, Stables Labs) via shared pools, loans and obligations.

In other words, the model of giving users yield is acceptable, but only when it’s underpinned by strong disclosures, real-time monitoring of risk, conservative leverage, and clear governance.

Which Yield-Generation Protocols Benefitted

The crash of Stream Finance and Stables Labs certainly disrupted the confidence in yield-generation projects. For example, the sector’s leader, USDe from Ethena Labs, saw a substantial drop in its circulating supply: from nearly $15 billion in October to less than $7 billion by early December.

On the flip side, some protocols appear to have performed relatively well and grown their crypto assets’ supply despite the broader market stress.

Falcon Finance, a universal collateralization protocol, has stayed remarkably steady. It has gradually built trust by maintaining a fully auditable reserve structure, publishing granular breakdowns of its asset allocations, and adopting diversified, balanced strategies that avoid single-counterparty or single-strategy concentration. As a result, its USDf token continued to grow even during peak market stress: in the last 30 days, Falcon synthetic dollar’s supply soared from ~$1.5 billion to over $2.2 billion.

Diversified and balanced mix of yield-generation strategies (the current allocation is provided on the Transparency page) allows Falcon to offer competitive yields without exposing itself to the cascading leverage loops or hidden risk pathways that contributed to the failures of Stream Finance and Stables Labs. As DWF Labs’ and Falcon’s Managing Partner Andrei Grachev emphasized:

“We don’t offer looping strategies, opportunities and leverage, but we offer sustainable, competitive and scalable products with great yield”.

He also said that the current market downturn is the “moment to get great deals with great builders”, and in the end of November 2025, DWF Labs launched DeFi Fund aimed at providing venture capital and other means of support to the teams developing dark-pool perpetual DEXs, decentralized money markets, and fixed-income or yield-bearing asset products.

One more example is Sky Money. The protocol emphasizes non-custodial access: funds remain in smart-contracts rather than being held by a central custodian. It also means that user assets are fully visible on-chain. At the same time, Sky’s yield rates are moderate and the strategy design is oriented toward stability rather than highest possible APY at all costs.

This contributed to user confidence and, alongside Falcon Finance, made Sky Money more resilient than other yield-generation protocols: in the last month, Sky’s USDS supply added almost $1 billion, surpassing the $9.2 billion mark by mid-November 2025.

Yield-Generation Sector Has Changed Inevitably

The turbulence that swept through the crypto market between October and November 2025 marked a decisive turning point for the yield-generation sector. What began as an isolated case, quickly evolved into a broader crisis of confidence, revealing just how fragile opaque, highly leveraged yield models truly are. When the dust settled, market sentiment shifted sharply toward caution: users and institutions now show far less appetite for strategies where risks are hidden, misunderstood, or justified solely by aggressive APRs.

The lesson is clear. From this point forward, only yield-generation protocols that can demonstrate real transparency, balanced and diversified strategy construction, and disciplined risk management will be able to retain capital and grow sustainably. Users have seen how quickly yields can evaporate, and how opaque structures can lock or destroy value overnight. The market is no longer willing to gamble on high APRs without understanding exactly how that yield is produced and what risks stand behind it.

Protocols like Falcon Finance, Sky Money, and a select few others have shown that trust can be earned through on-chain verifiability, conservative design, and open disclosure of collateral flows and strategy allocations. Their relative resilience, and in some cases growth, amid sector-wide stress demonstrates the direction the market is taking.

Disclaimer: Falcon Finance is backed by DWF Labs. This article is intended for general informational purposes only and does not constitute financial advice. Readers should conduct their own research and consult with a professional advisor before making any investment decisions.