Dark-Pool Perpetual DEXs: Why They May Be the Next DeFi Alpha

Updated On 10 March 2026

Published On 7 January 2026

Summary

- Perpetual DEXs have scaled to over a quarter of the global crypto futures trading volume, with crypto perps trading volume peaking at $1.2 trillion in October 2025, and that growth is making full on-chain transparency increasingly costly for advanced traders.

- Real-time visibility enables front-running and sandwiching, liquidation hunting, and systematic trading against large positions.

- Dark-pool perp DEXs borrow the TradFi dark-pool idea by hiding or encrypting orders and positions while keeping pricing, matching, and solvency provable on-chain, and preserving self-custody.

- Common designs of dark-pool DEXs include sealed or encrypted orderflow using ZK proofs, batch or auction matching, “house-blind” execution, and even purpose-built L1 chains optimized for private perps.

- DWF Labs offers targeted venture funding and growth support via DeFi Fund for teams building dark-pool trading protocols.

Introduction

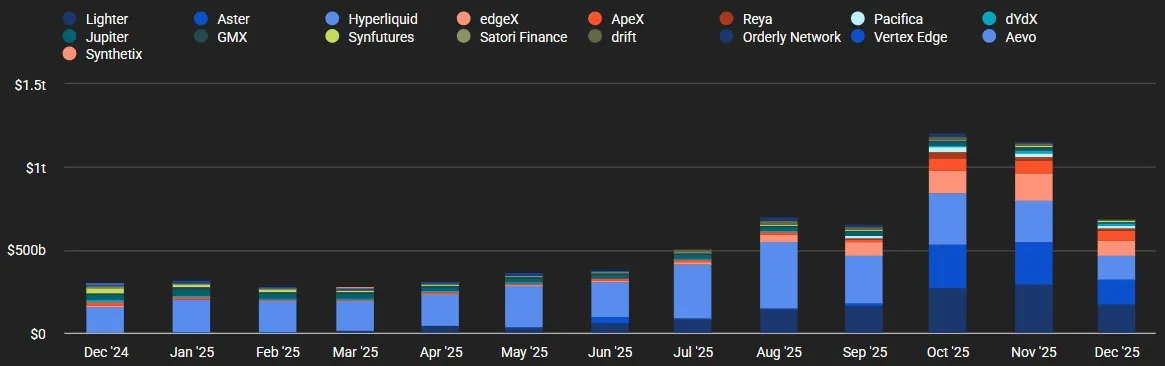

Perpetual futures decentralized exchanges (DEXs) became a pillar of the crypto derivatives market. Recent research estimates that perpetual DEXs now capture around 26% of global crypto futures volume, up from low single digits roughly a year earlier. Trading activity in crypto perps peaked in October, coinciding with the high market volatility, and totaling to $1.2 trillion of trading volume, according to data from The Block:

As the new trading instrument have scaled, however, a structural issue has become more apparent: complete, real-time transparency can make advanced traders and large positions vulnerable. Dark-pool perpetual DEXs are emerging as one answer to this problem. Read this article to learn why they can spearhead the next generation of DeFi projects.

Transparency Problems in Today’s Perp DEXs

Most leading perpetual DEXs are intentionally transparent. Positions, order sizes and liquidation levels are often visible on-chain in real time, either directly or via public dashboards.

This transparency has clear benefits for auditability and trust, but it also enables a set of behaviors that are economically harmful to traders:

- Front-running and sandwich attacks, especially when orders pass through public mempools.

- Liquidation hunting, where visible liquidation prices become targets during volatile periods.

- Systematic copying or trading against large positions, once those positions are widely known.

The widely reported case of Hyperliquid crypto trader James Wynn, who reportedly lost close to $100 million in a series of highly leveraged BTC liquidations in May 2025, crystallized these concerns. His positions, sizing and liquidation ranges were carefully tracked in public, turning his risk profile into a form of open data that others could trade around.

At the same time, existing research on MEV has demonstrated that a meaningful fraction of on-chain trading value is silently captured by transaction reordering and other forms of MEV. For leveraged crypto derivatives where margins are thin and turn-over is high, that hidden “tax” can substantially reduce strategy performance. In other words: the more important on-chain perps become, the more costly full transparency can be for serious participants.

Dark-Pool Model Applied to Crypto Perpetuals

In traditional finance (TradFi), dark pools are trading venues where orders are not displayed on the public order book before execution. Prices and volumes are still reported, but detailed intent such as size, exact level, and identity is shielded until after trades have been matched.

A dark-pool perpetual DEX adapts this concept to crypto derivatives. The general idea is:

- Orders and positions are hidden or encrypted in real time.

- Pricing, matching and solvency remain provable on-chain, often via cryptographic proofs.

- Traders retain self-custody, but their intent is not exposed to the broader market or to automated extraction strategies.

This concept was firmly put into the spotlight in June 2025, when Binance co-founder Changpeng Zhao proposed a dark-pool DEX for crypto perps. He explicitly argued that real-time visibility of orders and liquidation points on existing perpetual DEXs invites front-running and targeted liquidation, and suggested that a privacy-preserving design using zero-knowledge proofs could mitigate those risks.

Since then, a number of teams have begun experimenting with privacy-first perpetual architectures.

Design Foundations: How a Dark-Pool Perp DEX Works

Although there is no single blueprint, emerging projects share several common design patterns.

1. Encrypted or Sealed Order Flow

In a dark-pool DEX, orders are submitted either in encrypted form or as cryptographic commitments. Only a designated matching engine, or a small set of sequencers, sees enough information to match them, and even that view can be constrained. Zero-knowledge proofs are then used to demonstrate that matching followed pre-defined rules such as price-time priority and margin constraints without revealing raw order data.

2. Batched or Auction-Style Matching

Some dark-pool DEXs clear crypto trades in short batches rather than continuously, making it less attractive to attempt to “snipe” individual orders or to construct classic sandwich trading patterns around a single transaction. This can significantly reduce front-running incentives while still producing competitive pricing.

3. House-Blind Execution

Projects such as Opal DEX go further, marketing themselves as “house-blind” crypto perpetual DEXs where trades are sealed until settlement and are not visible to the public, to bots, or even to the exchange operators. The aim is to eliminate any advantage that might arise from the venue itself having privileged insight into orderflow.

4. Purpose-Built Layer-1 (L1) Infrastructure

There are also “purpose-built” perp DEXs like Defx that build a dedicated L1 blockchain optimized for high-speed, privacy-preserving perpetual trading. Its design combines a central limit order book, dark-pool execution and zero-knowledge encryption of order parameters such as size, direction, leverage and liquidation thresholds, while keeping transaction integrity verifiable on-chain.

Regardless of specifics, all these approaches attempt to balance confidentiality of crypto trader intent with public verifiability of prices and solvency, a more nuanced form of transparency than simply broadcasting all positions and orders in real time.

Why Dark-Pool Perp DEXs Can Be the Next Big Thing

The central question is not only whether dark-pool DEXs are technically appealing to the crypto trading community, but whether these protocols can be a genuine source of excess risk-adjusted return, the “alpha” that traders and liquidity providers seek. There are at least several reasons to suppose that.

1. Lower Implicit Trading Costs for Meaningful Size

For active crypto derivatives traders, the largest costs are often implicit rather than explicit: slippage, adverse selection and MEV rather than posted trading fees. If a dark-pool design can consistently reduce slippage on larger orders, the frequency of being traded against just before liquidation or stop levels, and MEV-related losses tied to exposed transaction flow, then the effective cost per trade declines. Over strategies that turn over capital frequently, a reduction of even a few basis points per round trip can make the difference between marginal and compelling performance.

2. More Stable Risk Profiles and Leverage Capacity

When liquidation bands and leverage are highly visible, they can become focal points during episodes of market stress. By keeping position size, direction and liquidation thresholds private, a dark-pool crypto venue can reduce artificially amplified volatility around known liquidation clusters, make it harder to manipulate price around funding or expiry events, and give risk managers greater confidence to offer deeper cross-margin and larger limits at a given risk tolerance. For sophisticated traders and liquidity providers, that can translate into higher usable leverage and more predictable drawdowns—in other words, a better risk/return profile.

3. Natural Fit for Institutional and Large-Scale Traders

Institutional desks and larger crypto treasuries are accustomed to using dark pools, block trading venues and request-for-quote (RFQ) systems to minimize information leakage. A perp DEX that can credibly demonstrate that counterparties cannot see its users’ orders ahead of execution, the venue operators themselves cannot exploit orderflow, and fair matching is enforced with on-chain proofs. CZ’s public advocacy for such an architecture is a reasonable indicator of where large-scale participants see the pain points today.

If privacy-preserving perp DEXs become the default route for institutional derivatives flow into DeFi, early users, liquidity providers and token holders in those ecosystems will be directly exposed to that growth.

4. Stronger Protocol Moats and Sustainable Fees

Competition among perpetual DEXs is already intense, with many venues relying heavily on short-term incentive programs. In the long run, the platforms that endure will likely be those that attract:

- high-quality, repeat orderflow;

- long-term relationships with sophisticated traders and institutions;

- crypto liquidity providers who trust that they are not systematically disadvantaged.

Private or semi-private execution can be a key differentiator. If a dark-pool DEX protocol can aggregate meaningful “sensitive” orderflow that must pass through its matching engine, it gains a durable base that can support liquidity provision incentives, token buybacks or other value-sharing mechanisms.

Trade-Offs and Open Questions

The move toward dark-pool perps is not without trade-offs.

First, there is reduced surface-level transparency. By design, some order and position information is hidden. That may make it harder for third parties to monitor market microstructure in real time, and raises questions about how much opacity is acceptable in a decentralized system.

Next, dark-pool DEXs are technically complex, which creates new attack surfaces. Encrypted orderflow, custom matching logic and zero-knowledge proofs add complexity. Implementations must be carefully audited, and edge-case failures could be serious if users implicitly equate “privacy” with “safety”.

There are also regulatory and governance considerations. As on-chain crypto derivatives attract more regulatory scrutiny, privacy-preserving leveraged platforms may be examined more closely than fully transparent ones, particularly if they become important for institutional trading.

Finally, there’s a question of fairness and access. Protocols will need credible, transparent rules to ensure that dark-pool style features do not simply re-create a two-tier market where only large players benefit from privacy.

These issues do not invalidate the concept, but they do mean that only a subset of designs will likely reach broad adoption.

Where to Get Funding for a Dark-Pool DEX

For teams building dark-pool perpetual DEXs, there is now dedicated venture capital on the table. DWF Labs has launched a $75 million DeFi Fund explicitly targeting projects in three areas: dark-pool perpetual DEXs, decentralized money markets, and fixed-income or yield-bearing asset protocols on Ethereum, BNB Chain, Solana and Base.

Alongside venture funding, portfolio teams can expect active liquidity provisioning, go-to-market support, and access to a broad exchange and infrastructure network, a generous package for dark-pool perp teams that need both capital and high-quality orderflow to reach scale. Founders interested in this direction can apply directly via the official DeFi Fund page.

Closing Thoughts

Perpetual DEXs already comprise a significant share of global crypto futures activity, driven by a desire for self-custody and programmable infrastructure. The next phase of innovation in DeFi is less about higher leverage or larger incentives and more about market structure, in particular, about reducing the ways transparency can be exploited against traders.

Dark-pool perpetual DEXs aim to keep the benefits of decentralization and verifiability while mitigating information leakage, MEV and liquidation hunting. If they succeed, they can lower trading costs, support more robust risk management, and provide a better entry point for institutional and large-scale participants.

We believe they are not just an interesting technical experiment but a credible candidate for the next major advancement in DeFi, rooted in improved microstructure rather than short-lived incentives.