Eyes on the Market, Volume 4: Year-End Hopium

Published On 31 December 2025

Summary

- Bitcoin drifted through late December 2025 in a tight price range, signaling less a demand shock than a year-end “risk ownership” reset where rallies fail without structural buyers.

- ETF flows stayed negative in the last 2 weeks: U.S. spot ETFs on both Bitcoin ($BTC) and Ethereum ($ETH) saw outflows, although the very end of the year presented a positive movement.

- The “store-of-value” narrative temporarily swung back to metals as 2025 performance diverged sharply, pushing crypto sentiment toward traditional safe havens into 2026.

- Beyond $BTC, tokenized stocks massively outperformed other RWA categories in 2025

- DeFi governance became the focal point: Aave’s dispute versus Uniswap’s “UNIfication” fee switch and planned $UNI burns as a concrete value-capture turn.

Introduction

As 2025 winds down and markets slip into holiday-mode liquidity, crypto is doing what it often does in late December: moving sideways on the surface while bigger positioning questions remain underneath. Does the year-end print set the stage for January’s fresh flows — and a very different 2026?

Bitcoin: Institutional Bid Looks Softer?

The last weeks of 2025 in crypto didn’t feel like a crash — more like a slow leak, while the market’s bleak sentiment contrasted with festivities and bright decorations. Following the low-volatility sideline trend, Bitcoin spent much of December pinned inside a tight range of $85,000-$90,000, and struggled to reclaim momentum into the holidays.

The BTC performance in the last weeks of 2025 is less about demand, and more about who holds the risk into year-end. Ted Pillows shared a chart on Bitcoin supply on Coinbase, which shows that long-term holders recently stopped selling BTC for the first time since July. Another important indicator was CME losing the top spot to Binance in $BTC futures open interest: it is a notable reversal because CME is often treated as the institutional “barometer” for directional exposure and basis trades.

When institutions are leaning in, price dips tend to get absorbed. When they’re stepping back, the market can still trade but rallies start failing for a simple reason: fewer structural buyers defend price levels. In that context, BTC hovering around the tight range looks more like a market waiting for a fresh regime in January flows.

As DWF Labs’ Andrei Grachev put in one of his recent interviews, many financial institutions avoid major trades in December because they close the fiscal year, so January 2026 will likely bring more breakouts to the crypto market.

ETF Flows Stayed Red

In the last two weeks, U.S. spot Bitcoin ETFs showed a net outflow. U.S. spot Bitcoin ETFs showed a net outflow of roughly $1.28 billion across the sessions reported in the period of December 15-26, with only one positive day in that period.

Spot Ethereum ETFs weren’t much better: around $0.75 billion net outflows across the same date range, with only December 22 showing a meaningful inflow day in the dataset. Movements in both categories were led by BlackRock’s IBIT and Grayscale’s ETHE.

With all that in place, the second positive day became December 30, which leaves a sign for a potential reversal trend.

Crypto ETF flows are a good litmus test for what might be waiting for the market around the corner: when inflows are persistent, dips feel “bought”. When flows are negative, rallies often feel like short-covering or thin-liquidity bounces.

Store-of-Value Debate Moved Back to Metals

While crypto drifted, precious metals put on a show.

Reuters reported silver briefly pushing through $80 per ounce, and gold near $4,500/oz, in the late-December melt-up, driven by a mix of Fed cut expectations for 2026, a weaker dollar, and persistent geopolitical and fiscal uncertainty — before some year-end profit-taking kicked in.

Current numbers for 2025 are stark:

- Gold is up about 72%

- Silver grew by about 181%

All while Bitcoin’s price is down 6%.

Discussions in the Crypto Twitter have now, at least temporarily, returned to embracing traditional precious metals as the “safe haven”, not Bitcoin. There is a high chance investors will choose real gold over the digital one in 2026.

However, Grachev believes in the revival of Bitcoin push:

“It doesn't seem really correct given adoption and institutional inflows in BTC. Of course, markets can be priced differently than we want, but something should happen and my bet would be on the BTC growth. Let’s see”.

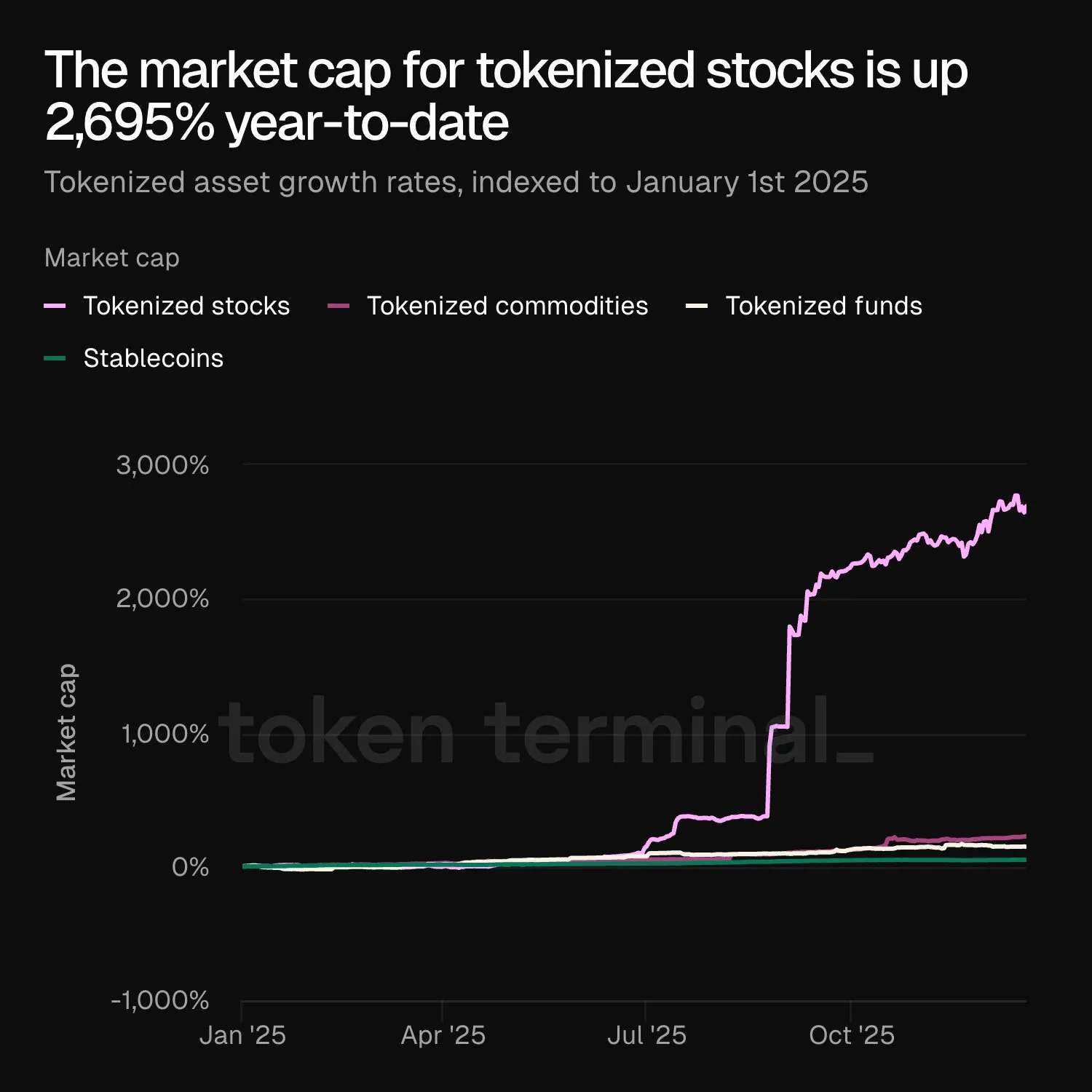

Notable Chart: Tokenized Stocks’ Takeover of RWAs

Token Terminal’s year-end snapshot of RWA growth makes the divergence hard to ignore: tokenized stocks’s market capitalization was up almost 2,700% year-to-date on December 22 (indexed to Jan 1, 2025), massively outperforming other asset categories (tokenized commodities were up 225%, tokenized funds 148%, and stablecoins ~50%).

The chart tells a story about timing. Tokenized stocks didn’t actually perform that well all year. Instead, it is an indicator of TradFi increasingly pushing the entire stock market on-chain. This comes without a big surprise, as tokenized stocks have clear benefits and regulation that’s improving globally.

Governance Conflict in Aave

DeFi’s most telling story in the last two weeks wasn’t a hack or a new chain, it was tension in the governance of a leading protocol.

On December 4, Aave Labs swapped out the front-end trade integration on Aave’s official interface, replacing ParaSwap with a CoW Swap-powered setup.

This move got under scrutiny by the community: critics argued that changes created a situation where value capture and control felt increasingly “off-DAO”, reigniting the long-running tension between Aave Labs and the Aave DAO.

In essence, old routing reportedly generated referral and surplus fees that benefited the Aave DAO, while the new arrangement prompted accusations that fees were now flowing to a non-DAO address, with delegates estimating the DAO was losing roughly $200,000 every week, or about $10 million annually.

Thus, the technical issue became a governance one: one camp framed the switch as “stealth privatization” — a sign that important economic levers, and distribution, could drift away from tokenholder control. The dispute then escalated into a bigger question: should key Aave brand assets (domains, trademarks, social handles) be brought under DAO governance?

It was decided by voting. In the end, the proposal to bring brand assets under DAO control was rejected: 55.3% voted against, 41.2% abstained, and only around 3.5% supported the move.

Aave avoided the escalation, but the alignment question hasn’t disappeared. If DAOs want to behave like financial organizations, they eventually have to answer institutional questions: who controls distribution, who captures revenue, and what exactly token holders own when the interface is operated by a separate entity?

Uniswap Reform: Fee Switch and $UNI Token Burn

Uniswap delivered the opposite kind of governance headline: a deliberate attempt to turn usage into token economics.

The proposal, dubbed “UNIfication”, set out to flip on Uniswap’s long-dormant protocol fees, route those fees into an on-chain pipeline that burns $UNI, and pair it with a one-time burn of 100 million $UNI tokens from the treasury. Alongside value-capture, it also aimed to “clean up” the ecosystem: shift key operational functions under one roof, remove interface-level fees, and formalize ongoing funding via a growth budget.

What changed after it passed? Apart from burning the part of $UNI supply, Uniswap implemented contract changes required to enable V2 and V3 protocol fees. In particular, the fee switch means that V2’s classic 0.30% swap fee becomes 0.25% flowing to LPs, plus 0.05% to the protocol, with V3’s protocol-fee parameters adjustable by governance.

$UNI traded the decision like a real tokenomics catalyst: bid into the vote, popped during the approval window, and then cooled. By December 29, $UNI was back around $6 from ~$5, suggesting the market liked the direction, but still treated it as a structural upgrade, not hype. This brings hope of getting $UNI back to its past highs of over $15 per token at the end of 2024.

The Close Will Confirm 2026

The last two weeks of the year didn’t deliver a clean crypto rebound but something useful instead: crypto stopped trying to be exciting and started to stabilize.

Bitcoin is ending 2025 less like a top, but not without the market hoping for its return. ETFs are still leaking. Metals are stealing attention. DeFi is arguing about who gets paid (and, in Uniswap’s case, starting to answer it).

Now comes the candle that matters. If the year-end close signals that the sellers are out of forced inventory, and buyers can step in without fighting mechanical flow, then 2026 doesn’t need a new story. It just needs the old one back: liquidity returning to rise.

Until that print shows up, any year-end confidence is just hopium dressed up as conviction.