USDT Scaling Solutions Explained: Can They Help Tether Achieve Further Global Adoption?

Updated On 5 August 2025

Published On 11 July 2025

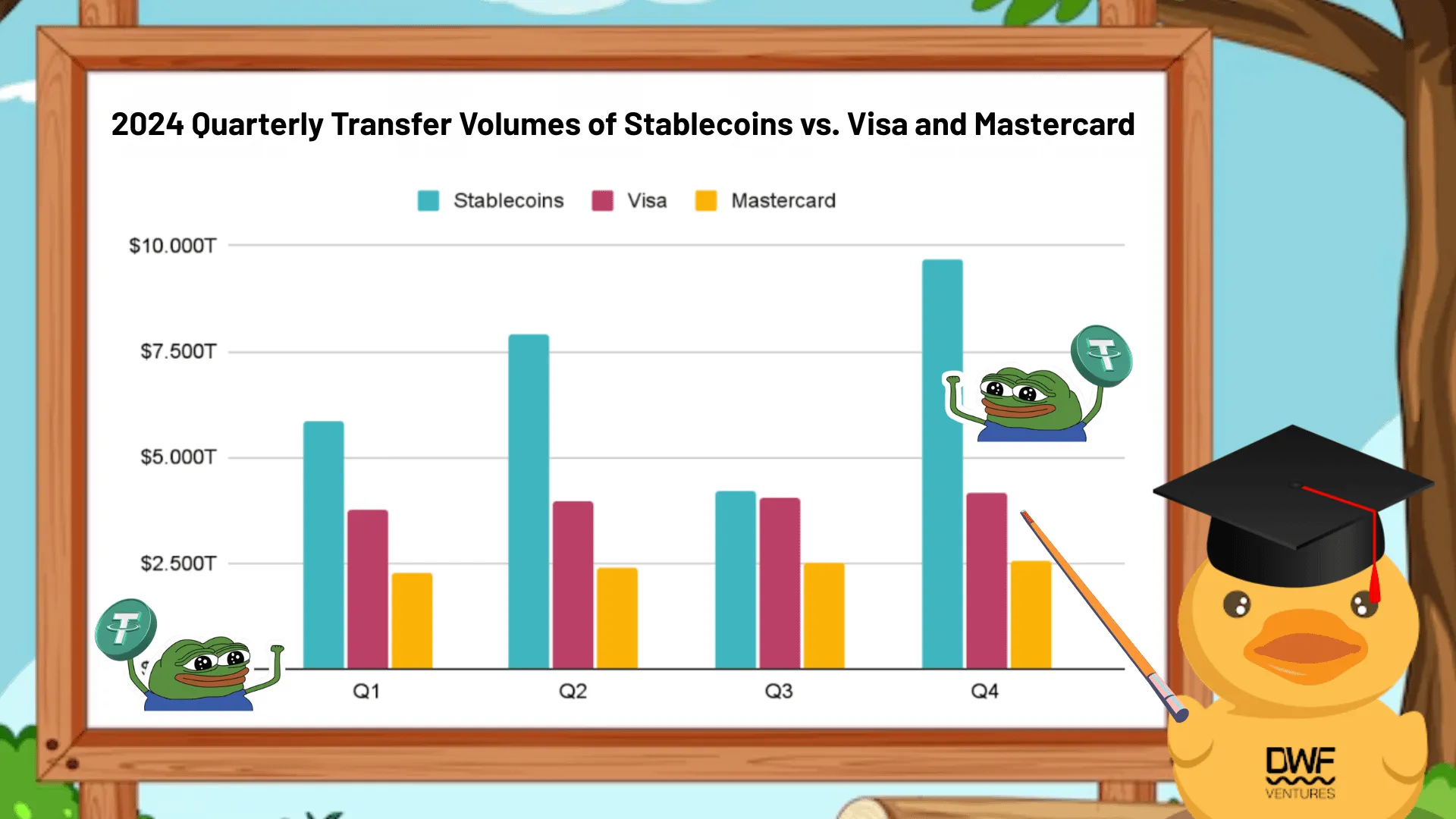

Stablecoins have rapidly evolved beyond simple on-chain pricing tools. With over $27 trillion in transfer volume in 2024, surpassing Visa and Mastercard, stablecoins are now a critical financial rail supporting remittances, global payroll, and fintech infrastructure. At the center of this development is Tether’s stablecoin, USDT.

But despite USDT’s leading position in volume, adoption, and infrastructure, new scaling solutions are emerging to push its utility even further. Plasma and Stable are blockchains that aim to upgrade USDT for real-world scalability. But what does this mean for the future of stablecoin infrastructure?

The Evolving Role of Stablecoins

Originally designed to offer stable value for trading cryptocurrencies, stablecoins now serve broader use cases, including:

- Cross-border remittances

- On-chain payroll and invoicing

- Inflation hedging in emerging markets

- Consumer payments infrastructure

In June 2025, the United States Treasury Secretary projected that the stablecoin market could reach $2 trillion by 2028. In the same quarter, Circle completed a successful initial public offering (IPO), and the U.S. Senate passed the GENIUS Act—a regulatory framework for stablecoins. These milestones have placed stablecoins at the forefront of policy and investment discussions in the United States, and the broader crypto industry.

Yet the question remains: does today’s stablecoin infrastructure have the capacity to meet the demands of this accelerating growth?

Current Efficiency Gaps in Stablecoin Infrastructure

Several technical and structural inefficiencies persist throughout the stablecoin infrastructure landscape. Liquidity remains fragmented across blockchains, limiting composability. Fiat on/off ramps are often complex and costly. Transparency in reserve management varies across issuers. Regulatory frameworks are still emerging and inconsistent across jurisdictions.

These conditions create friction for both institutional users and retail participants, prompting interest in alternative networks designed specifically to streamline stablecoin operations.

To understand the urgency behind these innovations, it is useful to examine USDT’s current role in the market and the structural challenges it still faces.

Market Overview: USDT Leads, but Structural Challenges Remain

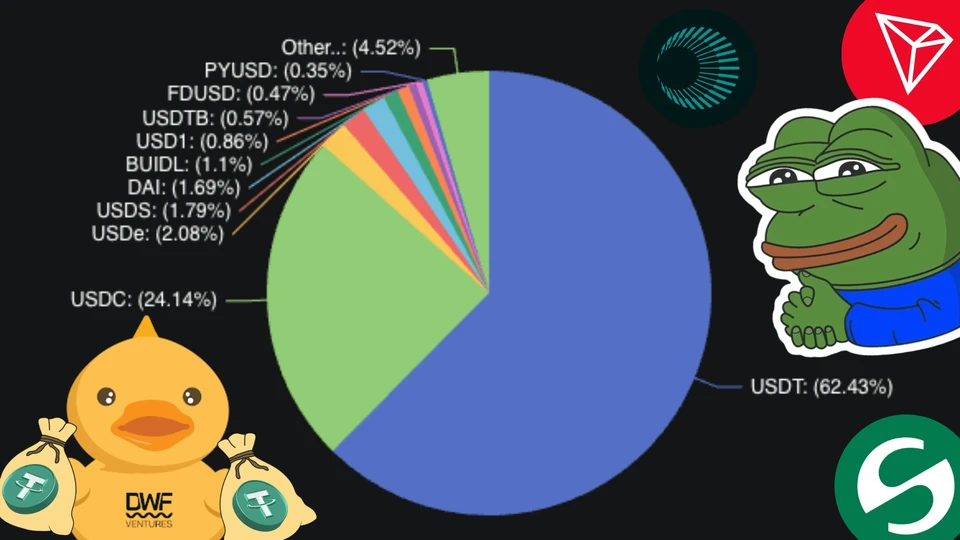

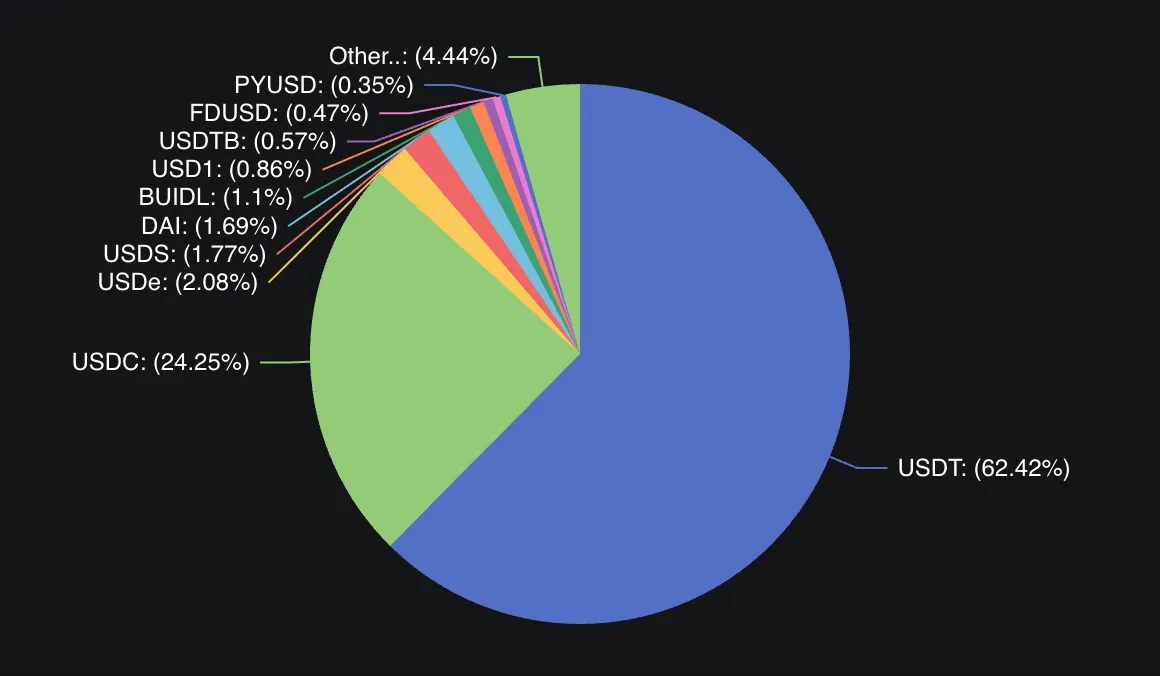

The stablecoin space comprises numerous projects different by design such as backing and peg maintenance. However, Tether is the most profitable company not only in crypto but across the entire global economy (although the latter is up to debate), with USDT holding a 62% share of the stablecoin market, as of June 2025. Alongside Tether’s closest rival, Circle’s USDC, the two stablecoins account for approximately 83% of all stablecoin transaction volume—more than 80% of which occurs on the Ethereum and Tron blockchains.

USDT currently maintains 8.6 million weekly active addresses, more than four times the number recorded for USDC. Approximately 50% of all USDT supply is held on Tron. USD-pegged stablecoins dominate the market, accounting for 95% of the total stablecoin capitalization. Tether generates around $4.9 billion in annual revenue and incurs $2.9 billion in network fees, split nearly evenly between Ethereum and Tron.

Migrating a greater share of this activity to lower-cost chains could significantly increase profitability. However, despite this growth, the stablecoin market remains highly concentrated and faces persistent challenges, including reliance on cross-chain bridges, centralization risks, and high fees on Ethereum. These limitations point out the need for more efficient and scalable infrastructure to support the next phase of adoption.

Two such solutions currently in development, Plasma and Stable sidechains, offer distinct approaches to resolving these constraints while expanding USDT’s functionality.

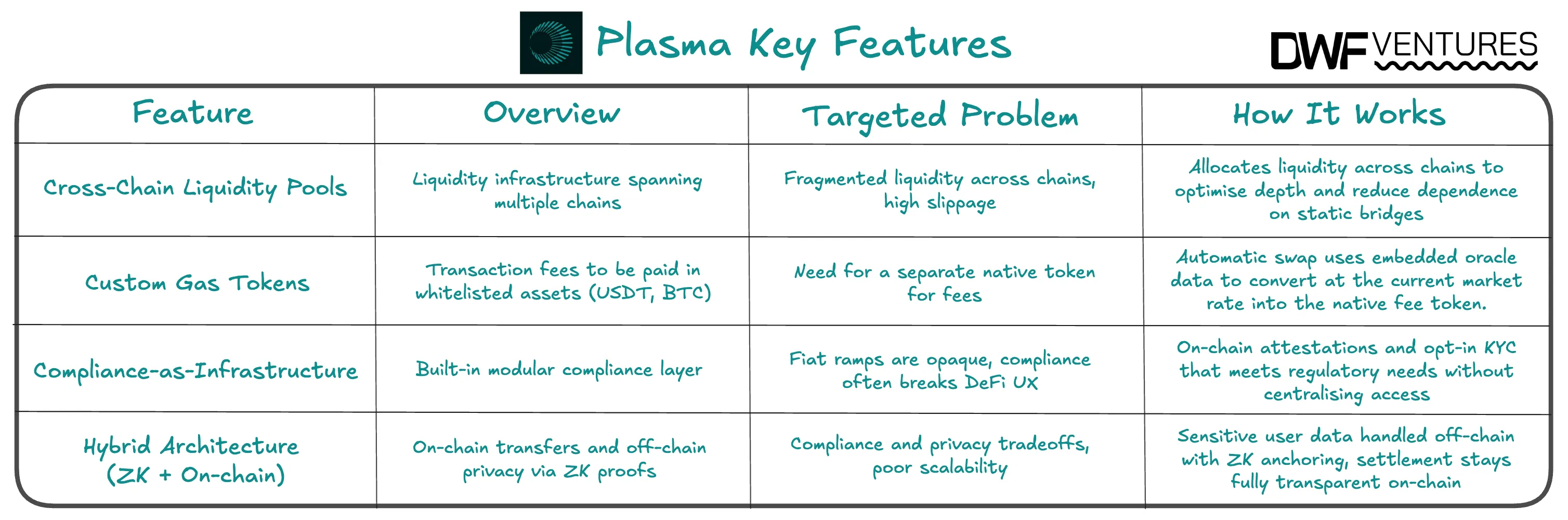

Plasma: A Bitcoin Sidechain for Stablecoin Utility

Plasma is an EVM-compatible sidechain built on the Bitcoin network and designed to optimize stablecoin transfers. Supported by Tether, it focuses on high-throughput financial use cases such as merchant payments, remittances, and commodity trading.

Its technical design is built around Reth, an execution engine written in Rust. Reth is a high-performance alternative to the standard Go Ethereum (Geth) CLI client and supports parallel transaction processing, improving scalability and reducing confirmation times. The use of Rust also enhances memory safety and execution reliability. Additionally, Plasma utilizes the HotStuff consensus algorithm, a Byzantine fault-tolerant protocol that enables blockchain nodes to agree on block inclusion even in the presence of faulty or malicious participants. This approach strengthens both resilience and finality in network operations.

Plasma combines the security of the Bitcoin blockchain with EVM compatibility, allowing developers to create decentralized applications while using USDT as a native asset. The platform also introduces yield mechanisms tied to Bitcoin, providing diversified returns within a stablecoin framework.

Below are key features that define Plasma’s approach to stablecoin integration and scalability:

Moving on to the next solution, Stable takes a distinct path in addressing the scalability and usability of USDT in high-frequency environments.

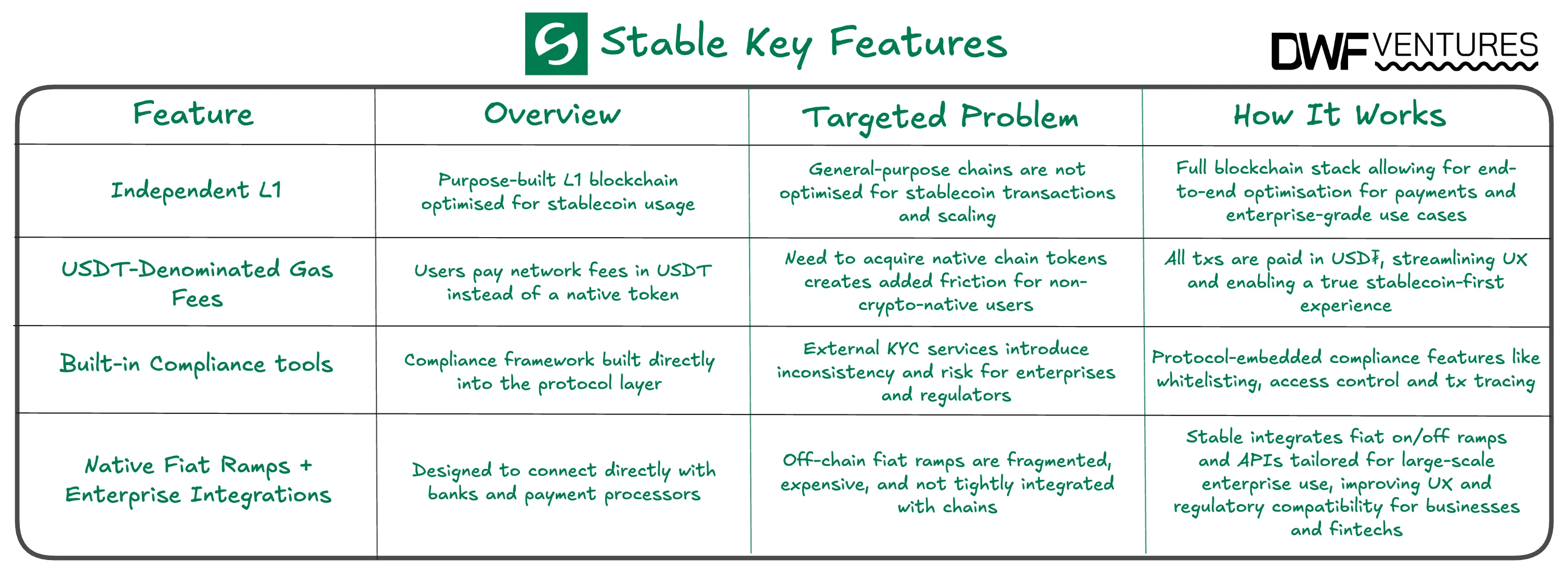

Stable: A Dedicated Layer 1 Optimized for USDT

Stable is a purpose-built Layer 1 blockchain that allows USDT to be used as the native gas token, reducing friction and costs for high-frequency transfers. Like Plasma, it is backed by Tether and focuses on expanding USDT’s functionality in high-frequency use cases.

Key features include:

Stable is particularly intended to make daily USDT transactions simpler, quicker, and more cost-effective. It is an excellent choice for anybody looking for a dependable platform for regular USDT transfers, payments, and settlements.

Initially, Stable Blockchain uses StableBFT, a modified Proof-of-Stake (PoS) consensus mechanism based on CometBFT, to provide fast throughput, low latency, and great network resilience. To improve consensus performance, Stable intends to separate data dissemination from the consensus process and implement direct transaction broadcasting to the block proposer.

Stable is positioned as a low-cost, developer-friendly alternative to traditional stablecoin rails, offering enhanced efficiency for both end users and service providers.

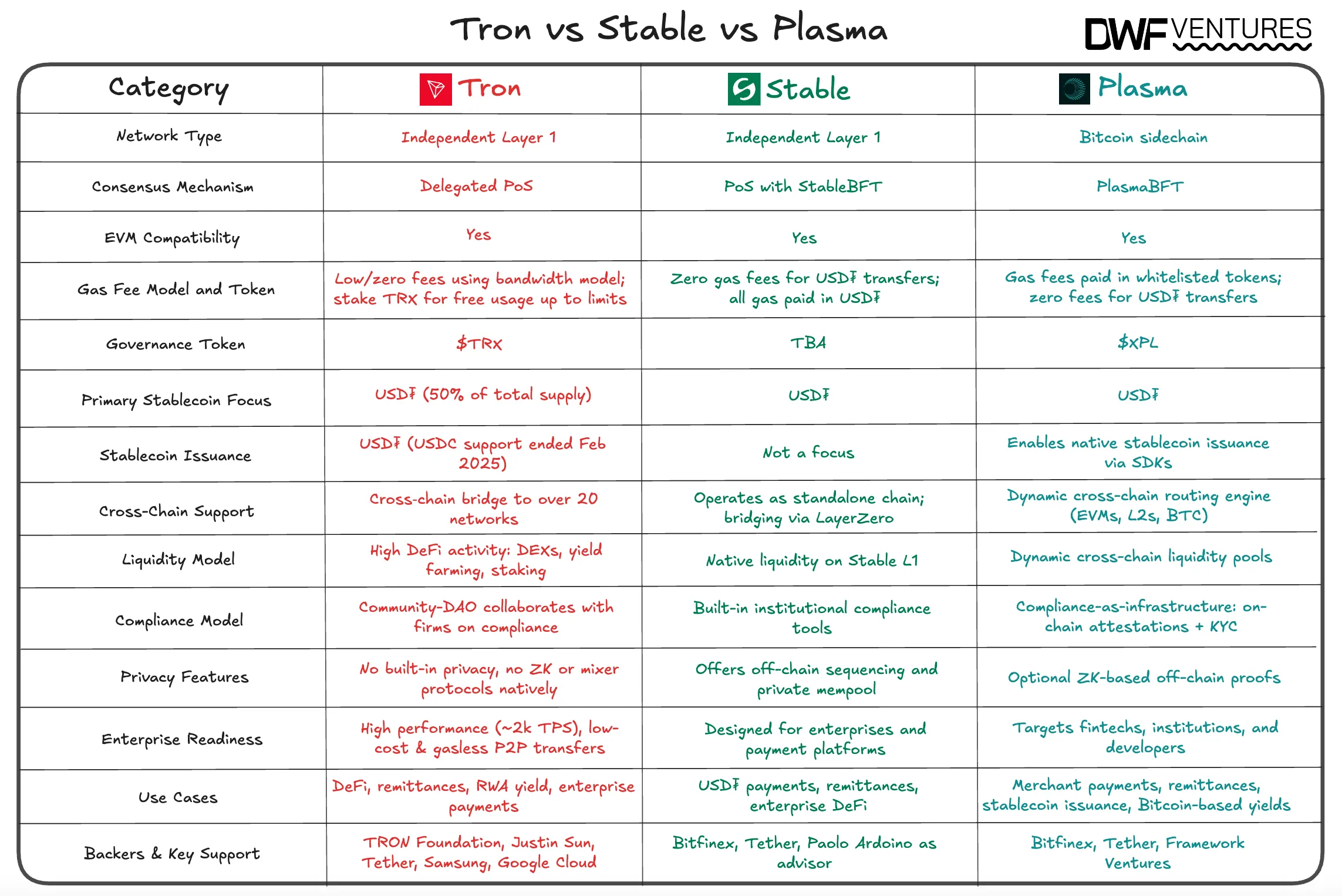

Comparing Plasma and Stable: Which One Fits USDT Better?

While both Plasma and Stable aim to optimize USDT usage, they take distinct technical approaches.

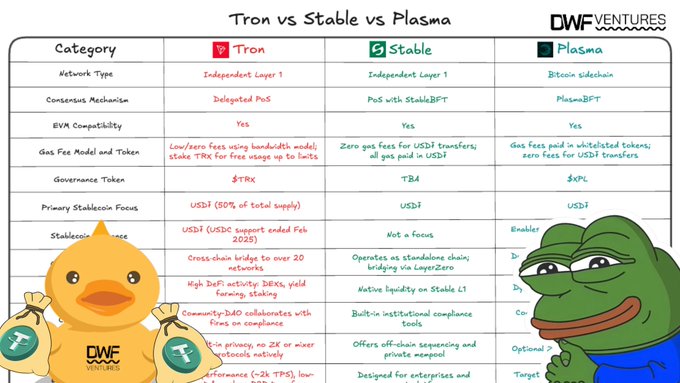

Both are backed by Tether, the primary beneficiary of their deployment. Shared traits include their use of USDT as a native gas token and the implementation of protocol-level compliance infrastructure. In the table below, you can see a detailed comparison of Plasma, Stable, and TRON, an L1 frequently used for transferring Tether tokens:

However, differences in network type, liquidity model, and privacy design suggest that each may develop a distinct role within the stablecoin ecosystem. Plasma, for example, operates as a Bitcoin sidechain with optional ZK-based off-chain privacy proofs and dynamic liquidity routing across EVMs and L2s. Stable, on the other hand, functions as a standalone Layer 1 with built-in institutional tools and native liquidity on its own chain.

Conclusion

Stablecoins are no longer experimental. They are forming the foundation of next-generation finance. However, continued adoption requires a more scalable, efficient infrastructure. Plasma and Stable are two efforts to meet that need—not by replacing USDT, but by optimizing the environment in which it operates and upgrading it for global adoption.

DWF Ventures sees infrastructure innovation as a key factor in unlocking the next phase of stablecoin adoption. If you are building solutions in this area, we encourage you to connect with our crypto venture capital team.

Disclaimer: This article is intended for general informational purposes only and does not constitute financial advice. Readers should conduct their own research and consult with a professional advisor before making any investment decisions.