2025: A Year in Crypto

Updated On 17 March 2026

Published On 31 December 2025

2025 has proved to be a tumultuous year for the crypto industry. From explosive memecoin frenzies that captured markets to landmark regulatory frameworks finally taking shape, showing the duality of crypto's ongoing evolution. DWF Ventures took a look back on the year through quarters.

Q1: Fresh Blood

Donald Trump’s inauguration on 20 January ushered in a wave of crypto-friendly initiatives from his administration. Key announcements included the establishment of a Strategic Bitcoin Reserve in March 2025 and renewed commitment on his family’s venture, World Liberty Financial, and its stablecoin USD1.

While memecoins have long been a fixture in the crypto market and culture, nothing compared to the frenzy surrounding Trump’s token launch. As highlighted in our previous article, the event had a significant impact on many stakeholders in the industry while fueling further growth of memecoins in the quarter and beyond.

DeepSeek’s R1 reasoning model was released on 20 January 2025, emerging as a strong competitor against OpenAI — offering superior cost efficiency and accessibility. Though its debut triggered valuation declines across both equity and crypto markets, it drove product innovation and integrations which benefitted end users. Alongside another Chinese AI model, Qwen, DeepSeek re-emerged in the headlines in Q3 2025, beating other popular AIs in the crypto trading competition.

Meanwhile, the venture capital landscape went not without big records. Binance secured a landmark $2 billion investment from MGX, an Abu Dhabi based firm backed by the UAE government. As the largest standalone investment in a crypto company to date, this deal underscores growing institutional demand for crypto exposure. Other notable private investments include Polymarket ($2 billion), Applied Digital ($788 million), Tempo ($500 million), and Flying Tulip ($200 million), among others.

In the same vein, the growing industry still remains vulnerable to security incidents, one of which, unfortunately, happened to Bybit in February 2025. However, the crypto exchange managed to swiftly secure strategic funding from a number of major crypto VC firms, including DWF Labs and Galaxy Digital, to cover losses for platform users. While users were fully compensated, the breach reinforces the need for enhanced custody solutions as cyber threats continue to evolve. Cybercrime remains a crippling issue for crypto: Chainalysis estimates the total amount of stolen digital assets in 2025 to exceed $3.4 billion, more than 50% growth from 2024.

Q2: Institutional Adoption and Support

In line with more crypto-friendly initiatives, Trump appointed Paul Atkins as the new SEC Chairman in April 2025, and established a dedicated Crypto Task Force to develop a comprehensive framework for distribution of digital assets. The administration’s decision to drop the longstanding Ripple lawsuit further demonstrated its pivot toward regulatory accommodation.

Digital Assets Treasuries (DATs), publicly-listed entities that hold crypto on their balance sheets, also gained momentum as an avenue for investors seeking equity exposure. While Microstrategy (MSTR) pioneered the model, alternative DATs started coming into prominence in June, starting with Fundstrat’s Bitmine (BMNR) and Consensys CEO’s Sharplink Gaming (SBET) which focused on ETH accumulation. This trend accelerated into the third quarter, and is expected to remain in one way or another further into 2026, despite significant capital outflows by the end of 2025, caused by market volatility.

On-chain liquidity remained robust among tokens as it marked the start of “Launchpad Wars”. Competing token launchpads on Solana proliferated during Q2 2025, each offering distinct launch mechanisms and rewards structures designed to capture and strengthen the liquidity flywheel.

On the infrastructure side, Coinbase introduced the x402 protocol, a standard for embedding on-chain payment gateways onto any API, with a particular utility for AI agents. Combining low costs, high speeds and seamless integration, the protocol is set to grow significantly in the coming year.

Circle’s IPO resulted in one of the largest crypto companies to be listed on the NYSE, generating substantial investor interest and signaling institutional confidence in regulated crypto entities. They also announced the launch of Arc, a stablecoin-oriented chain powered by USDC, generating interest from traditional companies such as Blackrock and Goldman Sachs to come onboard.

Q3: Promising Signs and Trends

Two foundational bills were proposed in the United States in 2025, contributing to the long-awaited regulatory certainty around cryptocurrencies. The GENIUS Act, signed into law in July 2025, introduced formal rules for stablecoins. The Clarity Act, which gives the framework for distinguishing between utility tokens and securities, was proposed in May 2025, has passed the the House of Representatives, and is currently waiting for the hearing by the Senate.

The U.S. fiscal policy has played a big role in the crypto market performance. In Q3 2025, the Federal Reserve started a series of the federal fund rate cuts. Market participants are expecting further reduction of the Fed rate rate and quantitative easing in the coming year, which is broadly expected to create favorable conditions for risk assets, including crypto.

TradFi giants kept tapping into the crypto market. Robinhood, the company behind the top stock trading app, announced significant expansion plans of its crypto offerings, including the launch of its own Layer 2 blockchain and tokenized stock products enabling extended trading hours (24 hours, 5 days a week). These developments underscore the company’s commitment to crypto, and the ongoing convergence between traditional finance and digital assets.

DATs continued to gain traction as a vehicle for traditional investors seeking crypto exposure, with some entities implementing active strategies to generate additional yield beyond passive holding. Notable new entrants include Sonnet Biotherapeutics (SONN) and DeFi Development Corp. (DFDV) which allocated capital into Hyperliquid (HYPE) and Solana (SOL) respectively.

Perpetual DEXs maintained momentum as viable alternatives to centralized venues. While HyperliquidX retained its market leading position, there were many new notable entrants. Chain-representative platforms like Avantis (Base) and Aster (BNB Chain) grew rapidly, alongside multi-assets platforms like Lighter and OstiumLabs, which are positioning themselves as the all-in-one platform for crypto, equities and commodities on-chain.

ICOs have well and truly returned, with multiple high-profile raises demonstrating sustained investor appetite. A memecoin launchpad Pump.fun raised over $600 million on the public token sale of its $PUMP token alone. Other notable raises included Plasma’s $373 million on Sonar and Falcon Finance’s $113 million on Buidlpad, reflecting strong committed capital across various fundraising platforms.

Q4 Giant Reset Button

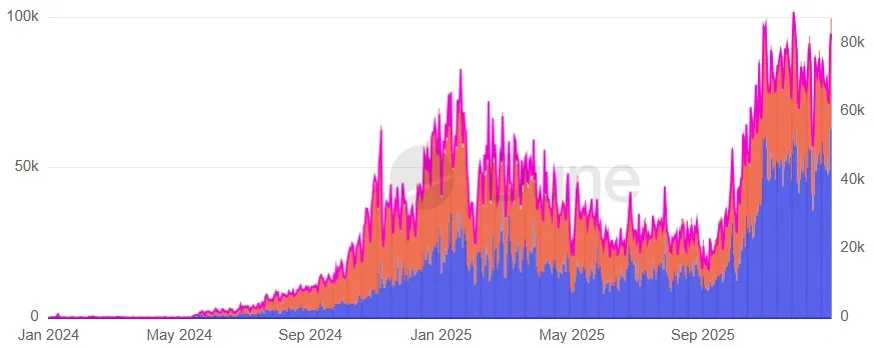

The fourth quarter’s most significant event occurred on October 10, when the crypto market experienced its largest liquidation event which wiped out over $19 billion in leveraged positions. While the catalyst was the U.S. announcing a 100% tariff on Chinese imports, the unprecedented scale of the cascade revealed underlying structural vulnerabilities within market infrastructure itself. This would put a huge question mark on current infrastructures while dampening investor confidence substantially.

At the same time, this event further drove the momentum for DEX perp trading: total trading volume in October grew 10x year-over-year, climbing to an ATH of $903 billion, while the DEX/CEX perp trading ratio surpassed 10% for the first time.

Prediction markets were running hot since the U.S. presidential elections late last year. Its recent institutional validation was marked by record-breaking investments: Kalshi’s $1 billion raise in the beginning of December and the already mentioned Polymarket’s $2 billion round. The uptick in volumes of prediction markets can also be attributed to expanding liquidity pools, broader category offerings, and improved user experience, collectively attracting a more diverse participant base. Overall in 2025, prediction markets have moved from niche bets to the mainstream financial market.

On-chain metrics for Polymarket show that user activity has been consistently increasing starting from September, reaching new ATHs:

New blockchains such as Monad, MegaETH and Stable, launched in Q4 2025 in either mainnet or testnet, continue to be well anticipated as significant capital has been allocated to these ecosystems. While each chain has its own niche in terms of speed and purpose, unique apps are still a main decision factor for users to get onboarded onto each of them.

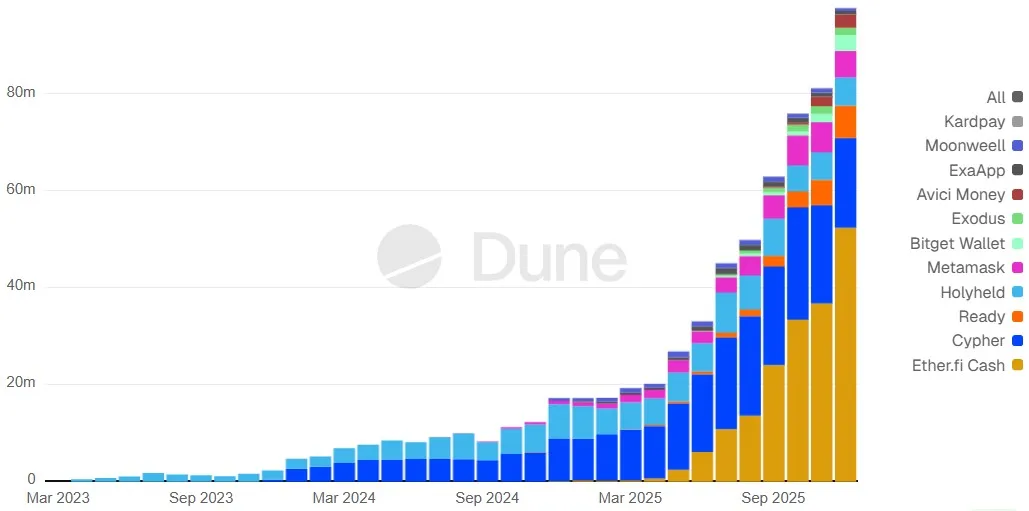

Cards and neobanks are proliferating, as it gets easier and easier to onboard from legacy finance onto crypto rails. Differentiation is currently marked by acquisition campaigns and marketing, which will likely grow stronger as more brands enter the scene. 2026 will be a test to see what users are more concerned about — safety of funds or rewards.

Volume of spending with crypto cards has grown from around $17 million in January to almost $98 million by the end of 2025, showing the increasing adoption:

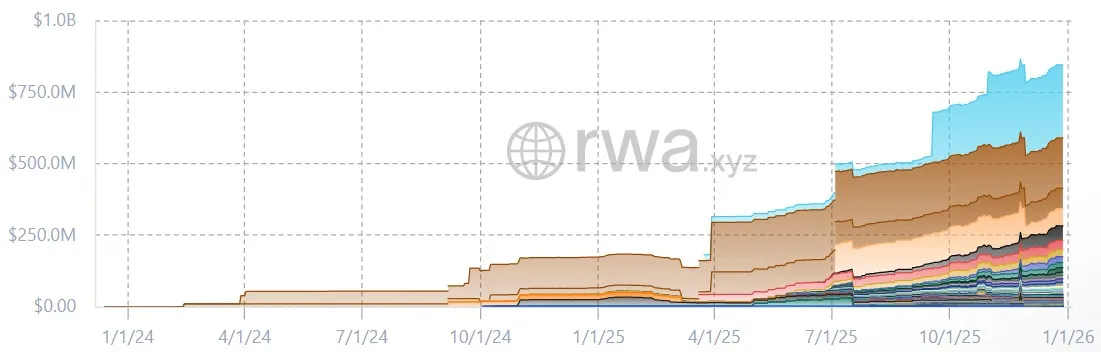

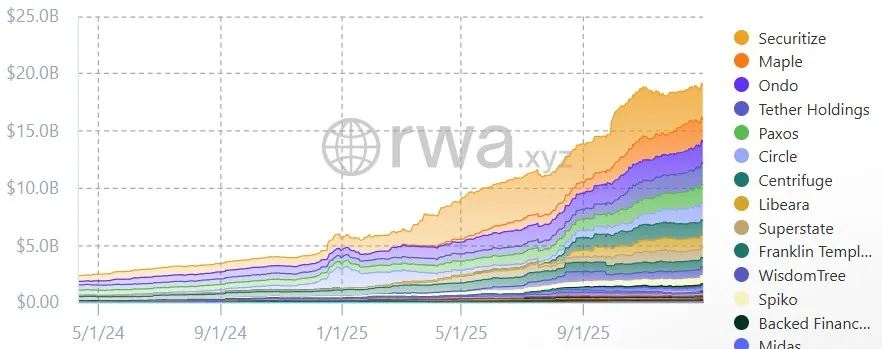

Wrapping up the Q4 2025 in crypto, RWAs continued its upward trajectory as more tokenized products such as Blackrock’s BUIDL and Van Eck’s VBILL are coming on-chain through platforms like Securitize. Solana has also been making a push towards this sector, seeing a 350% year-over-year growth. We’ll expect to see more of this growth in the coming year as well.

What Trends Will Drive Crypto in 2026?

Stablecoins

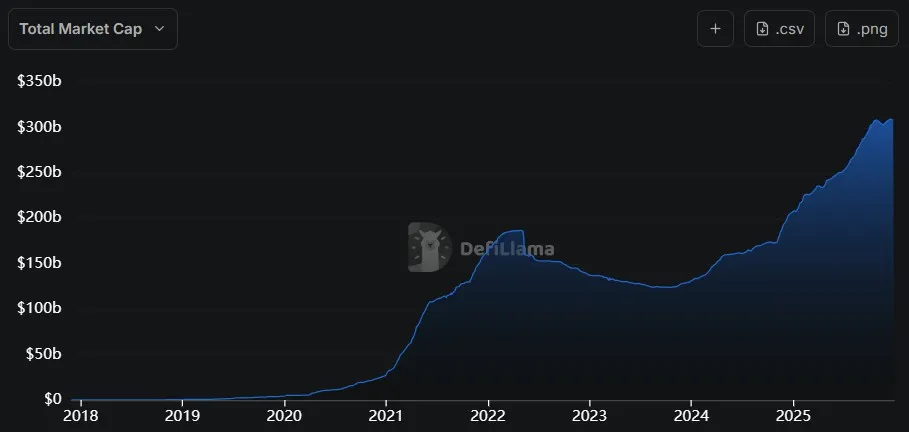

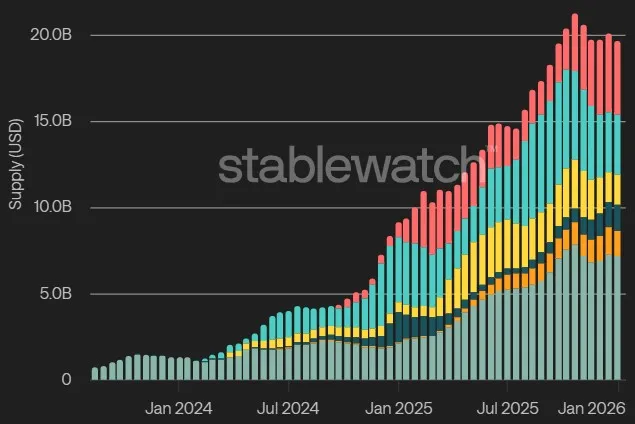

The year has been characterized by strong institutional adoption and infrastructure development. Regulatory support for stablecoin growth has proven to be impactful, with total stablecoin supply expanding over 50% year-to-date, surpassing $300 billion for the first time in November 2025.

The expansion of yield-bearing stablecoins into becoming the $20 billion market (albeit getting hit by the liquidity meltdown in October) also represents a new value proposition for institutional and retail participants.

Regulation and TradFi

This regulatory clarity has catalyzed a wave of institutional product launches as traditional finance players seek to expand their digital asset footprint. BlackRock’s BUIDL partnership with Binance, alongside new entrants such as Paxos’s USDG exemplifies this trend. As margins in TradFi compress, institutions are compelled to adopt crypto rails driven by the advantages of faster settlement times, enhanced liquidity, and access to new revenue streams in an expanding market. We expect to see this trend accelerate in the coming year.

Crypto Perpetual DEXs

On the on-chain side of things, two notable sectors are in an “up-only” trend. DEX derivatives volume is growing rapidly in comparison to CEX volume, as DEXs have grown rapidly in liquidity while CEX infrastructure has faced several issues in the year. The ratio between DEX/CEX futures trading volume has gone up from about 6% in January to over 18% in November, showing that on-chain protocols are just as competitive and scalable as centralized venues.

RWA Tokenization

Along with the growth of on-chain crypto derivatives trading that we already highlighted above, the RWA sector has also expanded greatly, with total value of tokenized assets growing from $4 billion to $18 billion by the end of 2025, enabling easier access to yields that were once restricted. Beyond accessibility, these tokenized assets are able to gain new utility by integrating with crypto lending products.

All these developments show that the blockchain industry has matured beyond crypto into credible financial infrastructure.

Despite many ups and downs, crypto is definitely here to stay. As we emerge beyond speculations and memecoin casinos, the next stage of growth is already set with the infrastructure in place. Bring on 2026!